Molecular Diagnosis Of Tumors Market: Strategic Imperatives for 2026 — PW Consulting Industry Brief

Executive summary

The molecular diagnosis of tumors market is entering a pivotal phase that will define competitive winners and losers through 2032. After a robust expansion from a mid‑single‑billion base in 2020 to an industry value of USD 9,450.5 Million in 2025, our diagnostic ecosystem is forecast to nearly double by 2032. PW Consulting’s analysis shows a compound annual growth rate (CAGR) of 11.25% over the 2026–2032 forecast window, driven by converging forces in precision oncology, regulatory recalibration, payer policy reforms, and rapid technological maturation in NGS, PCR, liquid biopsy and AI-enabled interpretation.

Molecular Diagnosis Of Tumors Market

Market trajectory and what it means for 2026 planning

Historical growth between 2020 and 2025 has been driven by widening clinical indications, expanded adoption of comprehensive genomic profiling and the increasing use of molecular tests to guide targeted therapies. With the base year set at 2025 and a forecast horizon running through 2032, PW Consulting projects the market to approach approximately USD 19,932.2 Million by 2032 under the central scenario. This trajectory implies sizeable addressable upside for product innovators, service providers and diagnostics laboratories — but with heightened strategic complexity.

Molecular Diagnosis Of Tumors Market

- Scale: The market size in 2025 establishes diagnostics as a multibillion‑dollar healthcare vertical with strong near‑term growth.

- Pace: An 11.25% CAGR to 2032 requires firms to accelerate commercialization and reimbursement strategies to capture share before commoditization pressures intensify.

- Concentration: Market concentration is meaningful but not prohibitive — the leading three firms account for approximately 38.5% of revenue, and the top five for roughly 52.8% — leaving a substantial middle market for specialist players and regional champions.

Why 2026 is a strategic inflection point

Several contemporaneous dynamics make 2026 the year to act decisively:

Molecular Diagnosis Of Tumors Market

- Regulatory tightening on Laboratory Developed Tests (LDTs). The FDA’s phased implementation of device regulation for many LDTs creates both compliance obligations and commercial opportunities for IVD-certified assays.

- Payer coding and coverage complexity. CMS MolDX program updates and stricter interpretation of CPT coding for NGS panels are raising reimbursement bar for comprehensive genomic profiling; providers must reconcile clinical utility evidence with payer expectations to secure coverage.

- New companion diagnostic approvals. The recent wave of approvals through 2025–2026 underscores accelerated co‑development between diagnostics and therapeutics, shifting the value capture map for diagnostics vendors.

Competitive landscape: patterns you must internalize

Competition is shaped by a mix of global platform vendors, specialized service labs, and AI-enabled analytics companies. The market architecture favors companies that can combine robust analytical performance, regulatory/quality credentials, payer engagement and integrated workflows for pathology and molecular labs.

- Large platform incumbents (e.g., Roche, Illumina, Thermo Fisher): These firms compete on breadth — instruments, IVD assays, and enterprise offerings for companion diagnostics and comprehensive genomic profiling. Their scale permits aggressive reagent economics, global lab partnerships, and bundled solutions for hospital systems.

- Specialized innovators (e.g., Guardant Health, Myriad, Caris): These players focus on differentiated propositions such as liquid biopsy, homologous recombination deficiency (HRD) assessment and integrated multi‑modal profiling tied to treatment selection and clinical decision support.

- Clinical lab networks and service providers (e.g., NeoGenomics, Exact Sciences): Their strengths lie in clinical adoption, end‑to‑end sample workflows and clinician relationships — all critical for driving test ordering and real‑world data generation.

- Enablers (e.g., Agilent, Danaher, Siemens Healthineers, Abbott, Bio‑Rad, Sysmex, Tempus): These companies provide assays, consumables, instruments and increasingly, software and AI pipelines that assimilate molecular outputs into clinical pathways.

Recent regulatory milestones illustrate these competitive dynamics: in 2025–2026 several notable companion diagnostics and IVD approvals validated both platform and test vendors’ strategies. Examples include regulatory approvals for comprehensive IVD assays and companion diagnostics across PD‑L1, HRD testing and tumor profiling platforms — events that materially shift market access and clinical adoption. PW Consulting’s report catalogs these actions and interprets their downstream impact on commercial positioning and product roadmaps.

Regulatory, reimbursement and coding — the operating environment

Executives must navigate a more prescriptive regulatory and reimbursement ecosystem in 2026:

- FDA LDT Final Rule: The shift toward device regulation requires long‑range compliance planning, including validation strategies, quality systems upgrades and potential re‑submission of legacy LDTs as regulated IVDs.

- Payer coding nuance: CMS and MolDX requirements increasingly demand DEX/Z‑code linkage alongside CPT submissions for coverage of molecular profiling. Additionally, the use of panel‑level CPT codes for NGS (e.g., codes for 5–50 gene and 51+ gene panels) changes revenue modeling and billing workflows.

- Companion diagnostic alignment: FDA‑cleared companion diagnostics tied to specific therapies will accelerate test uptake but require manufacturers to align clinical evidence generation with drug developers early in development cycles.

Report contents — what PW Consulting delivers to decision‑makers

Our Molecular Diagnosis Of Tumors Market report is structured as an execution toolkit for 2026. It combines quantitative market architecture with qualitative playbooks designed to be operationalized by commercial, strategy, regulatory and R&D teams. Key deliverables include:

- Market sizing and forecast model (historical 2020–2025, base year 2025, forecast 2026–2032) with scenario analysis and sensitivity testing linked to adoption, pricing and reimbursement levers.

- Competitive intelligence dossiers: company profiles, capability matrices, go‑to‑market positioning, and recent regulatory and M&A activity assessments.

