Latteholic Coffee Collection – Espresso Machines, Coffee Beans & Accessories

Shopping |

2026-06-30 07:38:08

PW Consulting’s latest market study on Lacrimal Stent Tubes provides a focused, decision-ready perspective for executives, product teams, and corporate development professionals planning for 2026. Combining rigorous historical trend analysis (2020–2025) with a 2026–2032 forecast horizon, the report quantifies a steady recovery and structural growth in tear‑drainage devices—anchored by a 5.48% compound annual growth rate—and translates those figures into actionable strategic options. This press release summarizes the report’s strategic value, outlines the analytic approach and practical content, and highlights competitive and regulatory dynamics essential for near‑term planning. For full segment-level tables, transaction models, and vendor scorecards, refer to the full report page.

Lacrimal Stent Tube Market

Timing: 2026 is a pivot year where elective procedure volumes and outpatient surgical capacity are expected to normalize post‑disruption. Our analysis integrates this operational rebound and isolates persistent demand drivers versus transient tailwinds.

Lacrimal Stent Tube Market

Clarity amid fragmentation: The lacrimal stent ecosystem spans single‑use intubation sets, self‑retaining stents, glass bypass tubes, and supporting instruments. The study synthesizes cross‑product dynamics into decision levers—pricing, channel mix, and regulatory pathway choices—relevant to market entrants and incumbents alike.

Lacrimal Stent Tube Market

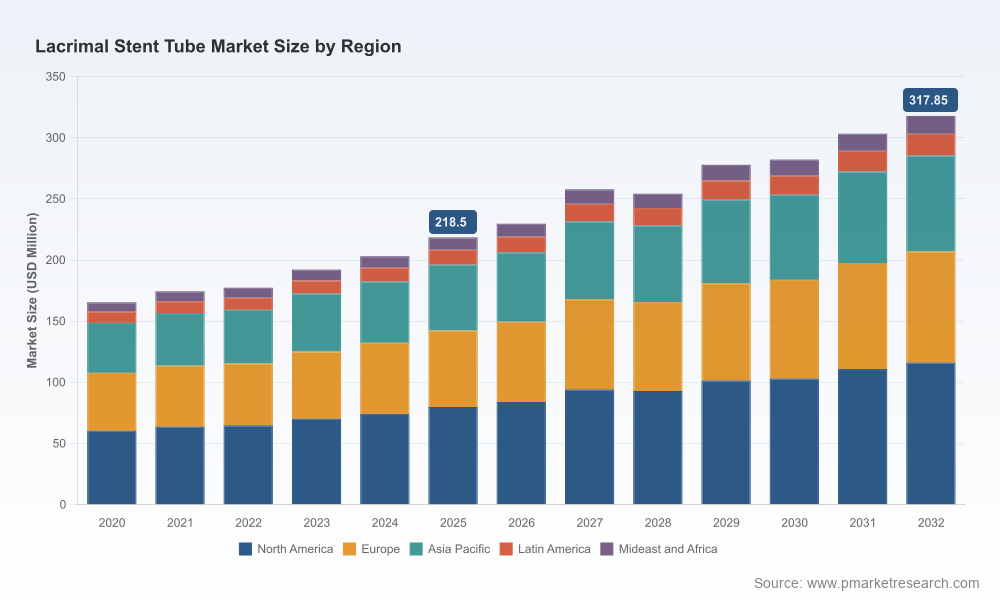

Financial framing: Using 2025 as the base year, the market size and trajectory through 2032 are projected to guide resource allocation. The projected mid‑single digit CAGR provides a stable backdrop for portfolio investments and M&A theatres that seek predictable, low‑volatility returns in specialty ophthalmic devices.

Market sizing and growth scenarios: We model a base and two sensitivity paths across the 2026–2032 forecast window. Readers receive a clear revenue trajectory and a set of trigger moments (regulatory shifts, reimbursement updates, clinical guideline changes) that would move the market between scenarios.

Commercial playbooks: For manufacturers and distributors we provide go‑to‑market blueprints for three archetypes—global incumbent, regional challenger, and cost‑focused supplier—each with recommended channel mixes, pricing strategies, and stakeholder engagement frameworks.

Regulatory and reimbursement routing: The report maps 510(k) clearance pathways relevant to lacrimal devices, practical considerations for labeling and sterilization validation, and a payer engagement guide tied to CPT coding practice. This helps regulatory teams and market access leads build concise submission and coverage plans.

Clinical adoption levers: We identify the clinical touchpoints most influential to device adoption (surgeon training needs, procedure workflow, and perioperative care) and translate them into pilot designs and value‑dossier structures to accelerate uptake.

Manufacturing and sourcing checklist: Given the material importance of silicone and the niche role of specialized glass, the report includes a vendor qualification matrix, sterilization pathway options, and unit economics sensitivity models to support procurement and operations planning.

M&A and partnership intelligence: The study flags target profiles, valuation ranges by business model, and integration risks for roll‑up strategies in specialty ENT/ophthalmic consumables.

