https://www.facebook.com/CraveBalanceReviews2026

Art |

2026-06-08 15:39:29

As enterprises recalibrate supply chains and product roadmaps for the AI and 5G era, the Lowdk glass fiber cloth market has moved from a niche materials conversation to a strategic boardroom topic. PW Consulting’s latest market study — covering historical performance through the 2025 base year and a detailed forecast to 2032 — distills where value will concentrate, where risk is crystallizing, and which tactical moves in 2026 will materially change competitive positioning.

Lowdk Glass Fiber Cloth Market

Market trajectory: After steady expansion from approximately USD 535 million in 2023 to USD 625.5 million in 2025, the market is forecast to grow to roughly USD 676.5 million in 2026 and reach about USD 1,082.5 million by 2032, tracking an 8.15% CAGR over the forecast horizon.

Lowdk Glass Fiber Cloth Market

Structure and concentration: The market shows meaningful clustering among a handful of global players — our analysis places the combined share of the top three firms north of the mid‑50s, with the top five approaching the high 60s (CR3 ≈ 52.5%; CR5 ≈ 68.4%). This creates differentiated supplier power along the technology and premium product axes.

Lowdk Glass Fiber Cloth Market

Near‑term dynamics: Supply constraints, upward ASP pressure on premium glass variants, and geopolitically driven capacity shifts are the dominant operational risks companies must manage in 2026.

Several intersecting forces make 2026 the year when decisions will lock in multi‑year outcomes. First, end‑market pull from AI servers, high‑speed networking, and the ongoing roll‑out of advanced 5G infrastructure has increased demand for ultra‑low‑loss and low‑CTE fabrics. Second, supply‑side moves — new fiber launches, regional capacity additions, and select supplier price actions — have tightened the window for securing differentiated materials without incurring premium lead times or margins. Third, geopolitical considerations have accelerated regional diversification strategies, prompting some buyers to re‑optimize sourcing footprints.

Demand profile: Our bottom‑up demand model quantifies pull from server farms, telecom CCLs, and automotive radar/ADAS applications and validates the macro CAGR of 8.15% to 2032. Importantly, growth is non‑uniform: higher frequency and AI‑oriented applications are structurally outgrowing legacy uses, creating premium pricing pockets.

Supply bottlenecks: Lead times for advanced low‑Dk and low‑CTE cloths have elongated materially and — based on supplier capex cycles and announced projects — are likely to remain extended through mid‑2027. This is compounded by episodic raw‑material tightness and selective price increases by leading upstream players, which has immediate margin and sourcing implications for downstream integrators.

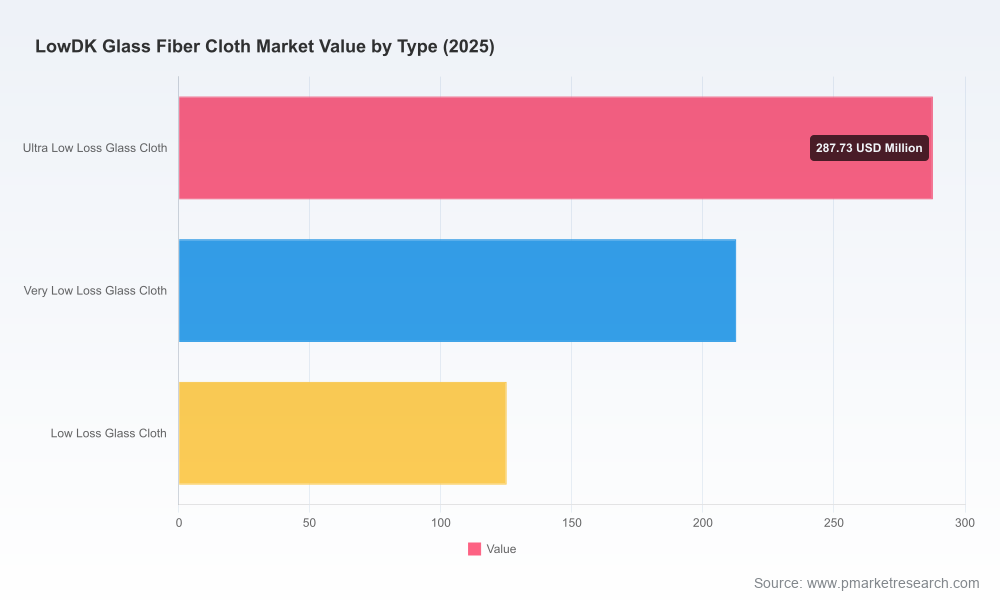

Pricing dynamics: Premium specialty glass variants trade at a substantial multiple of standard E‑glass ASPs. Buyers should expect sustained ASP differentials that reflect technical complexity and limited near‑term capacity elasticity.

The market is stratified between vertically integrated glassmakers, dedicated specialty fiber producers, and textile weavers that translate yarn into electronics‑grade cloth. Key strategic moves in 2025–2026 illustrate the competitive playbook:

Nittobo (Nitto Boseki): A dominant integrated supplier with deep IP in NE and T‑glass variants. Their ability to control both specialty fiber and cloth processing creates a durable advantage in advanced low‑Dk and low‑CTE segments.

