Cell Culture Media for Research: Strategic Intelligence for 2026 Decisions

PW Consulting — Executive Brief

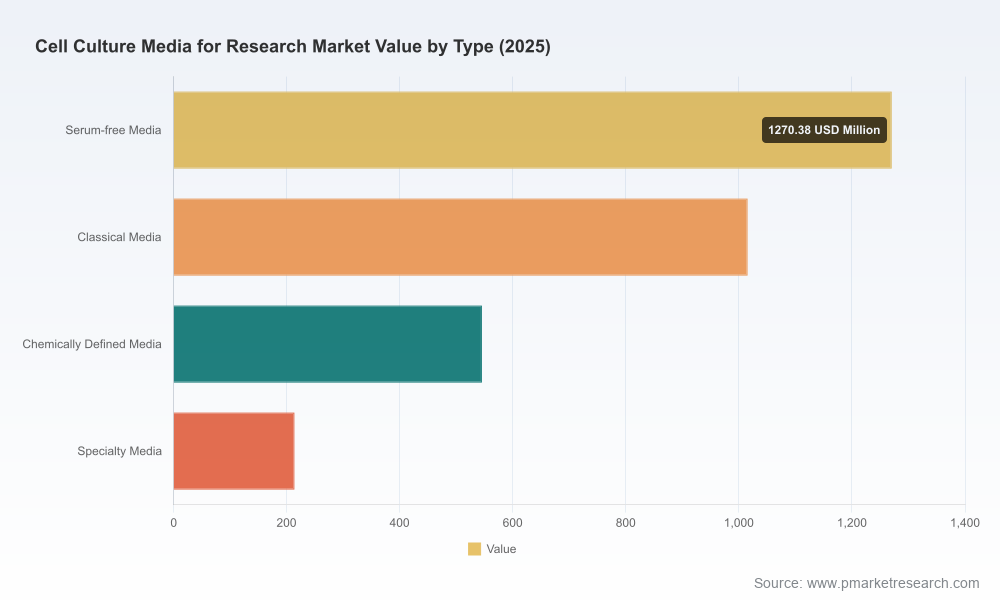

As laboratories, biotechs and academic groups recalibrate research roadmaps in 2026, cell culture media have moved from a tactical procurement line-item to a strategic lever for reproducibility, scalability and regulatory readiness. Our new Cell Culture Media for Research Market report — anchored on a 2025 base year and a forward-looking 2026–2032 forecast — distills the commercial realities that will shape investment, sourcing and product strategies this year. The global market reached approximately USD 3.05 billion in 2025 and is forecast to expand at a compound annual growth rate of 8.45% through the forecast horizon, reaching the mid-single-digit billions by 2032 under the scenarios modeled in this study.

Cell Culture Media For Research Market

Why this report matters to executives in 2026

- Macro momentum is strong. Sustained R&D investment across biologics discovery, cell and gene therapy enabling platforms, and advanced in vitro models is driving consistent demand growth for research-grade cell culture media.

- Product mix is shifting. The industry-wide move toward serum-free and chemically defined formulations is no longer an R&D fad — it is a procurement imperative that reduces batch variability and accelerates downstream transfer to regulated processes.

- Supply-side fragility is real. Key raw-material traceability and sourcing issues — from growth factors to specialty amino acids and serum alternatives — create vulnerability for labs that have not hardened supplier strategies and qualification pathways.

- Concentration matters. The market exhibits meaningful channel concentration among the top players, which shapes pricing dynamics, service expectations and partnership models for outsourced media development.

What the report delivers — practical, decision-grade content

This study is designed as an operational playbook for 2026 decision cycles. It combines quantitative market sizing and scenario-based forecasting with granular, executable modules that support board-level and operational decisions. Key deliverables include:

Cell Culture Media For Research Market

- Proven methodology and transparent assumptions: historical reconciliation (2020–2025) and a clear, stress-tested forecast (2026–2032) denominated in USD (report base year 2025).

- Demand-driver analysis: mapping the downstream value chain (discovery, regenerative medicine, cancer models, basic research) to identify where media choices materially impact reproducibility and time-to-result.

- Supply-chain heat maps: supplier concentration, critical raw-material flows, and traceability risk assessments with mitigation options for procurement teams.

- Commercial benchmarking: a vendor scorecard covering product breadth, technical support, global manufacturing footprint, and go-to-market models — enabling rapid vendor shortlists for partnerships or outsourcing.

- Innovation and product pipeline review: technology trajectories for chemically defined media, serum alternatives and integrated systems (media + cultureware + analytics), with commercialization readiness levels for each class.

- Scenario planning & sensitivity analysis: upside and downside demand cases tied to macro R&D spend, adoption curve assumptions for defined media, and regulatory shifts affecting RUO-designated products.

- M&A and partnership playbook: criteria-driven screening to identify targets that deliver capability uplift (e.g., media formulation IP, analytical QC platforms, or regional manufacturing scale).

