Ceramics and Glass Innovation: Driving the Growth of the Feldspar Market

Other |

2026-05-11 09:18:19

As global wind fleets scale and project developers push into ever-larger turbine classes, the choice between traditional gearbox-driven drivetrains and emerging direct drive architectures remains one of the most consequential engineering and commercial trade-offs in the renewable-energy value chain. PW Consulting’s new Wind Turbine Gearbox and Direct Drive System Market report—anchored on a 2025 base year and a 2026–2032 forecast window—offers actionable intelligence for executives preparing investment and product strategies in 2026.

Wind Turbine Gearbox And Direct Drive System Market

Our topline synthesis shows the market reached approximately USD 32.92 billion in 2025 and is projected to expand to around USD 49.27 billion by 2032. This trajectory reflects a compound annual growth rate (CAGR) of roughly 5.85% over the forecast period. These macro dynamics mask pronounced structural shifts—driven by technology choices, supply-chain bottlenecks, and regulatory interventions—that will materially affect vendor competitiveness, project economics, and capital allocation decisions next year.

Wind Turbine Gearbox And Direct Drive System Market

Policy and trade shock risk is rising. Recent government actions have elevated the probability of trade interventions and tariffs on key drivetrain components. Several announced measures and investigations in late 2024–2025 create an environment where sourcing strategy and footprint decisions will increasingly determine cost and schedule outcomes for wind projects.

Wind Turbine Gearbox And Direct Drive System Market

Raw-material constraints are reshaping technology economics. Direct drive permanent-magnet solutions depend on concentrated supplies of rare earth elements; volatility and sourcing concentration introduce an asymmetric risk that affects total-cost-of-ownership versus geared alternatives.

Technology and scale are converging. Suppliers are introducing higher-torque gearboxes and larger direct-drive machines simultaneously. Test-rig capacity, prototype validations and field installs completed in 2024–2025 mean 2026 will be the year when many firms must choose whether to double-down on incremental gearbox innovation, pivot to PMDD investments, or pursue hybrid approaches.

Service and aftermarket economics are emerging as a decisive margin lever. As the installed base ages and turbine MW ratings increase, aftermarket services and retrofits become a high-return play for suppliers who can offer proven reliability and multi-brand capabilities.

Comprehensive market sizing and validated forecast model for 2026–2032 at the system level (gearbox vs direct drive), with scenario outputs you can plug into corporate planning.

Technology roadmaps and comparative lifecycle-cost modelling, including CAPEX/OPEX sensitivities and maintenance profiles for key drivetrain architectures.

Supply-chain maps and risk heatmaps highlighting chokepoints (e.g., rare-earth upstream concentration, specialty steel supply and qualified test rigs), plus mitigation levers—nearshoring, inventory strategies, and long-term contracts.

Competitive benchmarking and supplier scorecards with strategic positioning, manufacturing footprints, service capabilities and modular product strategies.

Commercial playbooks for OEMs, tiered suppliers and investors: sourcing decision trees, local-content scenarios, and contracting templates tailored to mid- and large-scale projects.

M&A and partnership diagnostics—identifying where bolt-on acquisitions, JV structures or licensing deals deliver the fastest path to capability or market access.

Operational tools: Excel-based forecast model, supplier selection matrix, and a prioritized risk register for board-level review in 2026.

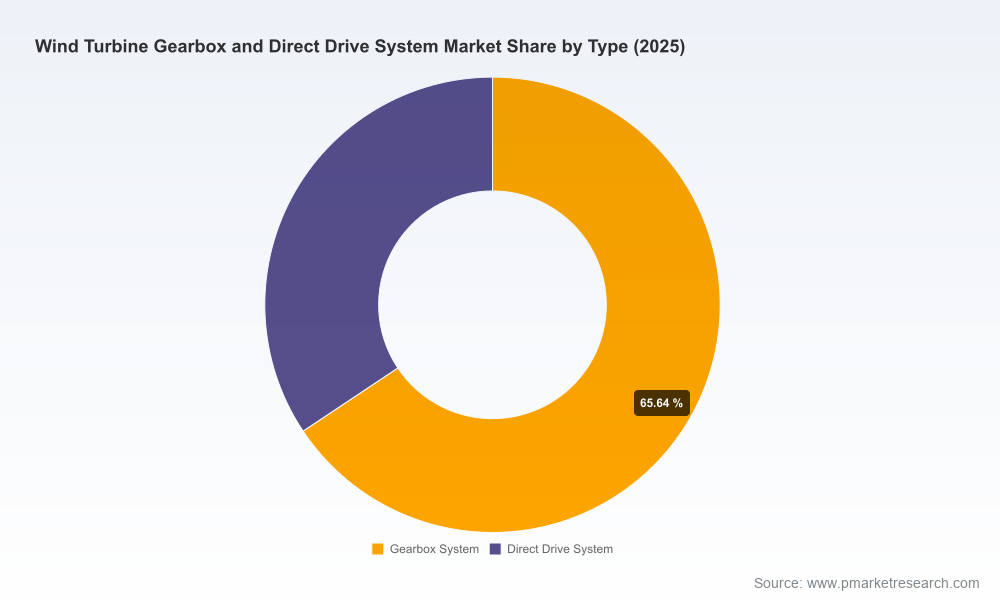

The market remains moderately concentrated; the top three players account for a majority share of system shipments, while the top five command a significant portion of revenue—factors that shape pricing power and OEM supplier strategies. Our vendor assessments combine product architecture analysis, recent investments, and service footprints to clarify who will be advantaged as the market bifurcates between high-torque-density gearboxes and large-scale direct drive platforms.

