Strategic Preview: Aviation Oxygen Systems Market — What Every Executive Should Know for 2026

As PW Consulting’s lead industry analyst, I present a focused executive briefing drawn from our forthcoming Aviation Oxygen Systems Market report (base year 2025, historical 2020–2025, forecast 2026–2032). This briefing is designed as a strategic “trailer” for senior leaders — airlines, OEMs, MROs, defense procurement offices, and private equity investors — to sharpen decision-making in 2026. It highlights high‑level market dynamics, structural forces, and the actionable levers that will matter most over the next planning cycle, while reserving detailed segment-level tables and models for the full report.

Aviation Oxygen Systems Market

Market trajectory and what it implies for 2026 planning

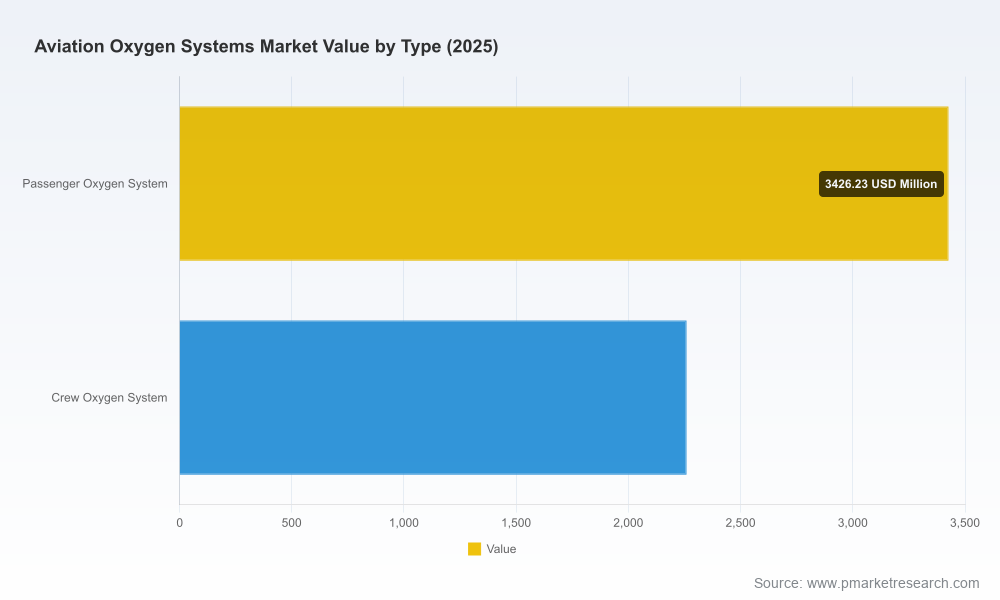

The aviation oxygen systems market has demonstrated resilient expansion across the recovery period following 2020. Total market value grew from roughly USD 4.12 billion in 2020 to approximately USD 5.69 billion in 2025, reflecting both demand recovery in commercial aviation and persistent requirements in military and general aviation. Our forecast shows the market expanding to about USD 6.02 billion in 2026 and tracking to roughly USD 9.01 billion by 2032, implying a compound annual growth rate (CAGR) of 6.8% for the 2026–2032 forecast window.

Aviation Oxygen Systems Market

Two immediate implications for 2026 corporate planning:

Aviation Oxygen Systems Market

- Investment windows are opening. The projected mid‑single‑digit to high‑single‑digit CAGR supports selective capital allocation to product lines that reduce total lifecycle cost (e.g., lightweight cylinders, pulse-demand regulators, integrated monitoring).

- Revenue upside is tied to services. Aftermarket services (MRO, cylinder testing, PBEs lifecycle management) will remain a primary, higher-margin growth domain as operators seek cost-efficient compliance and fleet availability.

Market structure and competitive dynamics — what the headline numbers hide

The market is moderately concentrated: the top three firms account for nearly half of the market by revenue, and the top five capture roughly two-thirds — a structure that favors incumbents with certified platforms and broad service footprints. That concentration creates a dual strategic posture for players in 2026:

- For incumbents: defend and selectively expand through M&A, certification portfolios, and integrated avionics/PSU partnerships to lock in fleet-level solutions.

- For challengers: focus on niche differentiation (weight, digital monitoring, pulse‑demand efficiency) and prove value through pilot programs with airlines and fractional operators.

These conclusions are drawn from a cross‑validated set of public filings, ADs, and primary interviews — and they underpin the defensive and offensive playbooks outlined in the full report.

Regulatory and airworthiness environment — planning for compliance as a strategic asset

Recent regulatory activity has elevated compliance risk into a strategic planning variable. In late‑stage 2025 and early 2026, regulators in major jurisdictions issued airworthiness directives affecting certain portable breathing equipment (PBEs), driving replacement mandates and tighter installation guidance. These actions underscore three operational imperatives for 2026:

- Inventory discipline: operators must reconcile parts and PBE inventories against AD timelines to avoid grounding risk and unplanned retrofit costs.

- Certified MRO network: expanding in‑house capabilities or contracting with FAA/EASA‑approved repair stations reduces lead time for hydrostatic testing, requalification, and emergency turnarounds.

- Product selection: prioritize suppliers with robust certification pipelines and transparent traceability for oxygen purity, cylinder testing, and replacement calendars.

