Government and Military Satellite Communications Market: Strategic Imperatives for 2026 Decision‑Makers

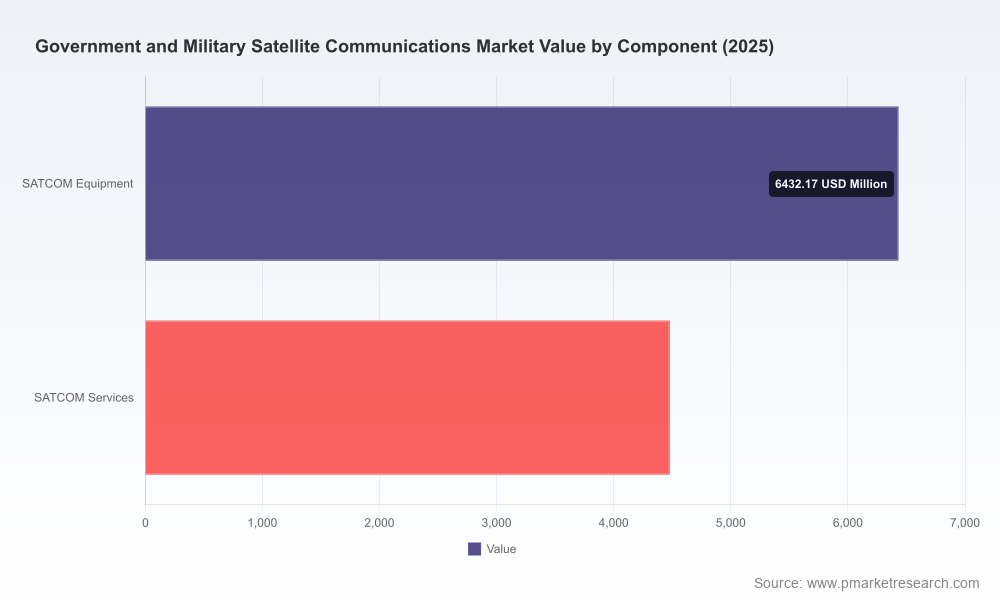

The government and military satellite communications (SATCOM) market is at an inflection point. After a period of steady expansion through the early 2020s, the sector entered 2026 with renewed momentum: our baseline analysis places the global market above USD 10 billion in 2025 and projecting to grow at a compound annual growth rate of approximately 7.0% across the 2026–2032 forecast window. That trajectory drives the market into the mid‑teens billions by the early 2030s, reshaping procurement calendars, industrial strategy, and alliance choices for governments, prime contractors, and new entrants alike.

Government And Military Satellite Communications Market

Why this report matters for 2026 decisions

- Actionable timing: The 2026 procurement cycle will determine multi‑year production lines, constellation commitments, and terminal fielding timelines. Our report translates headline growth rates into month‑by‑month decision points that matter for contracting, capacity reservation, and satellite production slots.

- Trade‑offs quantified: We map trade‑offs between sovereign capability (controlled, resilient GEO/Tactical architectures) and cost/scale advantages of commercial multi‑orbit solutions—and provide the decision framework to prioritize one over the other depending on mission criticality and budget profile.

- Supplier and partner playbook: The intelligence identifies the strategic postures of prime integrators, network operators, terminal suppliers and disruptive LEO providers so procurement teams can short‑list partners aligned to risk tolerance, certification timelines, and export control regimes.

- Risk, resilience and compliance: Practical checklists for export controls, sustainment commitments, and interoperability testing reduce program slippage and cost overruns in an environment of evolving regulations and alliance liberalizations.

Report content — what you get (practical deliverables)

- Executive briefing and 12‑month decision calendar keyed to program and budget cycles.

- Market model (historical 2020–2025 and forward 2026–2032) with scenario toggles for growth, procurement mix, and technology adoption rates.

- Supplier dossiers: strategic intent, capability maps, program exposure, and supplier risk scores for leading systems integrators, network operators, and terminal suppliers.

- Procurement playbooks: sample contract structures, incentive‑aligned milestones, acceptance test regimes, sustainment clauses, and options language tailored to multi‑orbit buys.

- Technology and interoperability assessments: anti‑jam payloads, crosslink architectures, terminal roadmaps, and migration pathways for legacy AEHF/ESS families to hybrid commercial architectures.

- M&A and investment watchlist: early warning indicators for consolidation, divestment candidates, and partnership vectors likely to accelerate capability delivery.

- Field‑deployable templates: RFQ/RFP language, supplier due diligence checklists, and a template interoperability test plan for joint coalition operations.

Competitive landscape — what strategic patterns matter

The competitive field is diverse but not fragmented. The market exhibits measured concentration: a small set of established primes and satellite operators control a meaningful share of capacity, while a fast‑moving tier of technology specialists and LEO entrants are changing the shape of tactical connectivity. Three strategic archetypes emerge:

Government And Military Satellite Communications Market

- Prime integrators and sovereign suppliers — Companies with deep systems‑integration bandwidth, heritage MILSATCOM programs, and program management experience remain central to capability delivery for the most demanding missions. Their strategic advantage lies in accredited, hardened solutions and long sustainment tails. Expect continued competition among legacy primes to secure flagship strategic SATCOM programs and sustainment contracts.

