Внос на коли от САЩ за малък и голям бюджет

Crafts |

2026-05-11 13:22:26

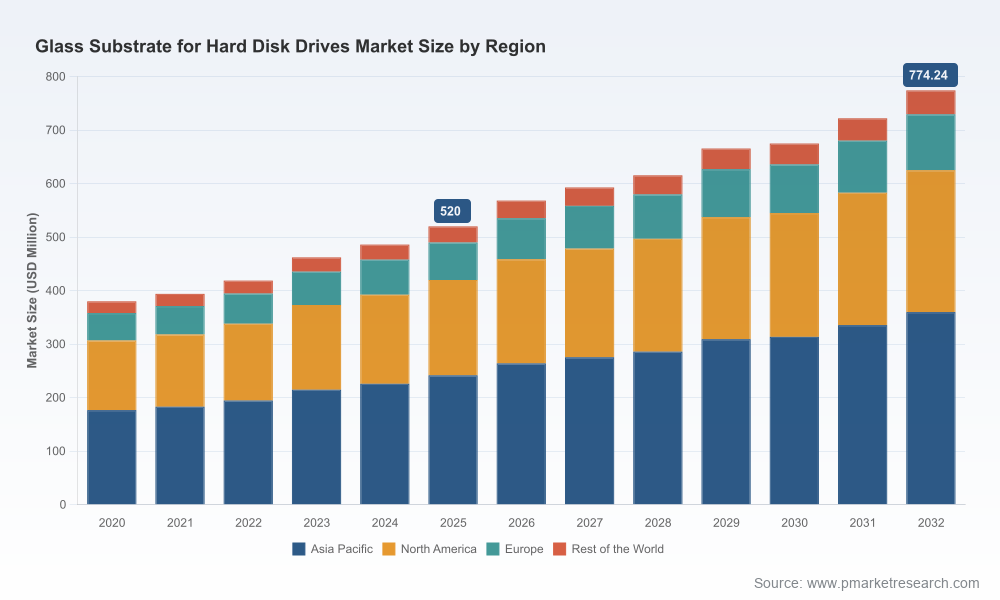

PW Consulting’s latest market study on glass substrates for hard disk drives (HDDs) reframes a maturing storage-materials market as one of the most consequential inputs for enterprise storage roadmaps in 2026. Anchored on a 2025 base year and informed by five years of historical dynamics (2020–2025), the report projects the addressable market to grow at a steady compound annual growth rate (CAGR) of 5.85% across the 2026–2032 forecast window, rising from an estimated USD 520 million in 2025 toward a substantially larger market by 2032. For decision-makers allocating capex, finalizing supplier strategies, or defining product roadmaps, this study is designed as an action-oriented intelligence package — deep enough to guide capital and commercial choices, but crafted to drive targeted engagement for full-data access.

Glass Substrate For Hard Disk Drives Market

Performance and roadmap enabler: Glass substrates are no longer a niche component; they are an enabler of higher platter counts, thinner mechanical designs, and thermal stability needed for advanced recording technologies such as heat-assisted magnetic recording (HAMR). For hyperscalers and enterprise OEMs, substrate choice materially impacts drive capacity-per-rack economics and reliability under sustained workloads.

Glass Substrate For Hard Disk Drives Market

Supply-side concentration: The supply base for precision glass substrates is highly concentrated and characterized by single-sourcing dynamics in critical size segments. That concentration introduces asymmetric supply risk — a strategic consideration for procurement, capacity hedging, and contractual terms.

Glass Substrate For Hard Disk Drives Market

Demand reorientation toward nearline workloads: Growth drivers are primarily tied to nearline/enterprise data-center demand, where density and durability premiumize glass over traditional substrates. The pace of cloud capacity growth, cold-storage strategies, and tiered-capacity architectures will therefore play a dominant role in substrate volumes.

Beyond headline forecasts, our analysis is structured to support three classes of stakeholders: corporate strategy teams, procurement and supply-chain leaders, and product development organizations. The full report includes:

A dynamic market-sizing and scenario model that allows users to toggle demand assumptions (cloud capex, archive storage uptake, HDD unit ASPs) and observe impacts on substrate volumes and value through 2032.

Supply-capacity maps and risk heatmaps showing geographic concentration of glass substrate capacity, near-term expansion projects announced by key manufacturers, and the timing sensitivity of those projects relative to demand inflection points.

Cost-curve analysis and raw-material sensitivity: a calibrated cost model that isolates the impact of primary raw-material swings and energy cost differentials on substrate unit economics, with stress-test scenarios for input-price volatility.

Supplier scorecards and negotiation playbooks: comparative operational KPIs, reliability metrics, technology readiness levels for HAMR compatibility, and recommended contractual terms to mitigate single-sourcing risk.

