The Future of Email Marketing Through an Accessible Email Design Guide Framework

Other |

2026-06-12 08:12:00

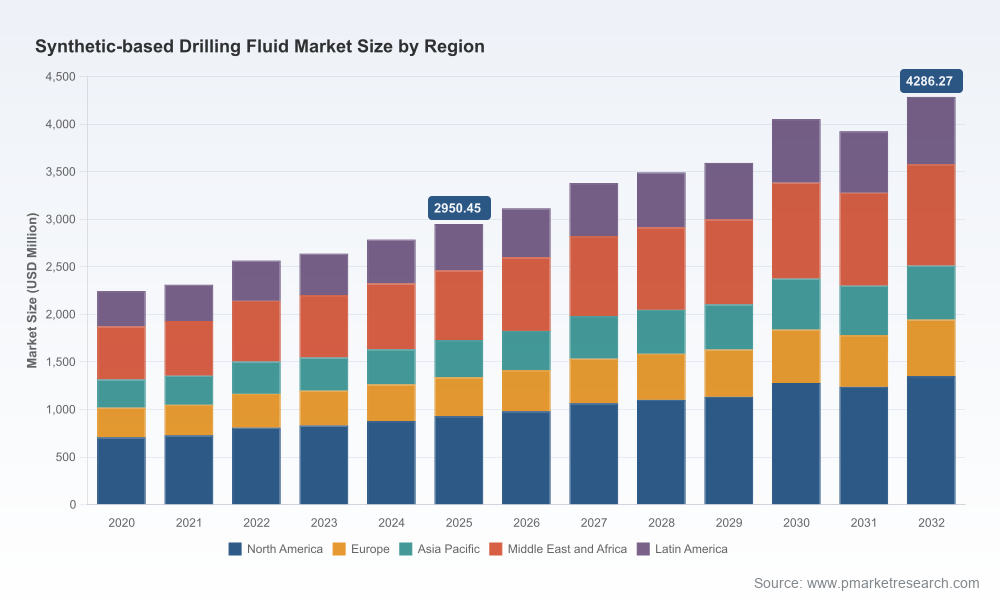

PW Consulting's latest market study on Synthetic Based Drilling Fluids (SBDFs) synthesizes five years of historical performance (2020–2025) and delivers a forward-looking, decision-ready roadmap for 2026–2032. The global SBDF market, which we estimate at approximately USD 2,950 million in our 2025 base year, is projected to expand at a compound annual growth rate (CAGR) of 5.48% through the 2026–2032 forecast window — reaching an estimated market scale in 2032 that materially reshapes investment and operational priorities for suppliers, operators and midstream partners alike.

Synthetic Based Drilling Fluid Market

Clarity under volatility: Operators and suppliers are navigating simultaneous shocks — raw-material supply disruptions and tightening environmental regimes — that change the economics of SBDF formulations. Our report translates market momentum and these shocks into concrete scenarios that inform capital allocation, contract negotiation and product roadmaps.

Synthetic Based Drilling Fluid Market

Actionable regulatory foresight: With jurisdictions updating discharge limits and trade measures, compliance is now a business differentiator. We map how tightened discharge permits and new border-adjusted tariffs shift the breakeven for different fluid chemistries and manufacturing geographies.

Synthetic Based Drilling Fluid Market

Competitive positioning: The market displays measurable concentration (CR3 ~48.6%; CR5 ~66.45%), meaning a relatively compact group of incumbents drive technology and procurement norms. The report translates concentration dynamics into playbooks for challengers and incumbent defense strategies.

Commercial signaling for procurement and pricing: As feedstock and base-stock costs have oscillated recently, purchasing teams require an integrated cost-to-serve and pricing sensitivity framework to protect margins while remaining competitive on tenders and service contracts.

Raw-material price pressure: Key feedstocks for SBDFs have experienced meaningful cost inflation linked to upstream petrochemical tightness. Linear alpha olefins (LAOs) and polyalphaolefin (PAO) base stocks have shown notable price moves that compress formulation economics and favour either higher-value differentiated products or vertically-aligned sourcing strategies.

Regulatory tightening: North American and European regulatory updates — from renewed discharge permit limits to trade measures that internalize carbon costs — are shifting where and how fluids can be blended, used and exported without incurring material compliance costs or delays.

Operational demand mix: Offshore deepwater programs, high‑pressure high‑temperature (HPHT) wells and extended‑reach onshore developments continue to create demand for specific SBDF performance attributes (biodegradability, lubricity, shale inhibition). The marginal value of formulation performance versus cost is increasing in tender evaluations.

