Biodegradable Mulch Film Manufacturers and Technology

Other |

2026-03-20 11:48:05

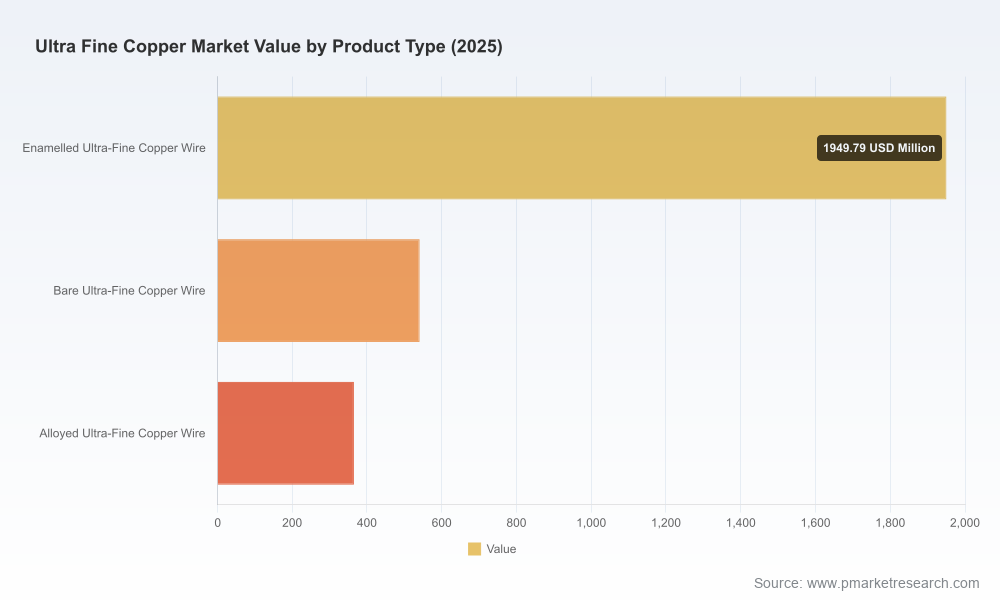

PW Consulting’s latest Ultra Fine Copper Market report (base year 2025, historical window 2020–2025, forecast 2026–2032) delivers the actionable intelligence corporate leaders need to make high-consequence decisions in 2026. The market expanded materially through the pandemic recovery window and reached approximately USD 2.86 billion in 2025, driven by demand across electronics, EV platforms and advanced manufacturing. Our model projects a steady compound annual growth rate (CAGR) of 5.48% through 2032, bringing the market to just over USD 4.1 billion by the end of the forecast horizon. Concurrently, the market structure shows a moderate level of concentration (CR3 ~38.5%, CR5 ~52.1%), leaving room for both consolidation and niche incumbency plays.

Ultra Fine Copper Market

Timing and scale: With mid-single-digit CAGR and a clear trajectory to 2032, firms must balance near-term margin pressure with medium-term capacity and capability investments. 2026 is a pivotal year to decide whether to accelerate localization, expand product portfolios, or pursue bolt-on M&A.

Ultra Fine Copper Market

Supply-chain exposure: Price volatility in primary copper and concentrated powder-production capability create idiosyncratic supply risk—requiring procurement redesigns, hedging, and supplier development programs.

Ultra Fine Copper Market

Regulatory and handling complexity: Nano- and ultra-fine copper fall into enhanced regulatory regimes in key jurisdictions, influencing product design, labeling, and customer acceptance. Compliance strategies will become a commercial differentiator.

Proprietary demand model: A scenario-based volume and revenue model covering 2020–2032, with buy-side adjustable levers for penetration, substitution and technology adoption. The public preview includes top-line trajectories; subscribers receive cell-level forecasts by product, application and region.

Supply-map and cost stack: A granular supply-map from raw-cathode sourcing through atomization, classification and finishing, paired with an input-driven cost build-up to help you stress-test margins under different copper-price regimes.

Regulatory playbook: Practical checklists and compliance timelines for REACH, GHS and other jurisdictional requirements affecting nano-classified copper powders and wires—designed for product teams and regulatory affairs.

Go-to-market and commercialization roadmaps: Channel strategies and OEM engagement templates for segments such as advanced electronics, automotive electrification and additive manufacturing.

M&A and partnership scorecard: Tactical frameworks to evaluate targets, including technology fit, capacity synergies and regulatory liabilities—plus a shortlist of strategic archetypes for 2026 value capture.

Technology and IP landscape: An annotated review of production processes (gas- and water-atomization, atomization variants, surface treatments), feedstock purity regimes and emerging additive-manufacturing use cases.

Three dynamics will disproportionately shape the next 12–24 months:

Raw-material cost volatility: Primary copper prices experienced pronounced swings in 2024 that propagated through powder and wire production costs. While input charges softened in some refining stages, episodic peaks remain a key margin risk. Procurement teams should embed scenario-based hedges and multi-source contracts into 2026 budgets.

Trade and policy friction: Ongoing tariff regimes in major markets are driving re-shoring and near-shore manufacturing economics. Firms exposed to cross-border supply of ultra-fine powders should re-evaluate landed-cost assumptions and consider tariff-engineered supplier diversification.

