Anti-Aging Mesotherapy in Dubai: Reverse Years with Micro-Injections

Health |

2026-03-26 10:02:11

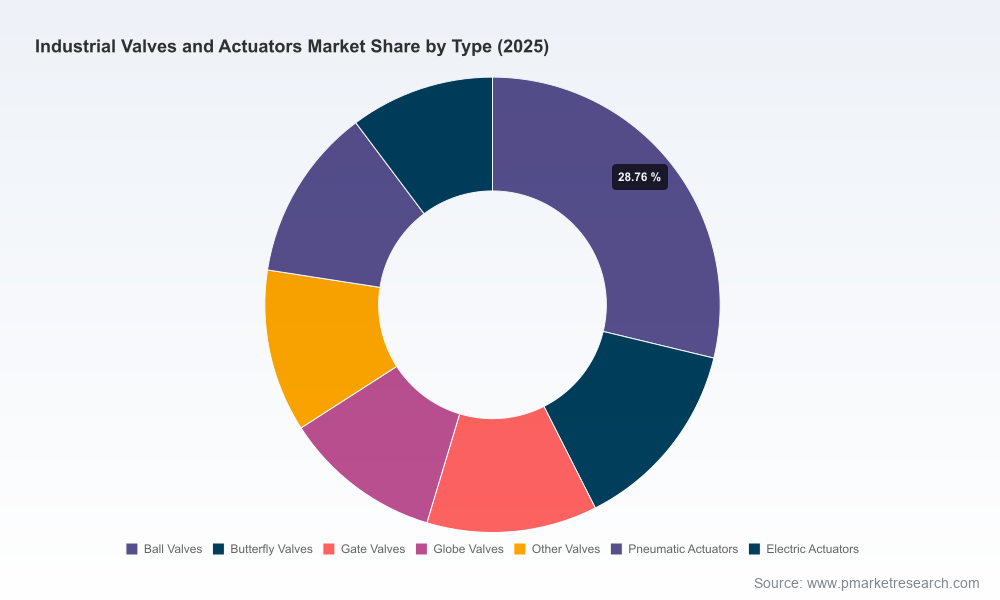

As PW Consulting’s latest market research report on Industrial Valves and Actuators goes live, senior executives, procurement leads and strategy teams face a pivotal planning window. Our analysis shows the industry has recovered and structurally expanded in the first half of the decade — rising from an estimated USD 118.45 billion in 2020 to about USD 159.34 billion in 2025 — and is projected to continue its trajectory through 2032. With a compound annual growth rate (CAGR) of 5.45% over the 2026–2032 forecast period, the sector presents both durable opportunity and intensifying strategic complexity entering 2026.

Industrial Valves And Actuators Market

Evidence‑based foresight: We translate macro momentum (market scale and growth trajectory) into decision priorities—capital allocation, supply‑chain design, product roadmaps and inorganic growth targets.

Industrial Valves And Actuators Market

Playbook orientation: Beyond market sizing, the report contains operational tools—price pass‑through models, capex vs. opex scenarios for electrification projects, and supplier health dashboards—that executives can apply directly in 2026 budgeting cycles.

Industrial Valves And Actuators Market

Risk‑to‑return calibration: We quantify how raw‑material shocks, trade policy and technology adoption alter margin profiles across common business models in valves and actuation.

The industry’s expansion through 2025 reflects resilient demand from energy transition projects, infrastructure renewals and the modernization of process facilities. Our long‑range view projects the market approaching the low‑to‑mid hundreds of billions by the end of the forecast horizon, underpinned by mid‑single‑digit CAGR. This growth masks material heterogeneity: while some end markets and product subsegments are moving toward consolidation and premiumization, others remain fragmented and price‑sensitive—creating differentiated strategic openings for agile market participants.

Electrification and digital integration: Adoption of electric actuators and smart valve systems is accelerating. Executives must evaluate retrofit vs. greenfield strategies, quantifying lifecycle energy savings, uptime improvements from digital monitoring, and integration costs with control systems.

Raw material and trade policy volatility: Steel and alloy cost dynamics are a near‑term margin lever. Steel prices moved above USD 1,000 per ton in 2026 amid tariff pressure and supply constraints, while trade measures implemented in 2025 continue to raise import costs. Suppliers and OEMs that establish index‑linked purchasing, strategic hedges, or localized production footprints will differentiate on margin stability.

Concentration and competitive positioning: The market remains moderately fragmented—CR3 and CR5 metrics indicate that leading suppliers control a meaningful but not dominant share of global revenue. That structure supports both targeted M&A to build scale in key applications and organic strategies focused on technical differentiation.

Regulatory and safety drivers: Nuclear, water and critical infrastructure projects are influencing demand for specialized actuation technologies (for example, gas‑charged hydraulic systems and high‑integrity electric actuators). Anticipating regulation‑driven specs can unlock long‑tenured service contracts.

