Supply Chain IT Transformation Services for Retail Market — Strategic Briefing for 2026 Decision-Makers

As retailers enter a decisive inflection point in 2026, the latest PW Consulting market study — Supply Chain IT Transformation Services for Retail Market (base year 2025) — synthesizes market dynamics, vendor capabilities, practical implementation guidance, and regulatory imperatives to help senior executives convert disruption into competitive advantage. This briefing summarizes the strategic value of the report for boardrooms and transformation offices, highlighting the macro trajectory, competitive posture, and the prioritized choices that will shape capital allocation and program design in the year ahead. For full segmented datasets, vendor scorecards, and operational playbooks, access the complete report on our site.

Supply Chain IT Transformation Services for Retail Market

Executive Snapshot: Why 2026 Is a Pivotal Year

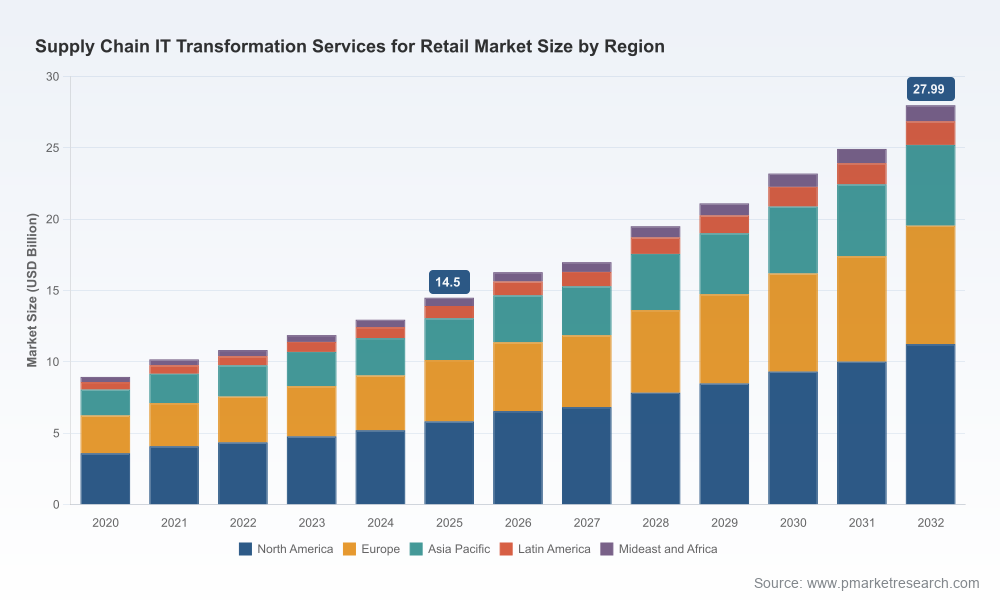

The market for Supply Chain IT Transformation Services in retail has moved from early adoption to broad strategic deployment. According to our base-year accounting, the market expanded from USD 8.95 Billion in 2020 to USD 14.5 Billion in 2025. Our forecast projects continued momentum, reaching approximately USD 28.0 Billion by 2032 at a compound annual growth rate of 9.85% over the forecast period. This growth reflects retail leaders shifting from point optimizations to integrated IT transformations that realign networks, inventory policies, fulfillment options, and technology stacks around customer expectations and regulatory imperatives.

Supply Chain IT Transformation Services for Retail Market

For executives planning 2026 budgets, the implication is clear: investment windows favor integrated programs that deliver measurable resilience and agility. The pace of vendor innovation and the parallel rise of platform and managed-service offerings mean that decision velocity — choosing the right partner, scope, and commercial model — will materially affect time-to-value and long-term TCO.

Supply Chain IT Transformation Services for Retail Market

What the PW Consulting Report Delivers (Practical, Actionable Content)

- Strategic frameworks for prioritizing IT transformation levers (data & analytics, AI/ML forecasting, orchestration layers, fulfillment automation, cloud migration).

- Operational blueprints and phased implementation roadmaps mapped to retailer archetypes (e.g., multi-format grocers, specialty apparel, omnichannel general merchandisers).

- Vendor assessment methodology and executive-ready scorecards that evaluate delivery capabilities, solution maturity, partnership ecosystems, and risk profiles.

- Procurement playbooks that align commercial models (capex vs opex, outcome-based contracts, managed services) with governance, KPIs, and migration milestones.

- Regulatory compliance checklists and data architecture patterns to meet traceability, privacy, and sustainability mandates without compromising customer experience.

- ROI modelling templates and sample business cases that translate technical investments into measurable supply chain outcomes for 12–36 month horizons.

The report purposefully pairs strategy with execution — not as a high-level manifesto, but as a toolkit for CIOs, heads of supply chain, and transformation leads preparing board-level approvals and procurement packages in 2026.

Market Dynamics Shaping 2026 Decisions

Three converging forces explain the market’s trajectory and should guide executive priorities in 2026:

- Technology maturation and economic rationale: AI-driven planning and orchestration moved from pilots to production, and industry data shows a rapid uptick in adoption. One major industry outlook notes current adoption for AI-enabled visibility at roughly 30%, with expectations to reach around 41% within a year — a pace that will force laggards to reevaluate risk exposure.

- Regulatory and sustainability requirements: New regulatory regimes — for example, EU packaging directives and extended producer responsibility frameworks — require traceability, recycled-content reporting, and digital passports. These rules create an imperative to embed compliance into core supply chain IT rather than bolt it on later.