ZF Friedrichshafen AG — ZF’s modular SHIFT platform and investments in large-scale testing position it to defend and expand share in both onshore and offshore gear-driven segments. Its emphasis on torque density and validation capacity is a key differentiator for OEMs seeking to minimize field risk when scaling turbines.

Winergy Group (Flender) — Recent product launches focused on high torque-per-weight concepts signal a strategy of squeezing the gearbox’s performance envelope to remain competitive with direct drive alternatives while preserving established supply and service relationships.

Moventas — With a heavy focus on service and aftermarket solutions, Moventas is well placed to capitalize on the growing aftermarket revenue pool, especially where operators prioritize lifecycle reliability and multi-brand support.

Chinese gearbox manufacturers (e.g., NGC Transmission, Chongqing Gearbox) — These players continue to provide cost-competitive, high-power solutions for rapidly growing domestic and export markets. Their scale and proximity to fabricators give them advantages on unit cost, but geopolitics and trade policy will influence export viability.

Specialist and regional players (e.g., Eickhoff, Ishibashi) — Focused on robust designs for demanding environments, these firms compete on durability and niche engineering expertise rather than scale alone.

Direct drive pioneers (e.g., ENERCON, Goldwind, Siemens Gamesa, GE Vernova, Mingyang) — Each pursues slightly different PMDD strategies: ENERCON emphasizes gearless annular machines, Goldwind and Mingyang push large-scale offshore PMDD platforms with extended-life designs, and western OEMs combine direct-drive options with broad service networks for offshore megaprojects. Recent product launches and large-platform installations in 2024–2025 indicate a continued acceleration of DD capability.

Product introductions and prototype demonstrations through 2025 indicate accelerating performance improvements for both gearbox and direct drive platforms; expect validation and supply readiness debates to migrate from R&D forums to procurement negotiations in 2026.

New large-scale test rigs and onshore/offshore prototype installations established in 2024–2025 shorten time-to-market for advanced designs and raise the bar for demonstrable reliability during contractual due diligence.

Regulatory and trade interventions announced in 2025 create immediate implications for sourcing and cost pass-through. Executives must incorporate tariff sensitivity into procurement contracts and consider dual-sourcing or nearshoring as contingency measures.

Price volatility in rare earths and the geographic concentration of magnet supply mean direct drive economics will remain sensitive to upstream dynamics unless supply diversification or recycling measures scale rapidly.

Our scenario framework maps three plausible 2026 decision contexts for drivetrain strategy:

Base case — steady demand growth consistent with a mid-single-digit CAGR (our central projection) where both gearbox and direct drive continue to co-exist, and suppliers differentiate on reliability, service and platform modularity.

Tariff-upside risk — aggressive trade measures or tariffs increase landed component costs, favoring local manufacturing, simplified architectures and suppliers able to demonstrate localized supply chains.

Raw-material stress — sustained rare-earth price spikes or concentration-driven supply disruptions increase the effective TCO of PMDD, narrowing the economic case for direct drive unless mitigations (recycling, magnet-substitution, or diversified sourcing) are deployed.

Each scenario has quantified impacts in the full report: sensitivity tables, break-even points for gearbox vs direct drive, and recommended hedging actions that executives can adopt for 2026 planning cycles.

Prioritize supply-chain resilience over absolute unit cost when negotiating long-term procurement contracts; the risk of tariff or raw-material shocks has increased the value of flexibility.

Invest in service capability and multi-brand competence—aftermarket revenues and retrofit opportunities will underpin margins as machines grow larger and remain in the field longer.

Adopt a portfolio approach to drivetrain technology: retain optionality between high-torque gearboxes and PMDD systems until field-level reliability and upstream cost trends conclusively favor one path.

Pursue targeted partnerships or minority deals to secure access to specialized magnet supply, advanced testing capacity, or localized manufacturing when entering politically sensitive or tariff-exposed markets.

Embed scenario-conditioned clauses in supplier contracts and EPC agreements—indexation to material costs and clear escalation mechanisms will be a differentiator in project bankability discussions.

PW Consulting’s report is designed as a decision-ready toolset rather than a descriptive summary. Together with the written analysis, clients receive the underlying forecast model, supplier scorecards, and a tactical playbook that enables board-level rehearsals and procurement negotiations. For organizations evaluating strategic shifts—whether re-shoring gearbox lines, investing in PMDD capability, or monetizing aftermarket services—our advisory engagements can fast-track diligence, supplier selection and commercial negotiation.

To access the full segmentation tables, scenario modelling outputs, and supplier-level financials that underpin these strategic recommendations, please visit the report landing page and request the complete dataset. The headline numbers and playbook above are intended to orient 2026 strategy; the full report supplies the segment-level visibility required to execute it.

For detailed analysis of this topic, please visit the official page:Wind Turbine Gearbox And Direct Drive System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com