Technology and product roadmaps linking substrate characteristics (rigidity, thermal tolerance, manufacturability) to HDD design levers (platter count, head stacks, areal density), with recommended R&D priorities for OEMs targeting 40TB-class and above devices.

The market is defined by a small set of industrial-scale players with differentiated intellectual property and manufacturing know-how. Among them, one company stands out as the incumbent in global substrate manufacturing, particularly for smaller-diameter and increasingly for larger-diameter nearline platters. That firm’s manufacturing footprint, technology stack, and strategic investments are central determinants of market balance over the next 24–48 months. Recent public moves by manufacturers and HDD OEMs (including verified multi-disk stacking demonstrations and early sampling of glass-substrate nearline drives) validate a shift from evaluation to scaled commercialization.

For procurement and supply-chain teams, the implications are straightforward: supplier concentration combined with rising commercial demand requires active mitigation — diversified tiering strategies, longer lead contracts tied to capacity ramp milestones, and collaborative demand-forecast sharing to avoid inventory shocks or forfeited growth opportunities.

Raw-material and input-cost dynamics: Production economics for precision glass substrates remain sensitive to flux and soda-ash pricing, as well as energy and furnace emission controls. While commodity prices showed easing trends through 2025 into early 2026, volatility persists and can erode margins at the substrate level faster than downstream OEM price adjustments.

Environmental and regulatory pressures: Tighter CO2 and energy-efficiency regulations for glass manufacturing are accelerating investments in lower-emission furnaces and recycled-content recipes. These investments will influence regional cost positioning and may redirect new capacity to jurisdictions with supportive transition policies.

Technology convergence: HAMR-readiness, higher platter stacking, and ultra-thin hub designs increase the technical bar for substrates. Suppliers that demonstrate consistent dimensional tolerance, improved heat resistance, and yield-friendly processing will capture premium demand.

Short term (next 6–12 months): Secure forward visibility. Negotiate volume-flex agreements with embedded options tied to measurable capacity ramps, and initiate supplier audits focused on capacity expansion timelines and process stability. Update procurement scorecards to include substrate-specific KPIs such as thermal resistance certification and glass-grade traceability.

Medium term (12–36 months): Co-invest selectively. For OEMs and strategic suppliers, consider joint investment vehicles or long-term offtake arrangements to underwrite new capacity that aligns with the projected nearline demand curve. Prioritize partnerships that deliver technology transfer for HAMR-compatible substrate manufacturing.

Long term (36+ months): Diversify materials and design architecture. Build optionality into product lines through modular mechanical designs that can accommodate multiple substrate types, and maintain R&D investment in alternative materials and recycling processes to hedge against supply and regulatory shocks.

Validate capital plans against substrate availability: Ensure that planned drive launches and capacity targets are reconciled with supplier capacity timelines and announced plant projects.

Incorporate raw-material sensitivity into financial models: Stress-test EBITDA and gross-margin scenarios for substrate cost spikes and slower-than-expected price pass-through.

Design supplier KPIs tied to technology readiness: Require substrate partners to certify compatibility with target recording technologies and provide yield guarantees tied to accepted test protocols.

Assess geopolitical and regulatory exposure: Map supply routes, energy-policy risks, and environmental compliance costs that can create regional cost differentials over the forecast horizon.

Consistent with a “trailer” approach, this executive preview is designed to convey the strategic contours and operational levers that will matter most in 2026 without exposing the granular tables and supplier-share matrices that drive transactional decisions. The complete report contains detailed regional and application splits, segmented pricing curves, and a granular supplier market-share model — all essential for contract negotiation, M&A diligence, or build-or-buy analyses. To preserve the integrity of proprietary inputs and to encourage targeted client engagement, those detailed exhibits are reserved for the full release.

Custom scenario workshops: We will run tailored sessions that inject your demand forecasts into our substrate model and identify critical timing mismatches or supply bottlenecks.

Supplier due diligence programs: From on-site audits to technical validation of substrate properties, we can operationalize the supplier scorecards contained in the full study.

M&A and strategic sourcing support: For corporates and private-equity sponsors assessing upstream entry or off-take structures, we offer valuation-grade models and integration playbooks.

For procurement directors, product chiefs, and C-suite leaders responsible for storage strategy, this report supplies the intelligence needed to move from reactive sourcing to anticipatory planning. The glass-substrate market is no longer an obscure line item — it is a determinant of capacity economics, product differentiation, and supply resilience. PW Consulting’s full report provides the data, models, and playbooks required to convert that understanding into strategic advantage for 2026 and beyond. Access details and the complete dataset are available on our report page.

For detailed analysis of this topic, please visit the official page:Glass Substrate For Hard Disk Drives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com