Tungsten Heavy Alloy Shielding Market Set to Hit USD 0.92 Billion by 2034 at 6.6% CAGR

Networking |

2026-07-01 13:27:25

PW Consulting’s latest Artificial Lens Market intelligence brief offers a forward-looking strategic lens for executive teams preparing decisions in 2026. Built on a rigorous base year of 2025, five years of historical traction (2020–2025) and a seven-year forecast horizon (2026–2032), the report synthesizes market sizing, technology evolution, competitive positioning, regulatory and reimbursement shifts, and pragmatic go-to-market playbooks. Our independent modelling shows the global market expanding from a 2025 baseline into the late 2020s at a compound annual growth rate of approximately 5.48%, reflecting steady demand for cataract and refractive lens solutions and continued premiumization of intraocular lens (IOL) portfolios.

Artificial Lens Market

Timing and resource allocation: 2026 is a pivotal year for portfolio launches and clinical investments. Several regulatory milestones and product approvals have reset competitive dynamics and reimbursement calculus — making near-term timing decisions more consequential for market share and margin trajectories.

Artificial Lens Market

Capital deployment and M&A: With moderate but sustained market growth and a high degree of market concentration (top-three players controlling the majority share and top-five even more), acquisitive strategies must balance scale-driven access to premium segments with targeted bolt-on technologies and regional distribution gaps.

Artificial Lens Market

Commercial rigour: Reductions in some facility reimbursement drivers and new procedural codes require a re-evaluation of pricing, value dossiers and channel incentives—especially for manufacturers relying on ambulatory surgery centers and physician-owned channels.

Our modelling indicates the global artificial lens market is growing steadily through the forecast horizon. The growth profile combines demographic tailwinds (aging populations in core markets), rising uptake of premium optics and EDOF/trifocal solutions, and incremental expansion in refractive implant categories. The market is mid-sized but strategically attractive: concentration metrics show significant leadership by a handful of diversified ophthalmic manufacturers, with three firms accounting for a dominant share and five firms controlling an even larger portion — a structure that rewards scale, clinical trust, and distribution breadth.

Importantly, the rate of growth (c.5.5% CAGR across 2026–2032) is sufficient to create meaningful value for product innovators and efficient incumbents, but not so rapid as to make executional excellence secondary. This is a market where clinical differentiation, evidence generation and optimized reimbursement strategies win more reliably than volume-only plays.

Reimbursement pressure in ambulatory settings: In the U.S., the ASC payment rule established for 2026 has altered economics for cataract procedures. Payers and facilities are adjusting to a lowered per-procedure payment, which has implications for lens mix negotiations, capital equipment prioritization and bundled-care proposals.

New coding pathways: The introduction of new CPT code constructs related to intraocular prosthesis fixation presents opportunities for innovators to capture differentiated procedure-level reimbursement, provided they can demonstrate distinct clinical value and coding compliance.

Clinical evidence bar is rising: Recent approvals for premium and EDOF platforms underscore the regulatory expectation for robust contrast sensitivity, defocus curve and real-world functional outcomes. Manufacturers should prioritize randomized and longitudinal studies that align with both regulatory endpoints and payer value narratives.

The competitive landscape blends long-established global leaders with nimble regional specialists. A concise synthesis of strategic positioning follows — emphasising implications rather than exhaustive product listings.

Global platform leaders: Multinational manufacturers with broad portfolios and deep surgical relationships continue to set the clinical standard. Their strength lies in integrated product ecosystems (premium optics, surgical viscoelastics, and disposables), expansive R&D pipelines, and established reimbursement dossiers. Expect continued investment in premium EDOF and trifocal enhancements as a defensive and growth strategy.

Specialist innovators: Niche companies focused on advanced optics, materials science or phakic solutions are capturing share by addressing specific unmet needs — for example, options for younger refractive patients or designs that minimize contrast sensitivity loss. Their pathway to scale typically requires distribution partnerships or favorable reimbursement carve-outs.

Regional players: Companies rooted in particular geographic markets are leveraging local hospital relationships, cost-advantaged manufacturing and regulatory familiarity to defend mass-market monofocal volumes and selectively compete in premium tiers where clinical differentiation exists.

Recent regulatory events in early 2026 have already changed competitive calculus: industry-leading firms secured approvals for new EDOF and full-range IOLs, and other manufacturers achieved first-in-market implantations of newly approved premium trifocal devices. These events not only validate premium categories but also raise the importance of post-market evidence and surgeon training programs to accelerate adoption.

