Non Fused Switch Disconnector Market Report: Trends, Growth, and Future Outlook

Technology |

2026-03-17 09:45:30

As sustainability shifts from a brand differentiator to a compliance and supply‑chain imperative, packaging for the pet food sector is entering a decisive phase. PW Consulting’s latest market study — with base year 2025 and a 2026–2032 forecast horizon — quantifies that transition and translates it into action‑oriented guidance for executives planning investments, procurement strategies, and innovation roadmaps in 2026. The global sustainable pet food packaging market reached USD 3,520.4 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 8.12% through the forecast window, approaching USD 6,080.43 Million by 2032. This brief highlights the report’s strategic value while preserving the granular segment-level detail available in the full study.

Sustainable Pet Food Packaging Market

Regulatory inflection points are compressing time to action. Multiple producer responsibility programs and state-level EPR laws now impose reporting, registration, and financial obligations on packaging producers — a compliance landscape that materially affects material selection, labeling, and supplier contracts.

Sustainable Pet Food Packaging Market

Material and input cost volatility is reshaping sourcing strategies. Recycled PET and other circular feedstocks command premium pricing dynamics that will influence total cost of ownership (TCO) calculations for packaging conversion projects and contract negotiations in 2026.

Sustainable Pet Food Packaging Market

Market growth at an 8.12% CAGR demands both scale and optionality. Companies that plan for modular packaging platforms and diversified supply relationships will be better positioned to capture upside while managing risk.

The PW Consulting report is purposely operational. Beyond headline sizing and trajectory, the study equips teams with the tools they need to execute in 2026:

Forward-looking market model (2026–2032) with scenario pathways tied to regulatory adoption, raw‑material pricing, and consumer premiumization — designed for CFOs and strategy teams to stress‑test investment cases.

Supplier and capability mapping with scorecards for circularity, barrier performance, cost profile, and provenability of sustainability claims — tailored templates that procurement can deploy immediately.

Packaging innovation playbook: decision trees for material substitution (e.g., mono‑material flexible films, paper‑based laminates, compostable formulations), hybrid approaches, and sample validation protocols for shelf‑life, barrier, and mechanical testing.

Regulatory impact matrix that translates state, national, and international producer responsibility rules into procurement triggers, reporting obligations, and product labeling consequences.

Operational checklists for pilot programs: test design, KPI selection (carbon footprint per pack, recyclability rate, cost delta), retailer acceptance criteria, and go/no‑go gating for rollouts.

Investor and M&A filters highlighting target profiles (technology, scale, geographic reach) aligned with consolidation scenarios and the current market concentration dynamics.

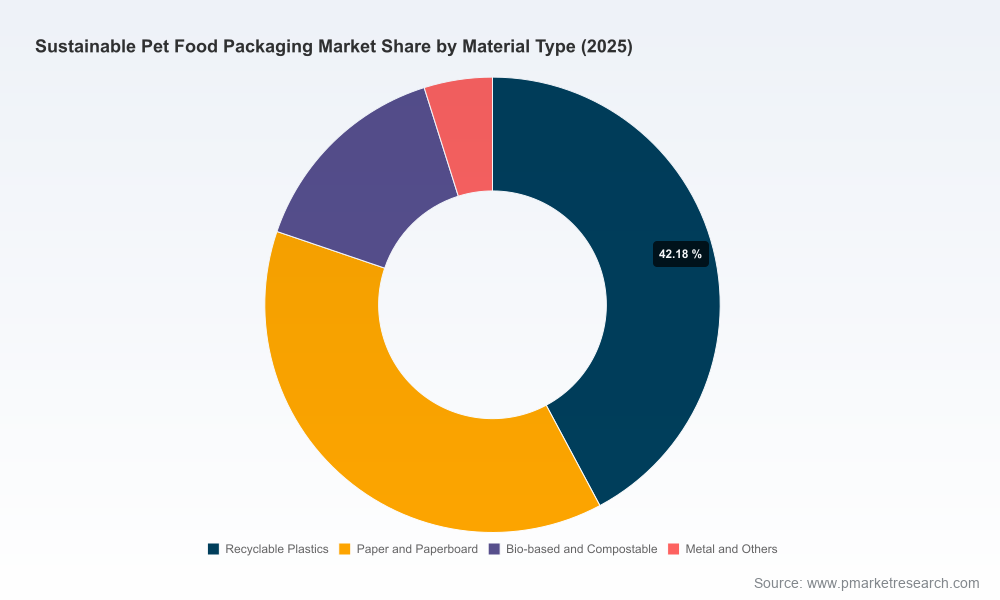

The market exhibits a moderate degree of supplier concentration: the top three suppliers account for 28.4% of market revenue (CR3), while the top five reach 42.15% (CR5). This structure creates a dual dynamic — established global players set technical and commercial baselines, while a diverse field of regional specialists and innovators accelerates niche adoption.