- Labor and operating-cost pressure: Rising labor costs and jurisdictional changes to working hours and pay transparency increase the value of automation, workforce optimization, and better demand-supply matching, all of which rest on modern IT foundations.

These dynamics mean that investments in planning, fulfillment orchestration, and traceability are not optional—they are central to sustaining competitiveness and managing regulatory and margin risk.

Competitive Landscape: How to Read Vendor Positioning

The market exhibits a moderate level of concentration: the top three and five providers capture a meaningful portion of spend but do not dominate it entirely. This positioning creates room for both large systems integrators and focused specialists. Our vendor analysis emphasizes three practical lenses for selection:

- Capability breadth and ecosystem depth. Larger firms combine advisory, systems integration, and managed services, enabling end-to-end programs but sometimes at higher cost and longer lead times. Look for demonstrable partnerships with cloud and platform vendors, packaged IP for retail use cases, and a track record of complex, multi-year transformations.

- Domain specificity and speed of deployment. Mid-sized firms and boutiques bring deep retail supply chain expertise and prebuilt accelerators for forecasting, inventory optimization, and fulfillment. These players can reduce implementation risk and deliver earlier benefits in tightly scoped use cases.

- Business model fit and outcomes orientation. Increasingly, retailers prefer outcome-linked commercial constructs — e.g., gain-shares on cost-to-serve reductions or subscription models for continuously managed forecasting services. Vendors willing to align commercial risk with performance will be more attractive to budget owners focused on ROI.

Representative competitors in the landscape include global integrators leveraging breadth and scale, consultancies emphasizing strategy and transformations, legacy technology firms offering platform-centric solutions, and specialized consultancies focused on retail forecasting and fulfillment. Each class of provider has a distinct role depending on program scale, desired speed, and internal capability.

Company Highlights — Strategic Readings (Non-Exhaustive)

- Tata Consultancy Services (TCS): Recognized for end-to-end supply chain transformation capabilities and partnership-led implementations; suited for large, complex retail/CPG transformations where execution depth is the priority.

- Cognizant: Focused on digital transformation for planning, forecasting, and visibility; appropriate for retailers seeking modernization with strong delivery models across legacy and cloud platforms.

- Accenture: Emphasizes network orchestration, AI, and automation across end-to-end supply chain transformations; a fit for retailers targeting ambitious, integrated programs.

- Deloitte and PwC: Provide strategy-led transformation and compliance-focused offerings, with advisory depth aligned to regulatory, sustainability, and large public-company governance needs.

- IBM: Leverages analytics and AI playbooks, particularly for e-commerce and predictive operational strategies.

- Specialists (e.g., Parker Avery, Brillio): Deliver deep retail domain expertise and rapid enablement in forecasting, inventory optimization, and fulfillment technologies; effective where speed and low disruption are critical.

Recent recognitions and market commentary — including analyst placements and 2026 industry outlooks from major consultancies — corroborate that leaders combine advisory depth with delivery scale. However, the market also rewards niche expertise and practical accelerators that reduce implementation time and risk.

Procurement and Implementation Imperatives for 2026

For retailers committing to transformation programs in 2026, PW Consulting recommends a disciplined approach to procurement and program architecture:

- Start with clearly defined business outcomes and measurable KPIs (inventory turns, fill rate, fulfillment cost per order, carbon footprint per SKU) rather than technology wish lists.

- Favor phased delivery with rapid value checkpoints: proof-of-value, followed by a scale wave, then operationalization via managed services to lock in benefits.

- Design data and integration layers up front to enable future portability of models and to meet privacy and traceability requirements — retrofit is expensive and slow.

- Consider blended commercial models that balance capital constraints with the desire for vendor accountability; outcome-based contracts can align incentives when metrics are well specified.

- Assess organizational readiness: transformation success hinges on change management, new governance processes, and capability uplift within planning, supply chain, and IT teams.

Risk Signals and Red Flags

- Overreliance on point solutions without orchestration layers that unify planning, fulfillment, and network decisions.

- Lack of a compliance-ready data architecture in contexts where packaging, traceability, and privacy rules are tightening.

- Vendors unable to demonstrate measurable outcomes in comparable retail formats or unwilling to tie commercial terms to delivery milestones.

How PW Consulting’s Report Accelerates Decision-Making

Beyond the strategic analysis summarized here, our full study provides operationally focused artifacts to accelerate procurement and delivery: validated ROI models, implementation checklists, vendor scorecards, use-case playbooks, and compliance templates for emerging packaging and data regulations. These resources are designed to shorten due diligence cycles, reduce procurement ambiguity, and provide boards with defensible evidence in 2026 investment decisions.

Importantly, we preserve confidentiality and commercial sensitivity by withholding granular segmentation tables and vendor-specific scoring in this public briefing. Those datasets — including regional, offering-type, and application-level segmentations that underpin our conclusions — are available within the full report and supporting data annexes.

Next Steps for Executives

- Use the market trajectory and strategic frames in this briefing to stress-test your 2026 budget and roadmap scenarios.

- Request a tailored briefing or workshop from PW Consulting to align the report’s playbooks with your enterprise architecture and operating model.

- Access the full report to obtain the segmented market data, vendor scorecards, and implementation templates necessary to finalize procurement and governance decisions.

PW Consulting’s Supply Chain IT Transformation Services for Retail Market report translates where the market is today — and how it will shape outcomes through 2032 — into concrete choices for 2026 leadership. For the full datasets, granular vendor evaluations, and the actionable blueprints referenced here, please visit our report page or contact our advisory team for a confidential executive briefing.

For detailed analysis of this topic, please visit the official page:Supply Chain IT Transformation Services for Retail Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com