A Strategic SWOT and PESTLE for the Epon Olt Market Analysis Sector

Other |

2026-06-23 10:51:42

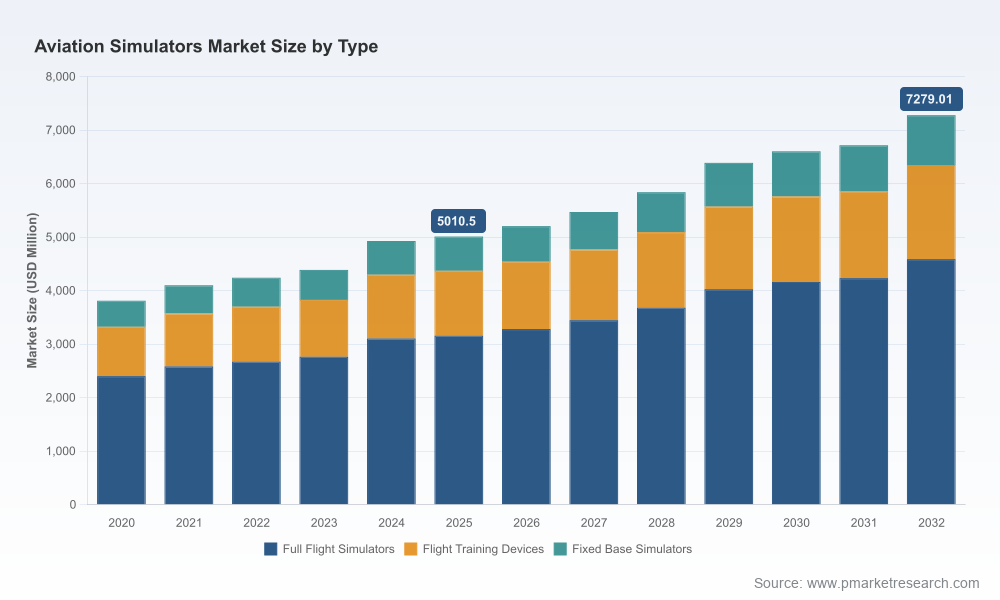

PW Consulting’s latest Aviation Simulators Market report provides a sharp, decision-grade view for executives, investors, and program managers preparing to allocate capital, sign contracts, or pivot product strategy in 2026. The global market for aviation simulators has expanded materially over the past five years — from approximately USD 3.81 billion in 2020 to USD 5.01 billion in 2025 — and is forecast to continue growing through our 2026–2032 horizon at a compound annual growth rate (CAGR) of 5.48%, reaching roughly USD 7.28 billion by 2032. This briefing summarizes the report’s strategic value, highlights the most consequential industry dynamics, and previews the competitive implications that will shape procurement and investment decisions this year.

Aviation Simulators Market

Timing for CapEx and Fleet Training Programs: 2026 is a pivotal year for many fleet renewal cycles and training academy expansions. Our modeling identifies where simulator demand will concentrate and when lead times create near-term scarcity — critical for procurement scheduling and RFP timing.

Aviation Simulators Market

Technology transition and certification windows: Regulators and qualification bodies have accelerated acceptance of mixed reality and VR-based training devices. Understanding the certification pathways and realistic deployment timelines is essential before committing to a platform or supplier.

Aviation Simulators Market

Competitive positioning and partnership strategy: Market concentration metrics in the report (CR3 and CR5 analyses) reveal consolidation dynamics that affect pricing leverage, delivery risk, and after-sales support strategies for buyers and OEMs alike.

M&A and service expansion insights: For private equity and corporate development teams, the report exposes niches where technology entrants or regional integrators can scale through bolt-on acquisitions or strategic alliances.

Robust market-sizing and forecasting methodology: We transparently document our base-year calibration (2025), historic trend reconciliation (2020–2025), and scenario-based forecasts (2026–2032). The report explains assumptions behind demand drivers — airline pilot hiring plans, defense training budgets, general aviation activity, and the rise of eVTOL and urban air mobility training needs.

Actionable procurement templates: Standardized procurement checklists, risk matrices for simulator delivery and qualification, and contract clause recommendations (warranties, performance acceptance criteria, spares, and upgrades) designed to shorten negotiation cycles and protect buyer interests.

Technology roadmaps and certification pathways: Comparative analysis of Level D FFS, Level-certified FTDs, fixed-base, and XR/VR solutions, including realistic deployment timelines tied to FAA/EASA qualification milestones and reciprocal acceptance mechanisms that can reduce duplicate validation work.

Vendor due-diligence frameworks: A repeatable scorecard covering technical capability, delivery track record, TCO and lifecycle support, software update cadence, and cyber/IT integration risk for training centers.

Commercial models and TCO calculators: Side-by-side total cost of ownership templates for ownership vs. managed services (training-as-a-service), with sensitivity analyses on utilization rates, maintenance cycles, and motion-platform replacement intervals.

