Krill Oil Market CAGR Insights, Competitive Benchmarking and Forecast to 2033

Other |

2026-02-04 10:29:12

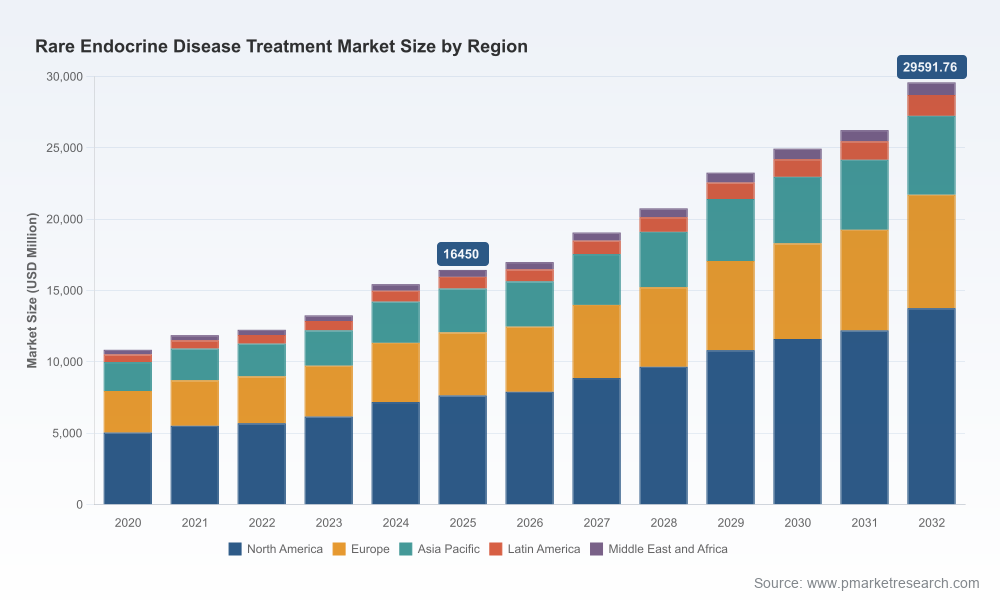

The Rare Endocrine Disease Treatment Market is entering a decisive expansion phase that will shape corporate strategies through the end of the decade. PW Consulting’s new market study — anchored on a 2025 base year, covering historical performance (2020–2025) and a forward-looking forecast window (2026–2032) — quantifies an accelerating growth trajectory with a compound annual growth rate (CAGR) of 8.75%. In dollar terms (USD, revenue unit: Million), the market is estimated at approximately 16.45 billion in 2025 and is projected to approach roughly 29.6 billion by 2032 under the central case.

Rare Endocrine Disease Treatment Market

For executives and strategy teams, the implications are clear: the near-term winners will be those that convert clinical innovation and regulatory momentum into durable commercial positions, while managing payer dynamics and shifting patient care models. This release outlines the strategic vantage points that matter in 2026 without disclosing the granular segmentation contained in the full report — to access the detailed regional, disease-type and therapy-level splits, please consult the full dataset on our website.

Rare Endocrine Disease Treatment Market

Growth is broad-based but nuanced. The market’s almost-doubling from mid-decade to 2032 is driven by a combination of recently approved therapies, late-stage pipeline readouts, and structural tailwinds from regulatory incentives (orphan designation, market exclusivity) that continue to de-risk investment in ultra-rare indications.

Rare Endocrine Disease Treatment Market

Transformative product profiles are changing treatment paradigms. The approval of once-daily oral somatostatin receptor ligands and the expanded pediatric labeling for long-acting growth hormone formulations are reducing treatment burden and creating new patient segments. These shifts favor companies that can match clinical differentiation with scalable manufacturing and patient support capabilities.

Payers are becoming more sophisticated. While orphan incentives sustain development economics, payers increasingly demand evidence of durable outcomes, real-world effectiveness, and clear value-based contracting pathways — particularly for novel modalities that command premium pricing. Companies must design reimbursement strategies in parallel with clinical development plans, not as an afterthought.

Concentration and competition. Market concentration metrics indicate a moderately concentrated market: the top three companies account for roughly 42% of market revenues, and the top five for about 59%. This structure creates room for focused specialists to achieve meaningful scale while leaving niches for new entrants with differentiated assets.

New approvals and label expansions: Recent regulatory events are reshaping addressable patient populations. Notably, the widening of pediatric indications for a once-weekly growth hormone in 2026 and approvals of oral and adjunctive therapies in previous years materially alter demand patterns across age cohorts and treatment settings.

First-in-class opportunities: The emergence of oral, once-daily treatments for traditionally injectable indications reduces adherence barriers and creates first-mover advantages. These shifts can accelerate patient conversion and justify differentiated pricing if supported by compelling outcomes.

Orphan and expedited pathways: Fast Track, orphan and other expedited designations continue to shorten time-to-market and extend commercial exclusivity windows. Companies that strategically leverage these pathways can materially improve the net present value (NPV) of development programs and attract partnership capital.

The competitive dynamic combines large multi-nationals with deep specialty portfolios and nimble biotechs delivering disruptive modalities. Primary companies we profile in depth include Ascendis Pharma, Novo Nordisk, Recordati Rare Diseases, Neurocrine Biosciences, Ipsen, Pfizer, Spruce Biosciences, AstraZeneca (Alexion), and a set of emerging specialists. Our analysis evaluates each on four strategic dimensions: clinical pipeline trajectory, commercialization capabilities, manufacturing and supply resilience, and payer engagement readiness.