- Actionable recommendations: prioritized 90/180/360 day roadmaps for R&D leaders, procurement, and corporate development teams — including pilot modalities and KPIs for rollouts.

Competitive landscape — what incumbent players are doing in 2026

Market leadership remains concentrated among a handful of global suppliers that combine deep formulation expertise with extensive application support and global logistics. These companies — spanning legacy life-science distributors, specialist media manufacturers and integrated bio-supply platforms — are pursuing distinct strategies:

Cell Culture Media For Research Market

- Large platform suppliers are leveraging breadth. Global life-science companies continue to capitalize on diversified portfolios (basal media, serum-free formulations, chemically defined solutions and supplements) and scale advantages in manufacturing and distribution to support reproducible research outcomes and multi-site studies.

- Specialists are capturing niche science. Firms focused on stem cells, primary cells and organoid systems differentiate through media formulations tailored to delicate cell types and by offering application-specific technical support that accelerates adoption in advanced in vitro models.

- Regional and price-sensitive providers address access. Cost-competitive manufacturers remain important for academic labs and smaller biotech firms, especially where budget constraints coexist with high-volume teaching and screening workflows.

- Service-augmented players are doubling down. The emergence of media development labs and in-situ optimization services — exemplified by recent facility and service launches — signals a market shift: customers are buying outcomes (robust cell expansion or assay-ready systems), not just SKU lines.

Recent product introductions and service launches underscore these trajectories. In early 2026, high-profile product kit launches targeted accelerated cell-line development workflows and CHO productivity, while media development labs opened to provide rapid optimization and scale-up support for customers seeking to bridge research and bioprocessing. These moves reinforce that proprietary formulation expertise and rapid application support are becoming prime competitive differentiators.

Regulatory and raw-material dynamics to watch

- RUO designation remains a gating factor. Many research-grade media are explicitly labeled for Research Use Only, requiring additional qualification before use in diagnostic or therapeutic manufacturing contexts. Companies planning translational pathways must map qualification steps early to avoid costly reformulation later.

- Traceability and supply-chain resilience are strategic priorities. Global sourcing of critical components introduces traceability gaps — an issue that procurement and quality functions must address via supplier audits, dual-sourcing strategies and increased inventory buffers for high-risk components.

- Serum sourcing constraints persist. Limitations on certified serum collection channels continue to pressure serum-supplemented formulations and accelerate the move to serum-free or chemically defined alternatives.

Strategic implications — recommended actions for 2026

Based on our analysis, PW Consulting recommends that organizations align short-term initiatives to long-term platform goals. Four practical actions rise to the top:

- Prioritize chemically defined and serum-free pilots now. Deploy controlled side-by-side studies to quantify variability reduction and downstream transferability; use the findings to re-specify procurement contracts within 6–12 months.

- Harden raw-material strategies. Map single-source exposures for key components, add mandatory traceability clauses to supplier contracts, and develop a qualified alternate-supplier list for critical inputs.

- Invest in partnership-based development. Seek suppliers that offer co-development capabilities (media development labs, formulation support) to accelerate transfer from discovery to scalable processes.

- Embed market intelligence into your investment thesis. For investors and corporate development teams, use concentration metrics and vendor roadmaps to prioritize targets that provide either proprietary formulation IP or scalable production capacity aligned with long-term adoption curves.

How to use this report in your 2026 planning cycle

The report is structured to be immediately actionable in boardroom and operational settings:

- For the C-suite: a concise strategic executive summary with scenarios and a prioritization matrix to inform capital allocation and M&A focus.

- For procurement heads: a supplier qualification checklist, risk heatmap and negotiation playbook to contract for resilience and technical support.

- For R&D leaders: standardized pilot protocols and acceptance criteria to evaluate serum-free/chemically defined replacements without disrupting ongoing programs.

- For investors and BD teams: a screening framework to identify acquisition targets that materially accelerate time-to-market or reduce cost-of-goods for cell-therapy enabling platforms.

What we deliberately withhold here — and why

This article purposefully presents high-level market sizing, growth rates and strategic imperatives while withholding detailed segment breakdowns, region-by-region shares and application-level revenue splits. That granular intelligence — including our regional channel models, application-specific adoption curves and vendor revenue benchmarks — is contained in the full PW Consulting report and associated datasets. We take a “show expertise, protect client-level detail” approach: enough insight to enable strategic thinking, but withholding the drill-down tables that are most valuable to competitive and procurement decision-making.

Next steps

To operationalize the insights above, PW Consulting offers tailored briefings and rapid-deployment workshops that map the report’s recommendations to your organization’s operating model. The full report includes the scenario-modeled market forecast (2026–2032), granular vendor benchmarking, a quantified risk register for raw-materials, and a playbook for media-driven product and portfolio decisions.

Contact PW Consulting to schedule a briefing and receive guidance on integrating the report into your 2026 strategic planning cycle. For immediate access to the full dataset and downloadable report, visit the PW Consulting publications portal.

For detailed analysis of this topic, please visit the official page:Cell Culture Media For Research Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com