Understanding the Value Behind Precious Metals

Other |

2026-06-25 07:55:13

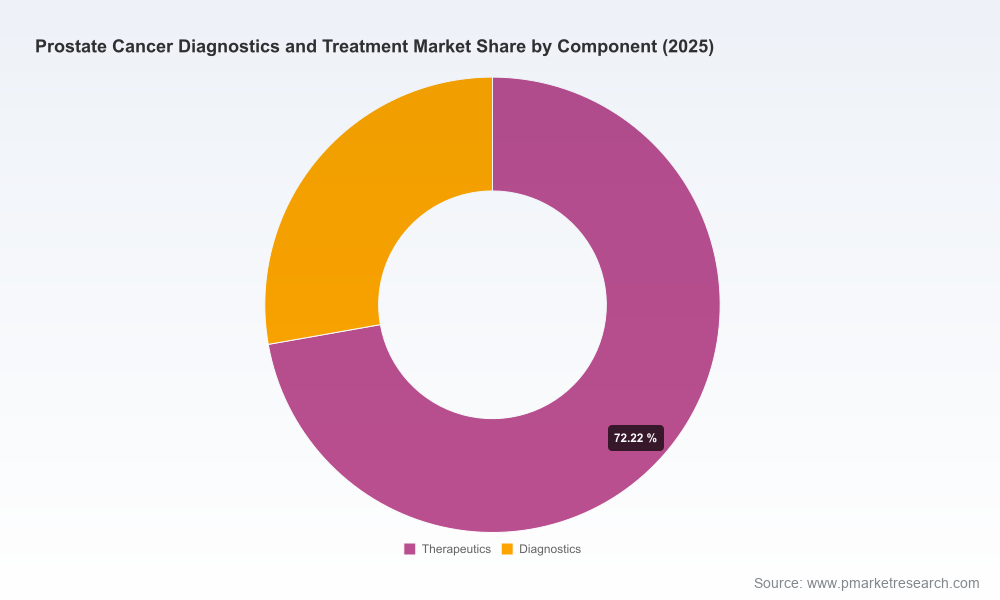

PW Consulting’s latest market research report on Prostate Cancer Diagnostics and Treatment presents a focused, practitioner-oriented view of a market in structural transition. The global market reached approximately USD 60,970 Million in 2025 (base year) and, under our central scenario, is projected to expand at a compound annual growth rate (CAGR) of 9.85% across the 2026–2032 forecast window — reaching roughly USD 117,684 Million by 2032. This briefing highlights the strategic implications of those macro dynamics for executive teams preparing plans, capital allocations, and pipeline priorities in 2026. Consider this a high-fidelity trailer: we describe the playbook and the high-impact inflection points while reserving the full segment-level tables, regional matrices and financial models for the report itself.

Prostate Cancer Diagnostics And Treatment Market

Time-sensitive portfolio decisions: Accelerated regulatory approvals and indication expansions are shifting market opportunity from late-line to earlier-line settings. Companies need forward-looking probability-weighted forecasts and clinical-catalyst calendars to avoid misallocated R&D and commercialization spend.

Prostate Cancer Diagnostics And Treatment Market

Diagnostics-commercialization alignment: The increasing requirement for companion diagnostics to select patients for precision therapies makes coordinated diagnostic-therapeutic go-to-market playbooks essential for capture of premium pricing tiers.

Prostate Cancer Diagnostics And Treatment Market

M&A and partnership prioritization: Patent expirations and new modality growth (notably radioligand therapies and targeted agents) make 2026 an actionable window for bolt-on acquisitions, licensing deals, and manufacturing partnerships that can materially alter market position by 2028–2030.

Reimbursement and access preparation: Regulatory approvals alone no longer guarantee adoption. Payer evidence strategies and PSMA-PET imaging validation are increasingly determinative of commercial uptake for advanced diagnostics and radiopharmaceuticals.

Regulatory momentum and indication creep: Recent approvals in 2025–2026 have expanded the addressable population and lowered the bar for moving effective therapies into earlier disease stages. These shifts, combined with ongoing Phase 3 readouts, create multiple near-term demand inflection points.

Precision medicine requirements: The FDA’s emphasis on companion diagnostics for therapies targeting BRCA mutations and PSMA-positive disease elevates diagnostic companies from service providers to strategic gatekeepers for therapy access.

Radioligand adoption: The expanded regulatory label for PSMA-directed radioligand therapy and growing reimbursement precedents mean radiopharmaceuticals will capture disproportionate attention from specialty oncology portfolios and nuclear medicine infrastructure providers.

IP cliffs and pricing pressure: Key androgen receptor inhibitors face patent expirations in major markets in the 2026–2027 window. That creates parallel incentives to defend margin via novel combination therapies, lifecycle extensions, and diversification into modalities less susceptible to generic erosion.

Imaging and diagnostics convergence: Uptake of advanced PET/MRI platforms and next-generation molecular assays is converging into new diagnostic pathways that change referral patterns, stage migration, and downstream therapeutic mix.