Key incumbent profiles covered in the report include:

Amcor plc (Switzerland) — leading in recyclable flexible formats and mono‑material innovations targeted at premium pet food pouches and bags.

Mondi plc (United Kingdom) — known for paper‑based and recyclable flexible solutions, including mechanically reinforced multi‑layer structures for high‑performance applications.

ProAmpac LLC (United States) and Berry Global Group, Inc. (United States) — providers of recyclable mono‑material systems and lightweight, high‑barrier films respectively, both focusing on scalability and circular material streams.

Sonoco Products Company, Huhtamaki Oyj, Printpack, Greiner Packaging, Constantia Flexibles, Crown Holdings, Smurfit Kappa, and Silgan Holdings — each with differentiated competency sets spanning rigid and flexible formats, paper and board solutions, and metal containers for wet pet food applications.

Recent corporate moves underscore the innovation cadence: Amcor launched advanced recyclable flexible solutions in February 2026; Berry Global rolled out lightweight high‑barrier offerings in January 2026; Sonoco expanded its paper‑based pet food portfolio in late 2025; and Greiner continued development of mono‑material lids for wet pet food in early 2026. These developments, and broader industry showcases such as the Sustainability Pavilion at Global Pet Expo 2026, are accelerating the diffusion of recyclable and high‑performance formats into mainstream brand spec sheets.

Producer responsibility programs (e.g., California SB 54, emerging state laws in the U.S., and similar schemes in other jurisdictions) will require companies to operationalize reporting and fee management workflows in 2026. Brands should prioritize systems integration between packaging teams and compliance functions to avoid last‑minute exposure.

Price signals for recycled feedstocks matter now. For example, rPET spot dynamics reached levels that materially change payback timelines for conversion projects in late 2025. Procurement teams should incorporate index‑linked clauses and short‑term hedges into supplier contracts while evaluating multi‑feedstock flexibility to moderate cost risk.

Convert pilots into platform strategies: move beyond single SKU pilots and design modular packs that can be adapted across formats (bags, pouches, cartons) to spread development and tooling costs.

Embed regulatory forecasting into procurement cycles: assign a regulatory owner for each major market and align supplier KPIs with upcoming EPR milestones and reporting requirements.

Prioritize supplier partnerships that offer circular feedstock integration: choose partners that can demonstrate traceability, PCR availability, and performance parity to incumbent materials.

Operationalize sustainability claims with verification: adopt independent testing and chain‑of‑custody verification for recyclability and recycled content claims to reduce brand risk and support retailer requirements.

Rebalance investments between capex for new conversion equipment and opex for higher‑cost sustainable feedstocks: use PW Consulting’s TCO model to quantify the trade‑offs under multiple price scenarios.

Leverage packaging as a growth lever: align premiumization strategies (design, convenience, portioning) with sustainability transitions to preserve margin while meeting consumer expectations.

PW Consulting positions the study as a playbook for near‑term execution and medium‑term resilience. Use the report to:

Inform 2026 capex prioritization: apply scenario outputs to decide which packaging lines to retrofit, which to replace, and which formats to pilot.

Reframe procurement KPIs: incorporate circularity metrics, on‑time compliance deliverables, and indexed pricing mechanisms into RFPs and long‑term agreements.

Support M&A and partnership screening: filter targets by technological readiness, supply‑chain fit, and commercial synergies using the report’s acquisition scoring matrix.

Structure market entry and expansion plans: the forecast and scenario analysis will help regional teams prioritize markets and channel strategies while avoiding short‑term overcommitment in high‑cost input environments.

In line with a “trailer” approach designed to spur actionable follow‑up, this brief highlights market scale, growth trajectory, concentration metrics, and the directional competitive and regulatory context. To preserve the integrity of proprietary forecasting and tactical segmentation models — which are central to execution planning — detailed breakdowns by region, material type, and packaging format are reserved for the full report and accompanying data workbook. Executives and procurement leaders seeking the granular slices required to operationalize SKU migration, supplier selection, and SKU‑level cost modeling should consult the complete deliverables.

For leadership teams preparing 2026 budgets and 3‑year operating plans, PW Consulting recommends a two‑week “rapid alignment” workshop to convert the report’s scenarios into board‑level decision memos and procurement RFIs. The full report includes templates and a downloadable model that will accelerate this work.

PW Consulting’s Sustainable Pet Food Packaging Market study is expressly built for leaders who must reconcile sustainability commitments, regulatory compliance, and margin stewardship. The market’s near‑term trajectory (USD 3,520.4 Million in 2025; CAGR 8.12% through 2032) signals both urgency and opportunity — the companies that align product, procurement, and compliance strategies in 2026 will secure optionality and competitive advantage as the market matures.

For detailed analysis of this topic, please visit the official page:Sustainable Pet Food Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com