This brief is an executive teaser of a larger report designed for leadership teams who need to convert market intelligence into decisions. The full PW Consulting Artificial Lens Market report includes:

Detailed market sizing and forecast models (2020–2032) with sensitivity scenarios across adoption curves and pricing pathways;

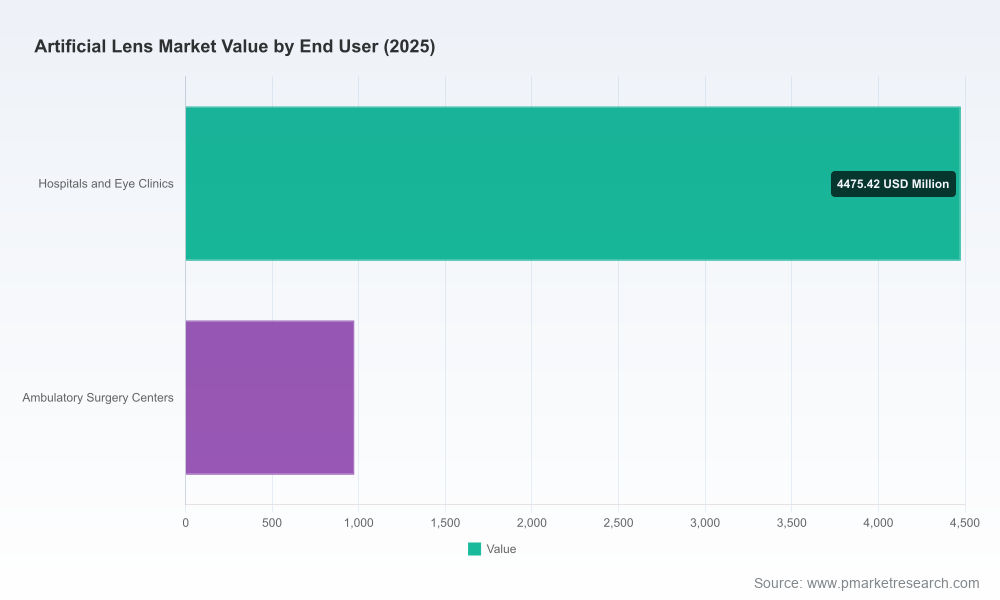

Segment-level diagnostic frameworks (product type, end-user channels and region) with layered demand drivers and bottlenecks. Note: the publicly available brief intentionally omits full disaggregation of segment dollar shares — these tables are available in the full report;

Competitive benchmarking with capability heatmaps, R&D pipeline synthesis, and commercial maturity assessments for the major firms active in the market;

Reimbursement and regulatory playbooks aligned to the latest coding and payment changes, including modelled impacts on procedure economics and product-level pricing levers;

Go-to-market toolkits tailored to 2026 realities: launch sequencing guides, KOL engagement frameworks, surgeon training pathways, hospital system contracting templates and real-world evidence (RWE) strategies;

M&A and partnership scouting: prioritized target lists and valuation sensitives for bolt-on optics, digital surgical planning tools and regional distribution platforms;

Operational risk assessments covering supply-chain exposure, capacity constraints for specialty materials, and mitigation options for maintaining sterile manufacturing continuity.

For executives preparing 2026 plans, the following moves warrant immediate consideration:

Re-assess launch timing and evidence generation budgets. Where premium approvals exist, accelerate real-world outcome collection to support payer engagement and surgeon preference formation.

Reconfigure commercial incentives to reflect shifting facility economics. Consider bundled service propositions and shared-savings pilots with ASC networks to mitigate downstream price pressure.

Prioritize partnerships over greenfield entry in markets where regulatory and distribution complexity is high. Strategic alliances can accelerate scale without proportionate upfront capex.

Invest in surgeon education and digital surgical planning tools that demonstrably reduce variability in refractive outcomes — these investments increase premium lens uptake and defend against commoditization.

Embed reimbursement scenario planning into product valuation models. Given recent U.S. payment updates, small shifts in procedure economics materially change ROI timelines for premium IOLs.

Plan M&A diligence around assets that either fill clinical gaps (e.g., true EDOF trifocal hybrids) or substantially reduce cost of goods for commoditized monofocals.

The report’s core models use a bottom-up approach calibrated against device shipment data, clinical adoption rates, procedure volume forecasts and pricing trajectories in USD (revenue unit: Million). Historical data covers 2020–2025 with 2025 serving as the base year; forecasts extend from 2026 through 2032 under a central (base-case) CAGR of ~5.48%. Concentration metrics were derived from firm-level reported revenues and independent market checks.

To maintain the integrity of our strategic preview and respect commercial sensitivity, detailed segment-dollar tables and country-by-country breakout are reserved for subscribers to the full report. This selective disclosure follows our “trailer” principle: it provides enough analytical depth to inform executive judgement while channeling operational teams to the full dataset for transactional and tactical decisions.

PW Consulting offers targeted advisory engagements to translate the report’s insights into executable plans: scenario modelling workshops, reimbursement dossier development, commercial launch roadmaps, and M&A diligence support. For firms preparing capital allocation, the combination of our sizing dashboard and competitive playbooks helps prioritize investments with a clear path to accretive returns.

To access the complete Artificial Lens Market report — including full segment disaggregation, interactive models and proprietary competitive matrices — please visit PW Consulting’s market research portal or contact our strategy desk for a customised briefing and data package tailored to your requirements.

For detailed analysis of this topic, please visit the official page:Artificial Lens Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com