Europe Biotechnology Market Growth and Future Trends

Other |

2026-03-04 05:13:22

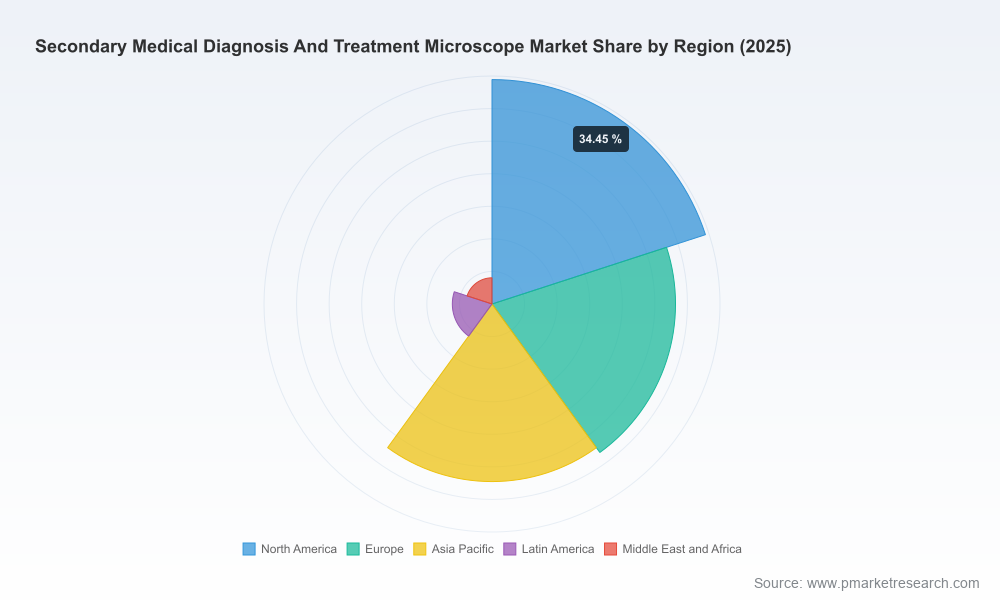

PW Consulting’s latest market study on the Secondary Medical Diagnosis and Treatment Microscope market — base year 2025, historical 2020–2025, forecast 2026–2032 — distills the commercial and clinical forces set to shape vendors’ and health systems’ choices in 2026. The market has expanded from roughly USD 621.8 Million in 2020 to an estimated USD 920.0 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 8.15% across the 2026–2032 forecast window, reaching approximately USD 1,592.11 Million by 2032. These headline metrics capture an industry transitioning from optics-led hardware competition to ecosystems where digital visualization, workflow integration, and procedural enablers drive purchasing decisions.

Secondary Medical Diagnosis And Treatment Microscope Market

Capital allocation. The sustained mid-single-digit-plus CAGR signals persistent demand for capital equipment in hospital operating rooms and specialty clinics; boards and strategy teams must reconcile growth opportunities with extended procurement cycles and capex scrutiny.

Secondary Medical Diagnosis And Treatment Microscope Market

Product strategy. Optical performance alone no longer guarantees differentiation. Digital 3D visualization, AR fluorescence, heads-up displays and software-enabled workflow integration are increasingly determining value perception and total cost of ownership.

Secondary Medical Diagnosis And Treatment Microscope Market

M&A and partnerships. Market dynamics favor combinations that couple proven optics with digital platforms, advanced imaging modalities, and service-led commercial models.

Three dynamics deserve prioritized attention in 2026 planning cycles:

Technological convergence: The OR is standardizing around integrated visualization suites — 3D/4K imaging, fluorescence-assisted modalities, and heads-up displays — that improve ergonomics, team situational awareness, and documentation. These features are migrating from premium to mainstream configurations, shifting competitive boundaries.

Regulatory momentum: Recent regulatory actions are reshaping clearance pathways for adjunct visualization technologies. Notable developments include a U.S. FDA 510(k) clearance enabling fluorescence-assisted visualization for high-grade gliomas, and broader device reclassification actions affecting certain optical diagnostics. Vendors must build regulatory intelligence into product roadmaps, particularly where adjunct devices enable new intraoperative decision-making.

Reimbursement and procurement realities: Surgical microscopes continue to be procured within existing DRG/CPT frameworks that reimburse the procedure rather than the hardware itself. This amplifies the importance of demonstrating procedural value (shorter OR time, better outcomes, fewer complications) and designing commercial models (service bundles, subscription/software licensing, outcome-based contracts) that reduce perceived capex burden for hospital finance teams.

The competitive map is populated by established optics incumbents that are rapidly incorporating digital visualization and by newer entrants advancing exoscopic and software-centric approaches. The landscape exhibits moderate concentration, with a set of global vendors influencing product direction and go-to-market practices. Key strategic moves observed in 2025–2026 illustrate where competition is intensifying:

Carl Zeiss Meditec AG — continues to leverage deep optical heritage while accelerating digital integration; recent regulatory approvals in key markets have expanded access for its latest ophthalmic microscope platforms, supporting growth in anterior and posterior segment procedures and reinforcing channel credibility in markets with rigorous device review.

