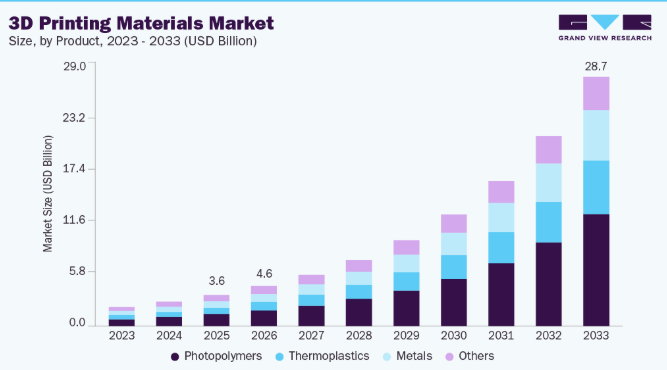

3D Printing Materials Market Trends Influencing Smart Factory Development

Other |

2026-05-25 04:38:30

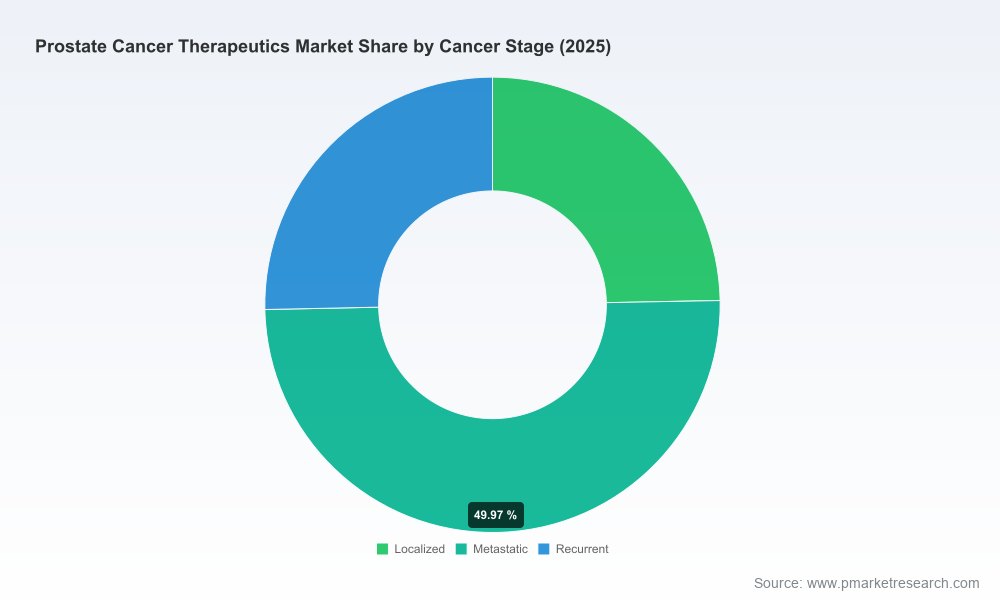

PW Consulting’s latest market intelligence on Prostate Cancer Therapeutics frames 2026 as a pivotal year for biopharma strategists. Built on a rigorous base-year analysis (2025) and a consolidated forecast through 2032, the report synthesizes commercial, clinical, regulatory and reimbursement forces that will determine winners in a market expanding at a mid-to-high single-digit trajectory. Our headline: the global prostate cancer therapeutics market—measured at an estimated USD 18,500 Million in 2025—is projected to grow to just over USD 31,400 Million by 2032, reflecting a compound annual growth rate (CAGR) of 7.85% across the forecast horizon.

Prostate Cancer Therapeutics Market

Regulatory momentum and new approvals. Late‑stage approvals and label expansions in 2025–2026 have moved targeted agents and PARP inhibitors into earlier lines of therapy, while radioligand therapies have transitioned from niche to mainstream in higher‑risk populations. These shifts recalibrate addressable populations and create new standards of care that will guide near-term trial design and commercialization models.

Prostate Cancer Therapeutics Market

Payer pressure and price dynamics. The intersection of high-cost innovation with intensified payer review is reshaping commercial playbooks. Negotiation programs and value frameworks are accelerating adoption of outcomes-based contracts, earlier real-world evidence (RWE) investments, and portfolio hedging against pricing volatility.

Prostate Cancer Therapeutics Market

Competitive concentration. Market concentration remains substantial: the top three players collectively command a majority share of the market (our CR3 estimate is 58.4%), and the top five reach more than three quarters (CR5 at 76.5%). This structure favours scale players able to integrate R&D, global commercialization and complex supply chains, while opening niches for focused innovators with differentiated mechanisms.

Our report is designed for senior decision-makers who require executable insights rather than high-level summaries. PW Consulting provides:

Independent market sizing and forward-looking scenarios that stress-test uptake under alternative reimbursement and competitive assumptions.

Pipeline and clinical-readout tracker aligning mechanism-of-action with likely commercial impact, launch sequencing and dose/regimen dynamics.

Regulatory and reimbursement mapping, including timing implications for label expansions and anticipated payer policy responses.

