Why Is Artificial Intelligence Platform Market Becoming the Foundation of Enterprise AI Adoption?

Networking |

2026-06-02 05:48:55

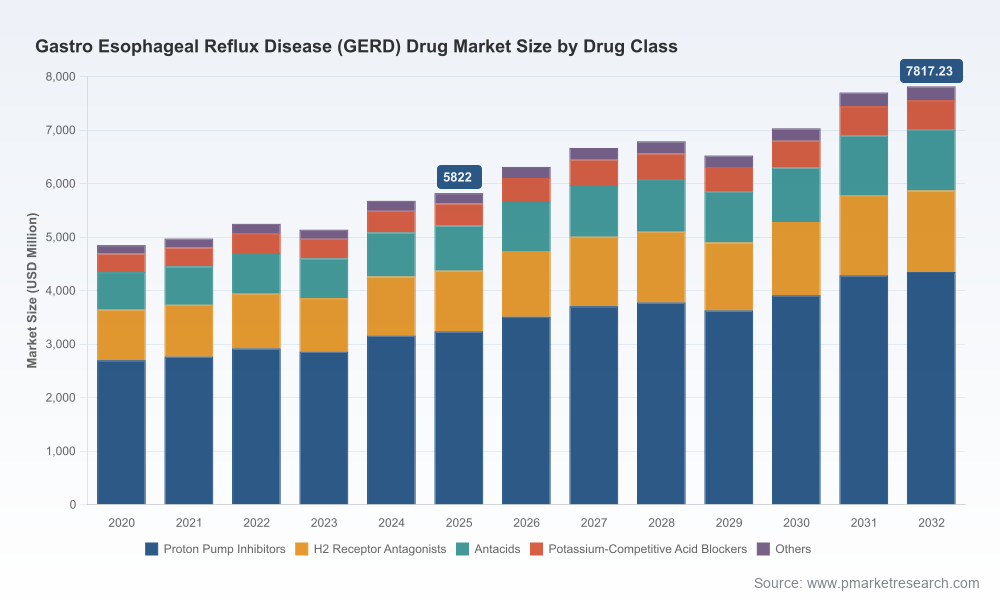

PW Consulting’s latest market study on the Gastroesophageal Reflux Disease (GERD) drug landscape delivers a focused, decision-ready briefing for life sciences executives preparing strategies for 2026 and beyond. The global GERD drug market, having recovered from episodic volatility over the past half-decade, is projected to continue steady expansion — our base-year analysis (2025) places total market revenue at USD 5,822.0 Million, with a compound annual growth rate (CAGR) of 4.3% across the 2026–2032 forecast horizon. These macroscopic dynamics underpin practical choices in portfolio prioritization, commercial investments, and risk mitigation that we outline below.

Gastro Esophageal Reflux Disease Gerd Drug Market

Actionable foresight at the right granularity: We combine top-down market sizing with scenario-based forecasts and sensitivity analyses to translate macro growth into concrete revenue ranges for product types, channels, and strategic initiatives — enabling CFOs and commercial leads to set 2026 budgets with confidence.

Gastro Esophageal Reflux Disease Gerd Drug Market

Timing-sensitive recommendations: With new drug classes emerging and generics dominating many therapy segments, 2026 is a hinge year for commercialization choices — first-mover investments in differentiated assets or disciplined defense against margin erosion are decisions that must be informed by up-to-date adoption curves and payer behavior models provided in the report.

Gastro Esophageal Reflux Disease Gerd Drug Market

Concentration and competitive pressure: Our market concentration analysis shows that the top three firms account for a meaningful share of market revenue (CR3: 42.5%) while the top five push cumulative concentration to 58.8% (CR5). This dual reality — significant incumbent power but meaningful room for mid-tier challengers — shapes realistic M&A and partnership strategies going into 2026.

Proprietary market model calibrated to 2020–2025 historicals and stress-tested across multiple 2026–2032 scenarios, including baseline, accelerated adoption of new classes, and heightened generic penetration.

Commercial playbooks for each major drug class: tactical messaging, channel mix optimization (retail, hospital, digital), and payer negotiation levers designed to protect margin where generic competition is strongest and to maximize uptake where clinical differentiation exists.

Regulatory and reimbursement heat maps that prioritize geographies and segments by ease of market access, reimbursement headroom, and timeline to potential coverage decisions — enabling precise resource allocation for 2026 market-entry and lifecycle projects.

Supply-chain risk matrix with supplier criticality scoring, API vulnerability indices, and contingency triggers. This includes mitigation pathways for API disruptions — a salient issue after recent pantoprazole sourcing challenges in Europe — and sourcing playbooks for new entrants.

Competitive landscaping with tactical dossiers on leading players and credible challengers, including value-proposition frameworks for branded products, generics, and new mechanisms of action such as potassium-competitive acid blockers (P-CABs).

Commercial impact simulations for emerging approvals and generic launches (illustrative scenarios only). The report intentionally refrains from publishing confidential sub-regional or application-level figures in this summary; access to the full dataset (including segmented revenue runs, channel split matrices, and price erosion curves) is available via the source portal.