- Regulatory and reimbursement playbook: practical steps for LDT‑to‑IVD transition, MolDX/CMS coding strategies, payer evidence generation templates and HTA engagement plans.

- Commercial and lab operational playbooks: sample throughput economics, turnaround time tradeoffs, central vs. decentralised testing strategies, and pricing negotiation levers.

- Technology roadmap and product prioritization: evaluation of NGS, PCR, ISH, microarrays, liquid biopsy and AI analytics across clinical and commercial metrics.

- M&A and partnership scoring: valuation frameworks and operator playbooks for inorganic growth, licensing and strategic alliances.

- Primary research appendices: interview excerpts with payers, lab directors, oncologists and procurement leads; methodological notes and data sources.

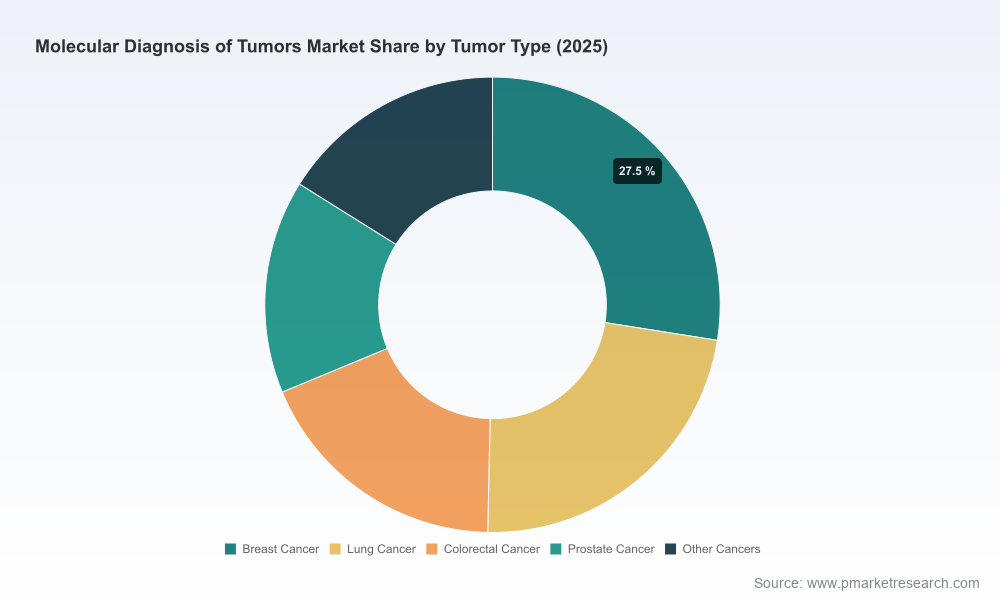

Note: In line with our “teaser” approach, granular segment tables (regional and tumor‑type breakdowns, technology splits and per‑segment dollar values) are summarized at a high level in this brief; full disaggregated tables, model access and downloadable datasets are available with the full report.

Actionable strategic recommendations for 2026

Based on our integrated analysis, PW Consulting recommends the following prioritized actions for market participants:

- Accelerate reimbursement readiness now. Invest in coding and claims teams, real‑world evidence generation and proactive MolDX engagements to secure coverage windows that will determine commercial viability.

- Pair regulatory and commercial timelines. For tests likely impacted by the FDA’s LDT rule, align IVD submission strategies with companion therapeutic timelines to preserve commercial exclusivity opportunities.

- Differentiate beyond the assay. Combine molecular outputs with workflow solutions, interpretation software, and clinician decision support to create stickier value propositions and defensible pricing.

- Optimize lab network strategy. Evaluate hybrid models that mix centralized high‑throughput testing for complex panels with decentralized rapid assays to serve acute decision points.

- Pursue targeted M&A to fill capability gaps. Smaller players should seek partnerships or bolt‑on acquisitions to consolidate sample access, reimbursement expertise or AI interpretation capabilities.

Risk scenarios and contingency planning

Our modeling surfaces three risk vectors that should be incorporated into 2026 operating plans:

- Reimbursement tightening: slower CPT/code acceptance or narrower coverage policies can compress short‑term revenue; mitigate via diversified payer strategies and outcome‑based contracting pilots.

- Regulatory delay: protracted IVD approvals may delay market entry for successor assays; build migration pathways and interim clinical utility communications for labs and oncology networks.

- Technological disruption: low‑cost, high‑throughput competitors or new multi‑omic offerings could reprice certain segments; maintain R&D vigilance and consider strategic partnerships to maintain relevance.

How to use this report in 2026 — quick playbook

Board members, corporate development teams and product leaders should use the report to:

- Recalibrate 2026 investment budgets against scenario‑based forecasts and expected reimbursement timelines.

- Prioritize partnerships with pharma and CROs to embed diagnostics early in therapeutic development programs.

- Design pilot projects that demonstrate clinical utility and economic value to payers, enabling faster coverage decisions.

- Benchmark internal lab operations and negotiate supplier contracts using our throughput and cost models.

Closing perspective

The molecular diagnosis of tumors market presents a rare combination of high growth and complex regulatory and commercial dynamics. By 2032 the market could approach roughly USD 19.9 billion, but realizing that upside will require disciplined execution across regulatory compliance, payer engagement, technology differentiation and laboratory operations. PW Consulting’s full report distills the necessary market intelligence, competitive playbooks and executable roadmaps for leaders who must make consequential decisions in 2026.

For the complete dataset, disaggregated segment tables, model access and our advisory engagements, visit PW Consulting’s Molecular Diagnosis Of Tumors Market page or contact our strategy team to arrange a briefing and model walkthrough.

For detailed analysis of this topic, please visit the official page:Molecular Diagnosis Of Tumors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com