Automotive Multi‑Domain Controller Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

PW Consulting’s latest market study on Automotive Multi‑Domain Controllers (MDCs) delivers a concise, actionable playbook for executives preparing decisions in 2026. Drawing on a 2020–2025 historical foundation and a 2026–2032 forecast window, the report quantifies the structural growth drivers, exposes supplier and technology inflection points, and prescribes prioritized actions for OEMs, Tier‑1s, semiconductor vendors, and investors. The market is entering a high‑velocity phase: using 2025 as the base year, our modeling projects a compound annual growth rate of 14.5% across the forecast period, more than doubling market scale by the end of 2032.

Automotive Multi Domain Controller Market

Executive summary: Why 2026 is a strategic hinge year

- Momentum. Centralized and multi‑domain architectures are transitioning from pilot programs to scaled production — enabling consolidation of IVI, ADAS, cockpit and gateway functions under single computing architectures.

- Commercial window. Cost declines in advanced process nodes and software reuse models are beginning to align with regulatory and safety timelines, creating a narrow window in 2026–2027 for positioning differentiated platforms.

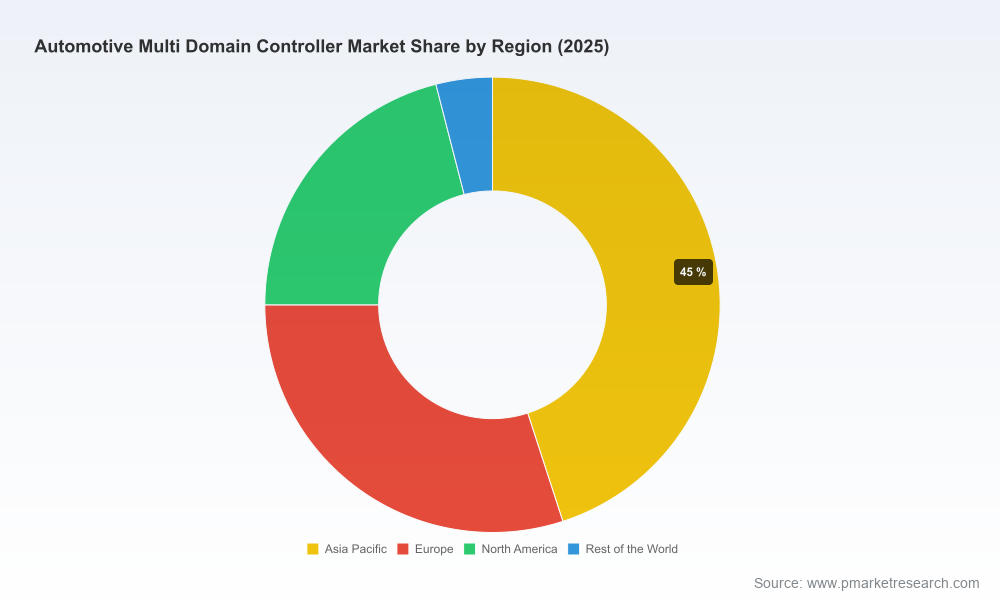

- Risk concentration. Market share is moderately concentrated (CR3 ~45.2%; CR5 ~62.4%), indicating that a limited set of incumbents and system‑level integrators exert disproportionate influence over standards, supplier selection and OEM roadmaps.

Market trajectory and what the headline numbers mean for strategy

Using 2025 as the base year, our topline forecast anticipates robust expansion through 2032 — underpinned by software‑defined vehicle adoption, regulatory safety mandates, and rapidly increasing compute requirements for ADAS and cockpit intelligence. The projected 14.5% CAGR reflects not only unit adoption of MDC architectures but also escalating content per vehicle as OEMs consolidate electronic control and advanced user experiences into centralized platforms.

Automotive Multi Domain Controller Market

For decision‑makers, the headline implication is twofold: (1) revenue pools will grow materially, but capture will be uneven — favoring suppliers that combine silicon, system integration, and lifecycle software capabilities; and (2) first‑mover commitments in 2026 to validated architectures and supply agreements will compound positional advantage through the late 2020s.

Automotive Multi Domain Controller Market

Competitive landscape: who leads, who follows, and what it means

- System integrators and Tier‑1s: Established suppliers with cross‑domain integration capabilities can translate hardware wins into recurring service and software revenue. Companies that demonstrate validated high‑performance computing deployments and vehicle‑level integration are best positioned to capture platform premiums.

- Semiconductor houses: Advanced process node SoCs and domain‑focused platforms are determining architecture choices. Vendors supplying purpose‑built automotive SoCs and real‑time platform stacks will influence OEM selection criteria — particularly where deterministic latency and ASIL compliance are required.

- Software and cloud ecosystem: Suppliers that can provide OTA update frameworks, cybersecurity solutions, and validated middleware will unlock recurring value beyond the one‑time hardware sale.

Representative profiles examined in the report include cross‑domain integrators and semiconductors that are actively shaping the MDC landscape. Our competitive assessment evaluates engineering roadmaps, go‑to‑market models, partnership networks, and recent milestones — reflecting how players are translating R&D into production‑level value.