Scenario playbooks for executives: If/then pathways for deploying simulators under alternate futures — e.g., accelerated eVTOL certification uptake, a moderate defense procurement uptick, or constrained supply-chain conditions — enabling rapid reprioritization of budgets.

Certification is evolving. EASA’s longstanding CS-FSTD standards and ongoing FAA qualification updates remain the baseline for device acceptance, but regulators are formally recognizing mixed reality and high-fidelity VR devices. Recent qualifications in the MR/VR space demonstrate the path to operational use, shortening the time between prototype and approved training tool.

Reciprocal acceptance and BASA-style arrangements matter. Mutual recognition frameworks reduce duplicate qualification costs across major jurisdictions — a pragmatic lever for global airlines and multi-site training providers to optimize fleet training rollout.

Level D remains the gold standard for upset recovery and full-mission simulator needs, but lower-cost, higher-flexibility XR solutions are rapidly maturing for procedural and multi-crew cooperation tasks. The report quantifies where XR substitutes are commercially viable and where they are not.

The market exhibits a concentrated vendor structure where the top tier holds a majority share of installed high-fidelity FFS platforms. Our CR3 and CR5 analysis shows significant but not complete concentration, creating competitive spaces for both incumbent expansion and disruptive entrants.

CAE Inc. (Montreal) — a global leader across civil and military simulation. CAE’s product line, including high-fidelity full-flight simulators, XR flight training devices, and specialized eVTOL simulators paired with advanced visual systems, positions it strongly across commercial and emerging urban mobility segments. Recent deliveries and strategic partnerships underscore CAE’s ability to convert R&D into deployable training infrastructure.

FlightSafety International (Columbus, Ohio) — a major integrator of training centers and high-fidelity simulators. Its deep operations in pilot training and broad service footprint make it a natural partner for airlines looking to secure training capacity as they ramp pilot throughput.

L3Harris Technologies (Melbourne, Florida) — continues to provide A320-family and other FFS platforms with strong engineering pedigree in defense-related simulations. Note: commercial aviation solutions business restructuring in 2025 changes go-to-market profiles for certain product lines.

Thales Group (Paris) — focused on helicopter and fixed-wing FFS platforms, with strength in defense and civil sectors where integrated avionics and simulation fidelity are mission-critical.

TRU Simulation + Training (Tampa) — offers innovative form-factor options (e.g., roll-on/roll-off suites) and serves large OEM-integrated programs, including long-haul aircraft training suites.

Specialists and challengers — Frasca, Indra, HAVELSAN, Loft Dynamics, Elite Simulation Solutions, and SIMCOM — represent an active mid-market and specialist layer. These firms compete on niche performance characteristics, lower TCO offerings, or specialized platform expertise (e.g., general aviation, rotary wing, regional types, or VR-certified devices).

Recent product and certification events exemplify market momentum and near-term tactical considerations: a major OEM’s 777-9 simulators achieved initial FAA/EASA qualification in early 2026, a regional PC-12 training device received dual FAA/EASA FTD certifications in 2026, and CAE delivered its first eVTOL simulator to a pilot academy in 2026. These developments create immediate demand signals for training capacity and second-order effects on maintenance, instructor hiring, and software integration.

For airlines and training academies: prioritize early engagement on delivery slots and qualification support. Simulators — especially high-fidelity suites — have multi-month to multi-year procurement-to-qualification cycles; misaligned timing can force expensive interim solutions or training bottlenecks.

For OEMs and systems integrators: adopt modular upgrade paths and clear certification support packages. Buyers increasingly value upgradeability (visual systems, motion cueing, synthetic training environments) to protect asset value.

For defense procurement planners: balance in-house capability development with supplier partnerships that provide sovereign control over critical training content and baselined hardware support.

For investors and corporate development teams: the market’s mid-tier and specialist layer represents attractive bolt-on targets, particularly firms offering certified VR/XR platforms, niche rotary-wing expertise, or unique delivery models (e.g., managed simulator services).

Decision-ready outputs: procurement timelines, vendor scorecards, and TCO models that can be used directly in board-level CapEx approval memos.

Risk checklists: supply-chain, certification, and operational readiness risks mapped to mitigation actions with ownership assigned for rapid implementation.

Custom scenario workshops: tailored sessions we run with executive teams to convert forecast scenarios into 90–180 day action plans for procurement, training capacity, and vendor engagement.

PW Consulting’s Aviation Simulators Market report is designed as a strategic tool for 2026: to shorten decision cycles, reduce procurement risk, and align technology choices with certification realities. This release outlines the report’s depth while preserving the full segmentation and granular vendor benchmarking for subscribers and authorized purchasers. For immediate implementation support, our consultants are scheduling limited advisory engagements to help clients convert insights into executable procurement and deployment plans.

To access the comprehensive dataset, segmented forecasts, and supplier-level deliverables, visit our official report page. The full report contains detailed regional and application-level breakdowns, supplier scorecards, and downloadable TCO models that are intentionally withheld from this briefing to encourage direct engagement and to ensure clients receive the complete, copyrighted analytical package.

For detailed analysis of this topic, please visit the official page:Aviation Simulators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com