The GERD treatment landscape in 2026 will be shaped by a mix of established multinationals, large generic manufacturers, and targeted innovators. Incumbent legacy brands remain influential in institutional settings, while generics dominate volume-driven channels. Our qualitative and quantitative assessment of key players reveals several strategic vectors:

AstraZeneca (Nexium/esomeprazole): Brand equity and clinical familiarity are strengths in certain specialty and hospital channels. However, historical patent expirations have already shifted significant volume to generics, requiring brand owners to emphasize differentiation through patient support, outcome data, and specialty formulations.

Pfizer (Protonix/pantoprazole) and Takeda (Dexilant/dexlansoprazole): Established hospital and specialty penetration provides a platform for lifecycle management and label expansion efforts; their success will hinge on maintaining supply continuity and demonstrating incremental clinical or adherence benefits versus lower-cost alternatives.

Viatris, Teva, Dr. Reddy's, Sun Pharma et al. (Generics): Pricing power in retail and payer formularies creates durable volume playbooks. Generics players should prioritize scale efficiencies, supplier diversification, and contractual wins with large retail and integrated delivery networks to defend margin in 2026.

Sanofi and Johnson & Johnson (H2 blockers): OTC and symptomatic relief channels remain relevant; positioning around safety, convenience, and co-marketing with consumer health channels will be a practical lever for growth.

Phathom Pharmaceuticals (Voquezna/vonoprazan): The introduction and regulatory approvals of P-CABs represent a structural opportunity to reset treatment algorithms, particularly for patients seeking faster onset of symptom control. P-CAB commercialization strategies — including hybrid specialty/primary care tactics and payer value dossiers emphasizing speed-to-relief — are a key theme in our 2026 playbooks.

New approvals and label expansions (e.g., P-CABs) that change prescriber switching behavior — the report models uplift scenarios tied to recent approvals and anticipated formulary decisions.

Regulatory withdrawals and safety events (historically exemplified by ranitidine’s market exit) that can reassign volume rapidly across drug classes; contingency planning in procurement and channel management is essential.

Ongoing generic penetration trends: more than 90% of PPI prescription volumes have shifted to generics historically; our study quantifies likely further erosion under different patent and competitive scenarios and prescribes defensive measures for branded stakeholders.

Supply-side constraints: reported API shortages (notably pantoprazole in recent European supply chains) require near-term supplier diversification and inventory strategy tweaks ahead of 2026 procurement cycles to avoid missed revenue.

Based on our integrated market modeling and competitive diagnostics, we recommend a prioritized set of actions organized by corporate objective:

Invest in differentiation — real-world evidence on symptom relief speed, adherence-boosting formulations, and patient support programs can sustain premium pricing even in mature classes.

Lock strategic supply agreements and regional buffer stocks to defend institutional contracts against generic substitution and API disruptions.

Evaluate targeted acquisitions or licensing of P-CABs or other differentiated assets to offset long-term brand deflation.

Prioritize contractual wins with major retail and hospital networks, and optimize cost-to-serve via vertical integration of key APIs.

Use segmentation analytics to defend profitable niches where brand loyalty or formulary placement creates above-average margins.

Focus on narrow indications, robust payer dossiers, and early formulary negotiations to accelerate adoption of P-CABs or other novel mechanisms within 24 months of approval.

Forge partnerships with established commercial players to leverage distribution breadth while preserving upside through milestone-based licensing.

Embed supply-chain stress testing into 2026 planning cycles, with defined triggers and alternate supplier lists for critical APIs.

Operationalize a reimbursement playbook for faster-onset therapies that quantifies economic value to payers and providers.

Accelerate digital channels in patient-facing segments (telehealth, online pharmacies) where convenience and adherence programs can shift share.

The PW Consulting GERD drug market study is structured as an operational toolkit: detailed market models (with downloadable segmented datasets), competitor dossiers, scenario planning modules, and executable commercial playbooks. For executives preparing 2026 budgets, the report reduces uncertainty by converting the market’s macro trajectory — from USD 5,822.0 Million in 2025 toward a modeled endpoint in our forecast horizon — into practical tactics and prioritized investment pathways.

Note: This executive release intentionally omits granular regional and application-level splits and other confidential segment matrices that inform precise tactical decisions. Those data tables, sensitivity runs, and playbook templates are available in the full report package and via our secure portal for clients and authorized stakeholders.

Request a tailored briefing: schedule a 60-minute strategy session with PW Consulting’s GERD team to review the model outputs most relevant to your portfolio and to stress-test 2026 scenarios against your assumptions.

Obtain the full dataset: access segmented forecasts, channel-specific price erosion curves, and supplier risk dashboards to finalize procurement and commercialization plans for 2026.

Engage our implementation team: convert the report’s playbooks into Q1–Q4 2026 tactical roadmaps with KPIs, resource requirements, and quick-win timelines.

PW Consulting’s GERD drug market study equips decision-makers with the foresight to act decisively in 2026: to defend margin where needed, to invest in differentiation where clinically and commercially viable, and to reduce operational risk in a landscape that balances entrenched incumbency with rapid therapeutic innovation.

For detailed analysis of this topic, please visit the official page:Gastro Esophageal Reflux Disease Gerd Drug Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com