Recent industry moves that will define 2026 battles

- Renesas’s launch of a 3nm multi‑domain SoC in late 2025 signals an acceleration in automotive process node adoption, enabling concurrent ADAS, IVI and gateway workloads on single silicon.

- Continental’s field implementations of cross‑domain high‑performance computers demonstrate system integrator capability to stitch cockpit and vehicle functions together at scale.

- Head‑line product showcases from cockpit specialists point to increasing centralization of displays and user experiences — pressuring legacy ECU counts and stimulating consolidation deals.

- Strategic wins involving Qualcomm‑based solutions illustrate the role of consumer‑grade compute adapted for automotive safety and lifecycle requirements.

Technology and supply‑chain dynamics: immediate operational risks

Two operational realities will demand explicit mitigation plans in 2026:

- Component concentration and process node timing. High‑performance MDCs increasingly rely on advanced SoCs; managing access to node‑leading silicon and ensuring automotive‑grade qualification are critical to program schedules.

- Memory and commodity volatility. Early‑2026 DRAM tightness pushed legacy memory prices sharply higher — our industry intelligence records near‑term price shocks on legacy DDR/LPDDR parts. Program teams must assume episodic memory cost inflation when modeling BOM and negotiating supplier terms.

Regulatory and safety environment: compliance as a strategic enabler

Functional safety and cybersecurity regimes have moved from checkbox compliance to commercial differentiators. ISO 26262’s ASIL framework remains foundational for hardware and software development; simultaneously, UNECE R155/R156 requirements for cybersecurity management systems and software update governance are shaping supplier selection and architecture decisions.

Moreover, evolving safety mandates — including advanced driver assistance performance expectations — are raising the minimum compute and functional redundancy requirements for MDC platforms. OEMs that bake ASIL‑oriented design and robust CSMS practices into early RFPs will reduce integration friction and time to market.

What’s inside the PW Consulting report (practical highlights)

- Topline market model with annual market size projections through 2032 and scenario analyses that stress‑test volume, content per vehicle, and price erosion assumptions.

- Commercial playbooks for OEMs and Tier‑1s: procurement strategies, contract structures to hedge memory and silicon price risk, and bundling approaches for software and services.

- Technology roadmaps mapping compute, functional safety, and software stacks to likely architecture outcomes through 2030 — enabling platform vs. modular investment tradeoffs.

- Supplier diligence frameworks and supplier health diagnostics that identify exposure across process nodes, IP dependencies, and manufacturing footprints.

- Deal and partnership matrices including real‑world case studies that illustrate successful pivot strategies from legacy ECU positions to MDC‑centric offers.

Actionable recommendations for 2026 decision cycles

Our guidance is prioritised by time horizon and enterprise function to accelerate execution without undermining long‑term optionality.

- Short term (0–12 months)

- Lock in multi‑year memory and silicon supply agreements with price‑adjustment clauses tied to clear indexation to protect near‑term BOM. Assume episodic DRAM tightness when stress testing P&L.

- Embed ISO 26262 and UNECE CSMS requirements into RFPs and acceptance criteria to avoid late‑stage redesigns and certification bottlenecks.

- Establish cross‑functional MDC steering committees (product, safety, procurement, legal) to unify decision criteria and accelerate approval cycles.

- Medium term (12–36 months)

- Pursue targeted partnerships that combine silicon access, system integration capability, and software lifecycle management to capture recurring revenue streams.

- Invest in modular software architectures and continuous update frameworks to monetize post‑sale features while managing cybersecurity obligations.

- Prioritise pilot‑to‑scale transitions on one or two platform families to avoid proliferation of incompatible MDC architectures across vehicle portfolios.

How to use this market intelligence

C‑suite leaders will find the report useful for aligning corporate strategy, M&A origination, and portfolio planning. Product heads can use the technical roadmaps to prioritize feature sets by safety class and compute requirement. Procurement and supply chain teams will benefit from our negotiated‑terms templates and cost sensitivity analyses tailored for MDC program economics. Investors and private equity teams will find the combination of forecasted growth, concentration ratios, and supplier‑level risk diagnostics helpful for valuation and due diligence.

Closing: the strategic lift you get — and where to go next

PW Consulting’s Automotive Multi‑Domain Controller Market study is designed as a decision accelerator for 2026. It provides a macro view (with a clear CAGR and topline trajectory) while delivering operational playbooks and supplier intelligence that reveal where value crystallizes and where execution risk concentrates. The report intentionally omits publishing core regional and application sub‑tables in this brief — those granular splits, component‑level cost curves, and scenario spreadsheets are accessible through the full report on our website.

For procurement teams, product leaders, or investors ready to convert market momentum into commercial advantage, the full dataset and downloadable annexes contain the granular segmentation and model‑level guidance necessary to finalize 2026 program commitments.

For detailed analysis of this topic, please visit the official page:Automotive Multi Domain Controller Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com