AGY: Focused investments in U.S. capacity and a product set tailored for AI PCB and semiconductor packaging use cases position them as a pivotal Western supplier. Their announced expansion and strategic partnership activity are explicit responses to onshore demand for secure supply.

Taiwan Glass, Fulltech, Nan Ya, Asahi Kasei, and established Chinese producers: These firms are expanding or upgrading production capability to capture AI and 5G‑driven demand. The nuance lies in whether they move up the value chain (toward ultra‑low loss cloth) or double down on high‑volume, standard products.

JPS Composite Materials and other fabricators: Weavers and fabric converters who can integrate specialty yarns (sometimes through strategic partnerships) will be gatekeepers for many Western and regional PCB makers seeking compliance and performance.

Recent industry developments underscore the shifting supply map: new fiber introductions aimed at advanced semiconductors, targeted capacity investments in North America, collaborative fabrication projects to localize low‑CTE fabric production, and large‑scale electronic glass and fabric lines coming online in China. Collectively, these moves reduce single‑source risks over time but create a two‑ to three‑year period of elevated sourcing friction for buyers.

Procurement and supply strategy: Move from tactical spot buys to a portfolio approach. Prioritize long‑dated offtake agreements for ultra‑low loss grades, but retain optionality via partnership clauses and capacity release mechanisms. Hedge exposure to premium ASPs using index‑linked pricing or graded pricing corridors tied to feedstock indices where possible.

Product planning and roadmaps: Align roadmaps to material availability and cost trajectories. For companies developing next‑gen RF/mmWave modules or AI‑optimized server boards, prioritize design for manufacturability with multiple qualifying fabric types and clear substitution hierarchies.

Capex timing and location: Given extended lead times through mid‑2027, greenfield or brownfield investments for vertically integrating specialty fiber or local fabric conversion should be evaluated as multi‑year plays. Consider staged investments that can be accelerated or decelerated based on actual demand realization versus forecast scenarios.

M&A and partnerships: Targeted acquisitions or JV stakes in specialty weavers or high‑end yarn producers can rapidly de‑risk supply. Partnerships that replicate the AGY–JPS model (technical yarn supply + local weaving) are a pragmatic route to fast‑track regional secure supply.

Inventory and lead‑time management: Adopt a dynamic buffer strategy — increase safety stock for premium grades where switching cost is high, and apply leaner cycles for commodity fabrics. Convert part of inventory holdings into strategic safety‑stocks under long‑term agreements to avoid opportunistic spot spikes.

Our full study is built as an operational playbook rather than academic analysis. Key deliverables include:

Demand model with application‑level drivers and sensitivity scenarios (AI server growth, 5G deployment cadence, automotive radar uptake).

Supply‑side capacity map and timing model that reconciles announced projects, commissioning risk, and lead‑time impact.

Supplier scorecard and decision matrix: technology maturity, vertical integration, geographic risk, price dynamics, and contract flexibility.

Commercial playbooks for procurement: model contracts, indexation templates, and negotiation levers tailored to premium glass fabrics.

Investment templates and IRR scenarios for on‑shore vertical integration, greenfield weave capacity, and toll‑manufacturing options.

Scenario planning toolset: “fast demand / constrained supply”, “moderate demand / eased supply”, and “decoupled regionalization” scenarios tied to quantitative triggers.

Executives should treat the report as both a decision engine and an early‑warning system. Use the supplier scorecard to prioritize shortlisting partners for long‑term agreements; use the capex templates to size incremental investments against market CAGRs and internal hurdle rates; and use the scenario triggers to time inventory and contract hedges. For boards and strategy teams, the model provides a defensible narrative to stakeholders explaining why fiscal commitments in 2026 — be they procurement, capex, or M&A — are necessary to capture disproportionate upside in the latter half of the decade.

Two attributes distinguish our work: integration and operability. We marry granular technical understanding of glass chemistry and fabric performance with commercial levers (pricing, contract design, sourcing footprints) and provide executable tools that operations and procurement teams can implement within 90–180 days. Our conservative baseline — embedded in the 8.15% CAGR and the market sizing trajectory to 2032 — is complemented by upside and downside scenarios to stress‑test critical assumptions.

This article is intended to preview the decision‑grade intelligence in PW Consulting’s Lowdk Glass Fiber Cloth Market report. It highlights the strategic stakes and the types of choices organizations will need to make in 2026. To access the full dataset, supplier scorecards, downloadable Excel models, and step‑by‑step procurement playbooks (which include the granular segmentation and benchmarking we intentionally omit here), please visit our report landing page or contact our market practice leads.

In markets where materials become a bottleneck to innovation, timing and supplier strategy often determine who captures margin and who cedes volume. 2026 will be the year that separates companies that simply react to supply shock from those that reshape their supply base to win the next decade.

For detailed analysis of this topic, please visit the official page:Lowdk Glass Fiber Cloth Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com