In addition, longstanding regulatory requirements — such as supplemental oxygen mandates under 14 CFR Part 91.211 and hydrostatic testing intervals — continue to drive structural demand for cylinders, test services, and certified components. Our scenario analysis quantifies the cost of non‑compliance versus the economics of forward‑scheduled replacements; the full report provides executable timing matrices tailored to different fleet mixes.

Technology and product trends to watch

Innovation is concentrated in three domains that will materially shift procurement and service strategies by 2028:

- Delivery efficiency: pulse‑demand and smart regulators that reduce oxygen consumption and extend cylinder service intervals — lowering operational cost per flight hour.

- System integration: oxygen systems integrated with passenger service units, cabin environmental controls, and health monitoring platforms to enable preventative maintenance and situational awareness for inflight medical events.

- Digitalization of lifecycle management: cloud‑enabled tracking of cylinder hydrostatic tests, traceability, and compliance dashboards that reduce audit effort and inventory buffer needs.

For 2026 investment decisions, prioritize technologies that deliver measurable OPEX savings (reduced cylinder swaps, fewer unscheduled groundings) and those that ease certification burdens. The full report models time‑to‑payback for retrofit packages across operator archetypes.

Competitive landscape — capability maps and partnership lenses

Our competitive analysis maps capability, certification breadth, and service footprints for established suppliers. Highlights relevant to procurement and M&A due diligence include:

- Aerox Aviation Oxygen Systems (Bonita Springs, FL): a market leader in both portable and installed solutions for general and business aviation. The firm’s 2025 acquisition of an FAA‑certified repair station expanded MRO capability — an instructive example of vertical integration that shortens service lead times and strengthens aftermarket margins.

- Safran Aerosystems Oxygen / AVOX Systems (Lancaster, NY): deep expertise in masks, regulators, and portable systems for civil and military platforms. Recent regulatory scrutiny around PBEs raises short‑term replacement demand but also accentuates supply‑chain and certification risk for vendors and fleets relying on a small set of PBE models.

- Collins Aerospace (RTX, Charlotte, NC): delivers fully integrated oxygen and passenger service unit systems across commercial and military segments; its scale and avionics integration capability make it the default partner for major OEMs seeking turnkey solutions.

- Precise Flight (Bend, OR) and Mountain High (Redmond, OR): strong positions in general aviation with differentiated pulse‑demand and portable offerings that appeal to fractional and business aviation buyers focused on weight and lifecycle cost.

- Meggitt / Parker Hannifin and Honeywell Aerospace: platforms focused on military OBOGS, specialized cylinders, and high‑altitude rotary/rotorcraft solutions — competitive for defense procurement and OEMs specifying integrated life‑support systems.

The competitive landscape section of the report contains capability matrices, supplier risk heatmaps, and a “fit for purpose” guide for selecting partners depending on fleet composition, regulatory exposure, and service strategy.

Operational playbook for 2026 — five immediate moves

Based on market sizing, concentration, regulatory dynamics, and technology trajectories, PW Consulting recommends the following priority actions for 2026:

- Map compliance timelines to cashflows: create a 24–36 month oxygen compliance calendar that aligns AD-driven replacement needs with maintenance shop capacity and capital expenditure windows.

- Lock MRO capacity via strategic partnerships or bolt‑on acquisitions: reducing dependence on third‑party windows for hydrostatic testing and PBE overhauls is a high‑leverage move.

- Pilot digital lifecycle trials: deploy smart cylinder tracking and predictive maintenance on a representative subset of aircraft to quantify OPEX benefits before fleetwide rollout.

- Design supply‑chain redundancy for critical components: cylinder suppliers, regulator electronics, and sealed mask assemblies each have distinct lead‑time risk profiles; diversify sourcing accordingly.

- Use procurement incentives to shift risk: structure supplier contracts to share certification and retrofit costs, and incorporate performance‑based payments tied to service availability or oxygen consumption reductions.

Where the full report adds operational value

The analysis above is intentionally selective. The complete PW Consulting Aviation Oxygen Systems Market report delivers the operational detail you need to convert insight into action, including:

- Full historical and forecast market tables (2020–2032) with scenario sensitivity and conversion factors by revenue unit and currency.

- Segment‑level demand drivers and unit economics by application and aircraft class (with interactive models to test fleet mixes without exposing proprietary splits here).

- Detailed supplier profiles, recent M&A timelines, and a proprietary supplier risk index.

- Certification and regulatory impact models tied to ADs and Part 91.211‑style requirements, with recommended compliance calendars for different operator archetypes.

- Actionable procurement templates, MRO partnership frameworks, and a prioritized list of product upgrades with estimated payback periods.

Final perspective — make 2026 the year compliance becomes a competitive advantage

Oxygen systems are often perceived as a compliance line item. Our research shows they can be a lever for operational resilience, cost control, and incremental revenue (through value‑added services). With a market expected to grow at roughly 6.8% CAGR through 2032 and a clear split of value between product and services, operators and suppliers who align certification strategy, digital lifecycle management, and supply‑chain resilience will convert regulatory pressure into differentiated operational performance.

To explore the granular datasets, supplier scores, and executable timelines that underpin these conclusions, request the full Aviation Oxygen Systems Market report. The report includes the interactive financial models and procurement playbooks that executives and investment committees need to justify 2026 capital and MRO commitments.

PW Consulting remains available for tailored workshops: fleet-level compliance mapping, supplier due diligence, and M&A target screening. Contact our aviation practice to schedule a briefing and to receive the full report and model access.

For detailed analysis of this topic, please visit the official page:Aviation Oxygen Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com