Regulatory tightening on nanoforms: Authorities in several regions now require specific registration and data for nano-class materials, and classification as nanomaterials triggers additional testing and disclosure. Compliance cost and time-to-market effects can be material for product launches and OEM qualification cycles.

The competitive set spans global specialty powder producers, diversified mining/metals groups, and emerging high-sphericity/AM-focused firms. Key incumbents we profile in the report include:

Fukuda Metal Foil & Powder Co., Ltd. (Osaka, Japan): Established in superfine copper powder for conductive pastes and sintered components; deep process know-how in atomization and particle-size control.

Mitsui Mining & Smelting Co., Ltd. (Tokyo, Japan): Strong on high-purity powders for electronics and additive manufacturing; vertically integrated capabilities are a defensive moat for high-spec applications.

Sumitomo Metal Mining Co., Ltd. (Tokyo, Japan): Supplier of sub-10-micron atomized powders for conductive adhesives and 3D printing; balance-sheet strength supports capacity investments and long-term contracts.

GGP Metalpowder AG (Schlatt, Switzerland): Gas-atomized powders focused on powder metallurgy and thermal spraying—offers premium particle distribution control and European market access.

Shanghai CNPC Powder Material Co., Ltd. (Shanghai, China): High-volume producer of nano and ultra-fine powders for diverse industrial uses; cost-competitive position but faces trade-policy risk in some export markets.

Shenzhen Nonfemet Technology Co., Ltd. (Shenzhen, China): Specialist in high-sphericity powders for selective laser melting and conductive inks—representative of the new-tech cohort aligned to AM and printed electronics.

American Elements (Los Angeles, USA): Flexible manufacturer of custom-grade powders across a broad purity and size spectrum; attractive for research-driven OEMs and prototyping programs.

Strategic takeaway: incumbents blend process IP, feedstock access and regulatory capability. New entrants must either pursue differentiated technical performance (particle morphology, oxidation control), secure captive feedstock, or occupy local/regulatory-advantaged niches to win commercial contracts.

Our report outlines three prioritized scenarios with concrete action lists for procurement, product and corporate strategy teams:

“Cost-Pressure Defense” — Prioritize flexible sourcing, multi-year supplier agreements with price collars, and working-capital optimization. Tactical actions include re-negotiating take-or-pay terms, pilot local blending plants and lock-in of key logistics partners to mitigate tariff exposure.

“Technology Premium” — Invest in R&D to reduce surface oxidation, improve sphericity and expand powder chemistries for additive manufacturing. Build co-development agreements with AM OEMs and secure early-adopter commitments to de-risk capex.

“Regulatory-First” — Accelerate REACH/GHS readiness, build testing partnerships and create a labeled-compliance product line for regulated markets. Use compliance as a commercial differentiator in tender processes and OEM qualification.

Segment-targeted partnerships: Pair advanced-material producers with OEMs in electronics and EV powertrains for co-developed formulations; structure revenue-share pilots with clear go/no-go gauges.

Localized manufacturing pilots: Use tariff and regulatory vectors to justify low-capex local finishing hubs in strategic markets rather than large greenfield powder plants.

Pricing architecture redesign: Move away from pure spot pass-through models; introduce alloy- and process-premium pricing bands, and negotiate index-based clauses with suppliers to stabilize margins.

M&A prioritization: Target bolt-on players that deliver particle-shape differentiation, regulatory dossiers, or embedded OEM relationships rather than volume-only plays.

Regulatory regimes have reached a level of specificity that directly impacts product design and go-to-market timing. Examples include registration requirements for nano-copper under regional chemical agencies, and global transport/handling obligations under contemporary GHS editions. Practical implications include additional testing timelines, labeling changes and potential constraints on industrial applications without robust safety data packages. Our report contains a compliance checklist and recommended timelines to incorporate into 2026 product roadmaps.

Procurement and supply-chain leaders should embed our cost-stack and scenario outputs into budget cycles and supplier RFPs.

Product and R&D teams should use the technology landscape and co-development templates to prioritize programs with the fastest path to commercial qualification.

Corporate development teams should apply the M&A scorecard to prioritize targets and eschew high-capex volume plays in favor of IP, customer lists and regulatory footholds.

Consistent with our “preview” approach, this press release demonstrates the report’s strategic depth while withholding select granular tables and company-level revenue splits that are part of the full deliverable. Specific regional/application/product-dollar breakdowns, detailed supplier cost-by-node, and company-level revenue estimates (where applicable) are reserved for the report to preserve commercial value and ensure subscription-grade confidentiality.

For strategy teams preparing 2026 capital and commercial plans, the PW Consulting Ultra Fine Copper Market report is designed to be an integrated decision support tool: a demand and supply model, a compliance playbook, a technology and competitor roadmap, and an M&A prioritization framework in one. To request the full report, model access or to schedule a tailored executive briefing, please contact PW Consulting or visit our report page for subscription options.

For detailed analysis of this topic, please visit the official page:Ultra Fine Copper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com