Commercial benchmarking and go-to-market playbooks for incumbent leaders and emerging entrants—addressing pricing, access, channel strategy and diagnostic co‑deployment.

M&A and partnership opportunity framework with playbooks for inorganic growth (bolt-on vs platform) and risk-calibrated valuation approaches.

Note: To maintain the “trailer” principle that drives strategic engagement, the report presents full segmentation tables, regional and indication splits, and granular revenue curves behind paywall access. The executive summary here omits those core split data points to encourage direct engagement with the full dataset.

The competitive field combines large integrated pharmas and smaller specialty companies with differentiated platforms. Key strategic moves to watch (and modeled in our scenarios) include:

Johnson & Johnson (Janssen): Multi-modal positioning across hormonal agents, PARP combinations and bispecific antibodies. Recent M&A activity and early clinical signals for novel bispecifics position the company to defend and extend incumbent franchises.

Astellas and Pfizer: The Xtandi collaboration remains strategically important as the product faces lifecycle pressures. Co‑development efforts with next‑generation AR pathway inhibitors and combination strategies with targeted agents are central to their defense playbooks.

AstraZeneca and Novartis: Heavy emphasis on precision radioligand and PARP-oriented strategies; platform acquisitions and radiopharmaceutical investments are recession‑proofing future oncology revenue streams.

Bayer, Sanofi, Merck, Eli Lilly and other major biopharmas: Each is balancing classic cytotoxic/hormonal assets with specialty investments in radioligands, immuno-oncology and targeted agents—creating multiple vectors for strategic partnerships.

Specialists and innovators (Dendreon, Exelixis, Telix, Lantheus, pharmaand, Ipsen): These players are the incubators for differentiated approaches—autologous immunotherapy, next‑gen radiopharmaceuticals, and biomarker‑driven therapies—that incumbents will seek either to license or to acquire.

Our competitive modules model different defensive and offensive scenarios: (1) incumbents deploying lifecycle management and combo regimens, (2) partnership-led expansion of radioligands and diagnostics, and (3) nimble entrants targeting tightly defined biomarker niches. Each scenario has distinct implications for capex, supply chain readiness and payer negotiation timelines.

Regulatory expansions for genetically targeted agents have altered therapeutic sequencing. Approval of new combinations and regular approvals for PARP inhibitors shift clinical practice—forcing label-driven diagnostic rollouts and earlier testing adoption. These developments increase the commercial importance of companion diagnostics and multi-gene panels.

Payer interventions and negotiated pricing mechanisms are accelerating the need for robust RWE and outcomes-based agreements. Manufacturers should prioritize early‑launch RWE programs and flexible contracting capabilities to mitigate payer scrutiny and secure formulary access.

Patent cliff timing for foundational androgen receptor inhibitors introduces near-term generics risk. Firms must weigh defensive patent strategies, authorized generics, and rapid launch sequencing for next‑generation agents to protect lifetime value.

Translating clinical promise into commercial success requires disciplined operational planning:

Supply chain and manufacturing scale-up for radiopharmaceuticals: Radionuclide therapies require unique manufacturing footprints and cold-chain logistics. Investment decisions must consider regional capacity constraints and partner networks for isotope supply.

Diagnostics and testing ecosystems: Uptake of PARP inhibitors and other biomarker-dependent therapies is contingent on accessible genomic testing. Companies should consider co‑funding testing programs, laboratory partnerships, and point-of-care logistics as part of launch planning.

Commercial capability evolution: Field teams will need to shift from broad oncology detailing to highly targeted, multi-stakeholder engagements that include nuclear medicine, urology, and molecular diagnostics stakeholders.

Revisit portfolio prioritization with scenario-based NPV models that incorporate potential price renegotiation and generic erosion timelines.

Accelerate partnerships for radioligand manufacturing and distribution to de‑risk time-to-market for late-stage assets.

Embed payer and health‑economics expertise into early development to design trials that generate both regulatory and reimbursement-relevant endpoints.

Invest in biomarker access programs and diagnostic reimbursement strategies to maximize addressable patient populations at launch.

Establish an M&A scouting process focused on platform technologies—RIPTACs, bispecifics, PSMA-directed radiopharmaceuticals and companion diagnostic providers—with a pre-defined integration playbook.

For executives preparing 2026 strategies, the immediate priorities are clear: shore up defenses for high-value, at-risk franchises; accelerate development and commercial readiness for precision and radioligand therapies; and build payer-credible evidence programs that support differentiated value propositions. Tactical execution should be informed by scenario-tested financial models and a playbook for rapid operational scale-up.

PW Consulting’s full Prostate Cancer Therapeutics Market report delivers the granular data, company-level deep dives, and actionable models required to execute on this agenda. The public summary above intentionally omits the detailed segmentation, regional and application splits and tabulated revenue forecasts that underpin our recommendations—these are available in the full report and interactive data package.

Professionals seeking the complete dataset, company profiles, clinical timelines and tailored advisory support for 2026 planning can access the full report and client engagement options through PW Consulting’s research portal.

For detailed analysis of this topic, please visit the official page:Prostate Cancer Therapeutics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com