Using 2025 as the base year, our modeled market demonstrates a steady expansion through 2032. The mid‑single digit CAGR (5.48%) reflects a combination of rising procedural volumes, incremental product innovation (coatings, delivery systems), and broader access in outpatient surgical sites. This growth is robust enough to support targeted investments (clinical studies, expanded sterilization capacity) while not so rapid as to erode pricing discipline across established channels.

The lacrimal stent market is competitive but specialized. A cluster of dedicated ophthalmic device firms and a handful of broader surgical portfolio players are directly shaping the product and service ecology. Key firms we track include established specialists and compelling regional manufacturers:

FCI Ophthalmics (Pembroke, MA, USA) — a leading specialist with a broad range of lacrimal stents and delivery systems, notable for self‑retaining bicanalicular and monocanalicular designs. Their continued product focus and sustained clinician engagement keep them centrally placed in surgeon preference maps.

Kaneka Medical (Osaka, Japan; US operations) — a technology‑led supplier emphasizing hydrophilic coatings and simplified insertion systems aimed at both congenital and acquired indications.

bess medizintechnik (Germany) — a regional engineering‑centric supplier whose surgical instruments and stenting solutions are influential in ENT/head‑and‑neck practice settings.

Aurolab (Madurai, India) — a high‑volume, cost‑competitive manufacturer providing silicone intubation sets and stents tailored to price‑sensitive markets and high‑throughput clinics.

Gunther Weiss (Hillsboro, OR, USA) — a legacy supplier of specialized glass bypass tubes used in long‑term CDCR applications, representing a unique niche with distinct clinical workflow and sterilization demands.

Beaver‑Visitec International (BVI Medical) — integrates lacrimal consumables into a broader ophthalmic surgery portfolio and recently strengthened its specialty procedure offering to support lacrimal applications.

Recent corporate moves reflected in our tracking—portfolio strengthening at BVI, renewed product emphasis at FCI, and clinical engagement events—signal that incumbents are investing along three vectors: clinician training, incremental device enhancements, and channel strengthening. For new entrants, these vectors define where differentiated value must be created: seamless delivery systems, demonstrable procedural time savings, or meaningful cost advantages.

Regulatory: Most lacrimal stents and intubation sets align with Class II device controls and are typically cleared via 510(k) pathways in the U.S. Practical guidance in the report helps teams scope predicates, common performance endpoints, and sterilization validation expectations.

Reimbursement: Procedural coding (for example, CPT provisions that cover nasolacrimal duct probing with stenting) supports economic viability in outpatient settings. Our reimbursement playbook translates coding nuances into hospital budget impact and ambulatory surgery center contracting templates.

Material & process: Silicone remains the dominant material due to biocompatibility and flexibility; specialized glass continues to serve a small but strategically important bypass niche. Sterility claims (single‑use, validated radiation or equivalent sterilization) are table stakes—our manufacturing chapter provides a checklist for sterile barrier systems, validation milestones, and CAPEX implications.

Prioritize productized clinician engagement: Short, procedure‑focused training packages and simulation kits materially reduce adoption friction. Allocate a portion of 2026 commercial budgets to surgeon champions and value‑demonstration pilots.

Optimize portfolio breadth vs depth: Incumbents with broad ophthalmic offerings should consider bundling lacrimal items into holistic DCR/CNLDO procedural kits; challengers should focus on a single high‑value device (e.g., novel self‑retaining design) and win depth before breadth.

Design for sterilization economics: Given sterilization is both a regulatory and cost driver, firms should model the tradeoffs between outsourced contract sterilization and in‑house capacity expansion when planning 2026‑2027 manufacturing investments.

Explore asymmetric M&A: Small‑scale acquisitions that add specialty instrument capability, regional distribution, or coating chemistry can accelerate market access without a full platform acquisition. Target diligence should include surgeon preference alignment and SKU rationalization risk.

Manage pricing discipline: With steady, mid‑single digit growth expected, avoid commoditization by locking in differentiated clinical outcomes and creating bundled pricing options that reflect the device‑plus‑service value proposition.

Our report is structured to move organizations from insight to action: market sizing and scenario models; a prioritized investment matrix; product commercialization playbooks; and a vendor/partner shortlist with readiness assessments. While this release outlines the strategic contours and operational levers, the full report supplies the proprietary tables, segment breakouts, downloadable financial models, and scorecards that executives use to finalize 2026 budgets and board presentations.

The lacrimal stent tube market in 2026 represents a disciplined growth opportunity for firms that align clinical utility, regulatory execution, and channel strategy. PW Consulting’s study offers the road map and tactical checklists to convert forecasted growth into durable share gains. To access the complete dataset, segment worksheets, and bespoke advisory options, please visit the PW Consulting report page and request the full Lacrimal Stent Tube Market report.

For detailed analysis of this topic, please visit the official page:Lacrimal Stent Tube Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com