Robust market model — a transparent, auditable demand-supply model covering 2020–2032 that integrates historical activity, rig counts, and project pipelines to generate a probability-weighted forecast. The model is parameterised so commercial teams can run sensitivity cases against feedstock price and regulatory inputs.

Regulatory impact matrix — jurisdiction-by-jurisdiction mapping of permit regimes, anticipated policy shifts and tariff exposures, paired with mitigation options (e.g., formulation swaps, localized blending, certification pathways).

Cost-to-serve and margin playbooks — unit-economics templates for different blending footprints and channel models (direct-to-operator, distributor-led, integrated services) that help commercial teams set thresholds for bids and long-term contracts.

Competitive intelligence dossiers — strategic profiles on the major players, including product portfolios, recent investments, capability gaps and tactical moves observed in 2024–mid‑2026.

Decision-ready recommendations — prioritized near-term initiatives (0–18 months) and medium-term choices (18–48 months) for manufacturers, service companies and NOC/IOC procurement organizations.

Incumbent advantage and product differentiation: Major service companies continue to defend value through branded SBM solutions and performance claims. Examples include advanced ester-based systems and next-generation biodegradable formulations introduced by leading firms, which elevate regulatory compliance and permit access in sensitive waters.

Strategic moves to watch: Recent activity — new product introductions with improved biodegradability, OSPAR-compliant certifications, and regional capacity expansions — signal that incumbents are investing along three vectors: product sustainability, regional supply agility, and compliance-proofing. These moves raise barriers to entry in core offshore markets while creating niches for specialized suppliers.

Profiles in focus: The report includes concise, actionable assessments of market leaders and notable regional players — their core capabilities, go‑to‑market strengths, and vulnerabilities. These profiles highlight where partnerships, licensing or M&A can deliver rapid access to differentiated chemistries or localized blending networks.

Hedge and diversify feedstock exposure: Lock in strategic offtake with LAO/PAO suppliers, evaluate synthetic substitutes and co-locate blending near feedstock hubs to dampen margin volatility.

Accelerate low-toxicity formulations: Invest in R&D and certification pathways (e.g., OSPAR and equivalent regional approvals). Certification is increasingly a “table stakes” requirement for deepwater and environmentally sensitive tenders.

Localize to mitigate trade friction: Given border-adjustment measures affecting synthetic base oils, assess near-market blending or toll-blending partnerships in tariff-exposed regions to preserve competitiveness.

Reconfigure commercial contracts: Move from commodity-pricing to value-based contracting where formulation performance, reduced non-productive time (NPT) and environmental compliance are monetized in multi-year scopes.

Targeted inorganic moves: Pursue bolt-on acquisitions to acquire biodegradeable ester technology or regional blending capacity rather than broadscale consolidation; smaller, targeted transactions often yield faster integration and immediate commercial leverage.

Embed scenario-driven R&D prioritisation: Use sensitivity outputs — especially to feedstock price and discharge-regulation stress tests — to sequence R&D investments between high-performance/low-volume and lower-cost/high-volume formulations.

Baseline (our central view): Modest, steady demand growth under the reported CAGR; suppliers with compliance-ready portfolios and resilient feedstock contracts maintain margin stability.

Upside: Faster recovery in offshore deepwater capex and accelerated adoption of high-performance SBDFs; premium-priced biodegradable systems capture disproportionate value.

Downside: Prolonged feedstock tightness or broader regulation tightening increases cost of formulation ownership and compresses volumes as operators delay non-critical programs; this favours vertically-integrated players and low-cost formulators.

Product evolution: Several leading suppliers have launched or certified next-generation synthetics with improved biodegradability and frictional benefits — moves that increase access to regulated waters and strengthen tender positioning.

Capacity rebalancing: Strategic investments in regional blending capacity — for example to serve the Middle East and nearby deepwater projects — reflect a deliberate response to both demand concentration and feedstock logistics.

Commercial integration: Top service companies are packaging fluids with drilling optimization services to monetize performance gains (reduced NPT, improved ROP), moving buyer conversations from price per barrel to total well economics.

2026 is a hinge year for the SBDF industry. The combination of healthy market growth, concentrated supplier power, feedstock volatility and regulatory tightening creates both opportunity and risk. Firms that translate technical differentiation into certified, regionally-viable product portfolios — while de‑risking feedstock supply and embedding value-based commercial models — will capture outsized returns over the forecast period. PW Consulting’s report equips executives with the tactical model, regulatory mapping and competitive insights required to make those calls with confidence.

For the full data tables, detailed subsegment analysis, company dossiers and the scenario-modelling workbooks referenced in this summary, please visit the PW Consulting report page to access the complete Synthetic Based Drilling Fluid Market study and associated decision tools.

For detailed analysis of this topic, please visit the official page:Synthetic Based Drilling Fluid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com