Mid‑2025–2026 approvals and data releases materially alter commercial calculus. Examples include regulatory approvals expanding indications for AR inhibitors and radioligand therapies, and late‑stage clinical presentations that may support earlier use of established agents.

Notable milestones: FDA approval activity in 2025 for expanded indications of radioligand therapy and AR inhibitors, and presentation of pivotal Phase 3 data in 2026 that could enable label expansion into localized high‑risk populations. These events are front‑loaded catalysts for 2026 go/no‑go decisions on launches, manufacturing scale, and payer engagement.

The market is characterized by a mix of large integrated pharmas, diagnostic specialists, imaging OEMs, and emerging radiopharmaceutical firms. The top companies control a meaningful share of revenue, creating a competitive environment where scale, regulatory depth, and diagnostic linkages confer advantage. Key strategic profiles and implications include:

Johnson & Johnson (Janssen): A vertically integrated therapeutic and companion‑diagnostic strategy with recent label expansions and late‑stage clinical data positions J&J to accelerate uptake where molecular selection is required. Recommendation: prioritize payer dossiers and diagnostic partnerships where J&J seeks to expand indications.

Astellas / Pfizer (co‑promotion): Their established androgen receptor franchise has broad penetration; patent expiries create downside risk but also partnership opportunities for generic and novel combination launches.

Bayer & AstraZeneca: Active in androgen receptor and PARP/targeted combinations — these players are likely to pursue earlier‑line claims and combination trials that will shape therapeutic sequences.

Novartis: Radioligand leadership with recent indication expansions signals supply‑chain and manufacturing scaling as strategic priorities; companies in the radiopharma ecosystem should evaluate CDMO tie‑ups and distribution partnerships.

Roche, Abbott, Myriad, MDxHealth, OPKO: Diagnostic leaders who are increasingly negotiating access value with therapeutic partners. For diagnostic firms the path forward is to demonstrate prospective clinical utility and cost‑offsets tied to therapy selection.

Siemens Healthineers, GE HealthCare, Lantheus, Telix: Imaging and radiopharmaceutical companies are catalysts for adoption — their commercial strategies dictate the pace at which PSMA‑PET becomes the standard staging tool in major markets.

Full market sizing and forecast model (2020–2032) with scenario toggles for regulatory and pricing shocks.

Clinical‑catalyst calendar and probability‑weighted impact analysis for every key Phase 2/3 program and recent label action.

Go‑to‑market playbooks for diagnostics, radioligand therapies, and combination oncology launches — including payer evidence timelines and commercial readiness checklists.

M&A and partnership heatmaps highlighting strategic targets by capability (diagnostics, manufacturing, distribution) and accretion scenarios over 24–36 months.

Regulatory and reimbursement sequencing maps for major markets, together with recommended dossier templates and real‑world evidence pilots.

Interactive pricing sensitivity and margin impact models to stress‑test investment cases under patent expiry, generic entry, and accelerated adoption scenarios.

Operational playbooks for radiopharmaceutical scale (cold‑chain logistics, centralized vs decentralized production, and QA pathways).

Corporate strategy / BD: Run a short list of diagnostic and radiopharma bolt‑on targets; prioritize deals that secure companion diagnostics or manufacturing capacity within 12–18 months.

R&D: Rebalance pipeline investments to include combination trials that can extend exclusivity or create differentiation as monoclonal AR inhibitors face downward pricing pressure.

Commercial / Market Access: Initiate payer pilots that couple PSMA‑PET utilization with improved outcomes and cost offsets; prepare value dossiers for radioligand therapies pre‑emptively.

Operations: Validate radiopharmaceutical supply chains and engage CDMOs for capacity buffering; invest in imaging service partnerships where diagnostics form the entry point for therapy selection.

Diagnostics teams: Move from analytic validity to prospective utility studies — the marketplace increasingly rewards demonstrated impact on therapeutic choice and downstream outcomes.

Use this briefing to prioritize hypotheses to validate in 2026: which indications will expand, which payer markets will set reimbursement precedents, and which modalities will drive portfolio differentiation. The full PW Consulting report provides the empirical foundation — downloadable financial models, regional access frameworks, segment‑level forecasts and a ranked list of near‑term clinical catalysts — to convert those hypotheses into executable plans. Our clients typically employ the report for strategic planning cycles, investment committee memos, and deal‑making diligence.

PW Consulting’s Prostate Cancer Diagnostics and Treatment Market report is intentionally designed as a pragmatic decision tool for 2026: it focuses on the levers that matter (regulatory timing, diagnostic linkage, payer evidence, manufacturing readiness) rather than a catalogue of static figures. To access the complete dataset, interactive models, and the full list of segment and regional tables that underpin the scenarios summarized here, please visit our publication page.

For detailed analysis of this topic, please visit the official page:Prostate Cancer Diagnostics And Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com