Leica Microsystems (Danaher) — pushing hybrid optical/digital propositions with 3D real-time visualization and headset integration, targeting neurosurgery and ophthalmology teams that prioritize collaborative viewing and teaching capability in high-acuity cases.

Haag-Streit Group — has rapidly broadened its ophthalmic portfolio with a next-generation microscope and an optional 3D heads-up module; this product expansion underscores a trend toward modular architectures allowing incremental upgrades rather than full-system replacements.

Alcon, Olympus, Topcon, Takagi — these vendors maintain strong ophthalmic and multispecialty presence by combining illumination, imaging, and surgeon ergonomics; their efforts center on seamless integration with microscope accessories and imaging suites used in high-volume procedures.

Synaptive Medical & Karl Storz — exemplify the shift toward exoscopic and endoscopic visualization systems for neurosurgery and ENT, offering high-resolution imaging platforms that can change theatre ergonomics and team workflows.

Seiler Instrument — remains relevant in dental and ambulatory surgical markets through value-oriented optics and service support, illustrating that differentiated go-to-market models (e.g., focused clinical training and local service networks) remain powerful competitive levers.

Market entries and upgrades: Multiple manufacturers launched or upgraded 3D digital heads-up modules and 3D-capable microscopes during 2025–2026, signaling mainstream acceptance of heads-up visualization as an OR standard for many procedures.

Regulatory approvals: Targeted approvals for fluorescence visualization in neurosurgery and reclassification of certain optical diagnostics into Class II with special controls in 2026 alter the commercialization calculus for adjunct imaging accessories; firms that anticipated these moves are better positioned to accelerate adoption.

Commercial impact: Given the procedure-focused reimbursement environment, vendors that can quantify and credibly communicate procedure time reduction, case conversion improvements, and educational benefits will secure preferential procurement outcomes.

Our full market study goes well beyond headline sizing and trend comments — it is structured to be directly actionable for business leaders working on 2026 strategic plans. Key deliverables include:

Transparent market sizing and forecasting methodology (historical 2020–2025; base year 2025; forecast 2026–2032) — enabling replication and sensitivity testing against alternative adoption curves.

Technology adoption maps and feature diffusion timelines that prioritize capabilities (3D/4K, AR fluorescence, heads-up displays, exoscopy) by clinical value and procurement barriers.

Competitive positioning dossiers for leading vendors with SWOT-style implications for product development, partnership, and M&A strategies.

Commercial playbooks: go-to-market segmentation hypotheses, hospital decision-maker personas, procurement tender templates, and service-model scenarios to de-risk launch and upgrade programs.

Regulatory & reimbursement mapping: a concise navigator of clearance pathways, recent regulatory actions, and payer engagement tactics relevant to microscope-adjunct technologies.

M&A and investment scorecards highlighting capability gaps and potential targets that would accelerate entry into digital visualization, imaging analytics, or installed-base monetization.

Prioritize modularity: design product lines and commercial offers that allow incremental upgrade to digital visualization to lower healthcare buyers’ upgrade friction.

Monetize services: shift from pure-capex selling to recurring revenue through software licensing, subscription imaging services, and prioritized service agreements tied to uptime and training outcomes.

Invest in regulatory foresight: allocate resources to preemptively validate adjunct technologies against emergent regulatory classifications and to build robust clinical evidence for intraoperative visualization claims.

Build OR ecosystem partnerships: collaborate with digital-imaging and AI companies to offer end-to-end solutions that improve procedural throughput and outcomes — differentiating on usability and interoperability.

Target hospital systems: given that hospitals remain the primary end-user segment, concentrate pilot programs and value demonstrations within integrated health systems capable of scaling adoption across sites.

Adopt outcome-based contracting pilots: test limited-scope payment models that tie part of the instrument’s economics to measured OR efficiencies or clinical endpoints.

The Secondary Medical Diagnosis and Treatment Microscope market presents a compelling growth profile — underpinned by a robust CAGR and a forecast doubling of market scale over the next decade — yet it is also a market where product differentiation is shifting from pure optics to system-level value. For executives planning 2026 investments, the strategic imperatives are clear: move beyond commodity optics, accelerate digital integration, design customer-friendly commercial models, and build regulatory and clinical evidence pathways into every product program. Our full report provides the granular segment-level sizing, company benchmarking, and scenario matrices necessary to convert these imperatives into executable plans.

This release is intended as a strategic preview. For the comprehensive dataset, segment-level analysis, company scorecards, and downloadable models that underpin these conclusions, please contact PW Consulting to request the full Secondary Medical Diagnosis and Treatment Microscope Market report and supporting appendices.

For detailed analysis of this topic, please visit the official page:Secondary Medical Diagnosis And Treatment Microscope Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com