The competitive set combines large diversified industrial groups, specialist actuator manufacturers and systems integrators. Established engineering leaders supply end‑to‑end control solutions and have deep installed bases; specialist actuator firms compete on electrification, service networks and intelligent actuation. Recent corporate actions underscore this dynamic:

Flowserve’s acquisition of Trillium Flow Technologies’ Valves Division in early 2026 reinforces scale in critical infrastructure and nuclear‑grade equipment—an M&A play to accelerate market share and capability.

Rotork’s 2025 results and commentary emphasize procurement wins in wastewater projects and a strategic push toward electrification and net‑zero support: a clear commercialization pathway for smart actuation in municipal markets.

Emerson’s recent outlook highlights automation and final control solutions as a core growth pillar—reminding incumbents that integrated automation offerings remain a durable competitive advantage.

Company profiles in our report provide granular, transaction‑level intelligence on capabilities, service footprint, technology roadmaps and channel strategies for major players—information designed to feed target selection, benchmarking and partnership planning. (For the full dataset and comparative matrices, see the subscription report.)

Procurement leaders must act across three time horizons in 2026:

Immediate (0–12 months): Stabilize cost pass‑through frameworks and secure critical castings and machined components under index‑linked or hedged contracts to reduce spot exposure.

Medium (12–36 months): Reassess global sourcing footprints in light of tariffs and logistics risk; prioritize suppliers with localized repair networks and strong digital service platforms.

Strategic (36+ months): Invest in supplier co‑innovation for electrified actuation platforms and digital valve analytics to capture aftermarket service economics.

Our scenario analyses quantify the impact of two high‑probability shocks on 2026 P&L and balance sheet outcomes: a persistent tariff regime (as seen since 2025) which raises landed costs, and a raw‑material price spike similar to the 2026 steel uptick. Firms that modeled these scenarios and implemented mitigating actions—vertical integration of critical supply, pass‑through clauses in contracts, or targeted product price increases with customer value justification—preserved margins and shortened cash conversion cycles. The report provides templates for these stress tests and suggested covenant language for supplier agreements.

Actionable market playbooks: segment entry checklists, three‑year GTM tactics for electrification, and retrofit decision matrices for OEMs and end users.

Procurement toolkits: index‑linked contract templates, cost‑uplift modeling spreadsheets, and supplier risk scoring methodologies.

M&A & partnership pipeline: criteria‑based shortlists, synergistic capability maps, and valuation multiples guidance anchored to comparable transactions and current market dynamics.

Technology adoption roadmap: TCO comparisons for actuator types, deployment sequencing for digital valve monitoring, and integration playbooks for plant operators.

Service and aftermarket optimization guide: strategies to convert installed base into recurring revenue via predictive maintenance, remote diagnostics and spare‑parts rationalization.

Commodity and tariff volatility: Continued upward pressure on steel and alloy costs, and elevated tariff rates, will require dynamic procurement policies.

Competitive repricing: Acquisition activity and scale plays may compress prices in certain OEM segments—execute defensible premium strategies on technical differentiation.

Technology integration lag: Digitalization yields operational benefits only where integration with plant control systems and service models is coherent—insufficient systems integration risks suboptimal ROI.

Prioritize electrification pilots in high‑value sites where lifecycle cost and downtime benefits are measurable; use pilot outcomes to build standardized retrofit bundles.

Rebalance supplier networks toward partners offering technical services and spare‑parts availability—service revenue can be a margin hedge during raw‑material price swings.

Prepare an M&A watchlist: identify bolt‑on targets that accelerate electrification, expand service footprint, or add application‑specific credentials in regulated markets.

Institutionalize material cost triggers: adopt index‑based contracting and scenario budgets tied to metal price bands and transport cost indices.

Embed regulatory surveillance: ensure product roadmaps account for specification shifts in nuclear, water and critical infrastructure projects.

This report was developed to move beyond descriptive analytics. It equips decision makers with the quantitative context (market scale and growth path), qualitative nuance (competitor strategies and customer buying behavior), and operational artifacts (contracts, scorecards, templates) necessary for execution. For teams building 2026 budgets, the report’s scenario engines and procurement playbooks are ready to be customized to client data.

Executives seeking to convert market insight into action should begin with three pragmatic steps: 1) run the PW Consulting stress tests on your supplier network using our model, 2) scope a 90‑day electrification pilot with cost‑benefit criteria drawn from our adoption roadmap, and 3) review the report’s M&A shortlists to identify targets that close capability gaps in your priority geographies. The full report contains the supporting datasets, comparative company matrices and downloadable playbooks to operationalize each recommendation.

For access to the complete Industrial Valves and Actuators Market report, including full segmentation, proprietary datasets and the detailed competitive matrices, visit the PW Consulting research portal or contact our advisory team for a briefing.

For detailed analysis of this topic, please visit the official page:Industrial Valves And Actuators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com