Ascendis Pharma (Copenhagen): Known for its TransCon long‑acting platform, Ascendis has advanced programs across growth hormone deficiency and hypoparathyroidism. The company’s platform strategy creates optionality across therapeutic targets — a commercially attractive play if regulatory data confirms durable efficacy and safety.

Novo Nordisk (Bagsværd): With a recent expansion of pediatric indications for a once-weekly growth hormone in 2026, Novo Nordisk has strengthened its foothold in growth disorders. Execution will depend on effective pediatric market access strategies and the company’s ability to integrate new label expansions into existing supply and patient support networks.

Recordati Rare Diseases (Milan): A focused rare disease player with deep expertise in pituitary and adrenal dysfunctions. Its commercial agility and specialist networks remain an asset for high-unmet-need conditions where clinical nuance drives adoption.

Neurocrine Biosciences (San Diego): The approval of a novel adjunctive therapy for congenital adrenal hyperplasia marks a clinical and commercial inflection point. As the first new therapy in decades for select indications, the company faces the dual challenge of educating clinicians and designing reimbursement models that reflect additive value to standard care.

Ipsen and Pfizer: Both incumbents bring scale, distribution breadth and existing specialty portfolios that can be leveraged for incremental launches. Their strategic playbooks emphasize label lifecycle management and portfolio optimization.

Spruce Biosciences and MBX Biosciences: Small‑molecule and more targeted biotech entrants remain important sources of innovation. Their commercial success will depend on partnering strategies and the ability to secure favorable formulary placement against entrenched therapies.

AstraZeneca (Alexion): Advancing candidates for hypoparathyroidism with expedited designations, AstraZeneca is positioning to lead in this high-unmet-need niche — an example of big pharma applying M&A and development muscle to rare indications.

March 2026: Expanded pediatric approval for a once-weekly growth hormone materially increases the addressable pediatric growth disorder population and shifts therapy selection dynamics toward long-acting options. Immediate implications include supply planning, pediatric dosing strategies, and new adherence economics for payers.

September 2025: The approval of an oral once-daily somatostatin receptor ligand for acromegaly changes chronic care delivery for adult patients — reducing dependence on injectables and creating new competitive pressure on legacy therapies.

December 2024: The first new adjunctive therapy for congenital adrenal hyperplasia in decades demonstrates that regulatory appetite and clinical need can converge to re-open historically stagnant treatment areas.

Ongoing: Fast Track and orphan designations for hypoparathyroidism candidates underscore how regulatory incentives accelerate clinical development and commercial planning.

Our report is designed for senior leaders, corporate development teams, product strategy groups, and investor decision-makers who require both rigor and actionable recommendations. Key practical deliverables include:

Robust market model (2020–2032): Dynamic forecasts under base, optimistic and conservative scenarios with sensitivity testing for pricing, access and uptake assumptions. (Note: the public summary omits the full granular segmentation; the detailed model with regional, disease and therapy splits is available in the full report.)

Opportunity mapping: Pinpointed sub-indication and therapy niches where unmet need, payer willingness-to-pay and competitive intensity create attractive ROI profiles.

Commercial playbooks: Go-to-market strategies optimized for different company archetypes — global incumbents, specialty players, and biotech innovators — including partner selection criteria, launch sequencing and patient support program design.

Regulatory & reimbursement pathway analysis: Practical steps to leverage orphan and expedited designations, and templates for payer engagement that translate clinical differentiation into sustainable access.

Competitor dossiers and scenario-led M&A insights: Deep profiles of leading companies and a framework to evaluate strategic transactions, licensing or co-development opportunities.

Primary research evidence: Interviews with KOLs, payers and leading clinicians across major markets, enriching quantitative forecasts with real-world adoption signals.

Refine prioritization: Use our scenario outputs to rank programs by NPV across probable payer access timelines rather than headline prevalence or clinical novelty alone.

Align commercialization with clinical milestones: Stage market entry investments to coincide with label-enabling data that most influence payer decision-making (durability, safety, quality-of-life gains).

Pursue tiered access strategies: For premium therapies, construct phased rollout plans combining early access programs, outcomes data collection and value-based contracting pilots to demonstrate real-world value.

Prepare for competitive displacement: Monitor oral and long-acting entrants that reduce treatment burden and anticipate pricing dynamics by modeling best- and worst-case substitution scenarios.

The study integrates primary stakeholder interviews, KOL validation, proprietary demand modeling, and an exhaustive review of regulatory filings and clinical results. We calibrate assumptions with observed adoption curves for comparable specialty therapies and stress-test the model against macroeconomic and policy shifts. Currency is USD and revenue units are expressed in Millions. Detailed methodological notes and the full dataset are included in the paid report package.

By 2026, the rare endocrine market is no longer a niche sideline; it has become a strategic front where clinical innovation, regulatory incentives and payer scrutiny intersect. The path to market leadership requires more than an effective molecule — it requires an integrated approach across clinical development, evidence generation, payer strategy and commercial execution. PW Consulting’s Rare Endocrine Disease Treatment Market report equips leaders with the macro view, the tactical playbooks and the competitive intelligence needed to make confident investment and portfolio decisions for the rest of the decade.

For a complete view of regional, disease-type and therapy-level estimates, the detailed company dossiers, and access to the full financial model (2020–2032), download the full report from our website or contact the PW Consulting team to schedule a bespoke briefing tailored to your strategic questions.

For detailed analysis of this topic, please visit the official page:Rare Endocrine Disease Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com