- Network operators and managed‑service providers — Established satellite operators and network service providers are pivoting to hybrid offers that combine managed capacity, ground segment services, and contractually guaranteed performance. Their play is to be the aggregation layer between sovereign buyers and diverse satellite platforms.

- Disruptors and terminal specialists — LEO constellation operators, small GEO providers, and rugged terminal manufacturers are accelerating innovation cycles in latency, mobility, and anti‑jamming technologies. Their ability to demonstrate rapid fielding and interoperable terminals is changing procurement risk calculations.

Key corporate behaviors to watch: increased teaming among primes and network operators on protected, proliferated GEO concepts; vertical partnerships between LEO operators and terminal vendors to present hardened, tactical solutions; and targeted wins by specialist suppliers that translate niche capability into scalable contract vehicles. Our report profiles each major player across capability, program exposure, and strategic intent so decision‑makers can match partners to program archetypes.

Government And Military Satellite Communications Market

Regulatory and programmatic drivers shaping 2026 choices

Public‑policy moves and program callouts are accelerating change. Export‑control adjustments among allied governments are lowering some friction points for collaborative development and supply chains; procurement offices are increasingly using commercial channels to secure capacity while retaining sovereign overlays for critical functions; and major defense programs are crowding the near‑term launch and production pipelines. Collectively, these dynamics shorten decision windows for capacity reservation and force clearer articulation of interoperability and sustainment assumptions in contracts.

Scenario framework — how to stress‑test strategy

We provide three practical scenarios to test procurement and industrial choices:

- Accelerated modernization (Base case) — Continued moderate growth with prioritized investments in protected payloads and hybrid multi‑orbit architectures. Contracting is competitive but predictable.

- Distributed resilience (Upside) — Coalition demand and operational lessons accelerate adoption of proliferated, maneuverable satellites and tactical LEO solutions; early adopters gain field advantage but must manage integration complexity and sustainment risk.

- Constrained budgets (Downside) — Fiscal pressure delays some strategic procurements, increasing demand for managed commercial capacity and business models that transfer program risk to suppliers (e.g., capacity subscription or performance‑based logistics).

For each scenario we quantify implications for capacity demand, supplier revenue exposure, and terminal refresh cycles—allowing organizations to stress‑test procurement options against plausible geopolitical and fiscal futures.

Operational recommendations for 2026

- Adopt a hybrid multi‑orbit procurement posture: combine sovereign GEO capabilities for assured, strategic communications with commercial LEO/GEO services for surge capacity and tactical agility.

- Prioritize terminal interoperability and modularity to accelerate fielding across coalition partners and to lower lifecycle costs.

- Build export‑compliance and sustainment clauses into contracts from day one to avoid mid‑program friction as allied rules and licensing evolve.

- Use staged contracting and options to hedge against launch and production bottlenecks—reserve capacity and satellite manufacturing slots in alignment with mission timelines.

- Insist on clear SLAs and end‑to‑end test regimes when purchasing managed services; push for measurable resilience metrics (anti‑jamming performance, restoration timelines, crosslink availability).

- Design partnership structures that align incentives across primes, network operators, and terminal vendors—consider revenue‑sharing or capacity‑subscription models where appropriate.

- Monitor concentration signals: the market shows meaningful share among top incumbents; use this intelligence to decide whether to foster competition via multiple suppliers or pursue industrial partnerships for sovereign objectives.

How PW Consulting’s analysis supports boardroom and program office decisions

Our market model and supplier dossiers convert macro growth trends into practical procurement actions: they show when to award large‑scale vehicle and payload contracts, how to sequence terminal roll‑outs, and how to structure sustainment obligations to lock in value while maintaining operational flexibility. The result is a decisioning toolkit designed for program offices, defense ministries, and corporate strategy teams that must make binding commitments in 2026 with multi‑decade consequences.

Closing — the intelligence gap we close

The Government and Military Satellite Communications Market report synthesizes quantitative growth trajectories and qualitative competitive dynamics into a single playbook for 2026 execution. We surface which capability combinations deliver operational assurance, outline practical contracting language to preserve maneuverability, and expose the signals that presage supplier consolidation or disruption. The summary above highlights the report’s strategic utility while reserving detailed segmentation models, supplier scorecards, and contract templates for the full publication—deliberately withheld to preserve the actionable core of our work and to ensure subscribers receive the full, validated dataset.

For program offices and executives preparing 2026 budgets and acquisition strategies, the PW Consulting report is the operational intelligence product that turns a 7.0% CAGR and a multi‑billion‑dollar market outlook into executable strategy. Access to the full report provides the granular models, supplier assessments, and procurement templates needed to move from plan to contract without surprise.

To obtain the complete dataset, supplier scorecards, and procurement playbooks referenced here, visit the PW Consulting report page and download the full Government and Military Satellite Communications Market study.

For detailed analysis of this topic, please visit the official page:Government And Military Satellite Communications Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com