Ion Chromatography Column Market 2026 Strategic Outlook — A PW Consulting Intelligence Brief

Executive summary

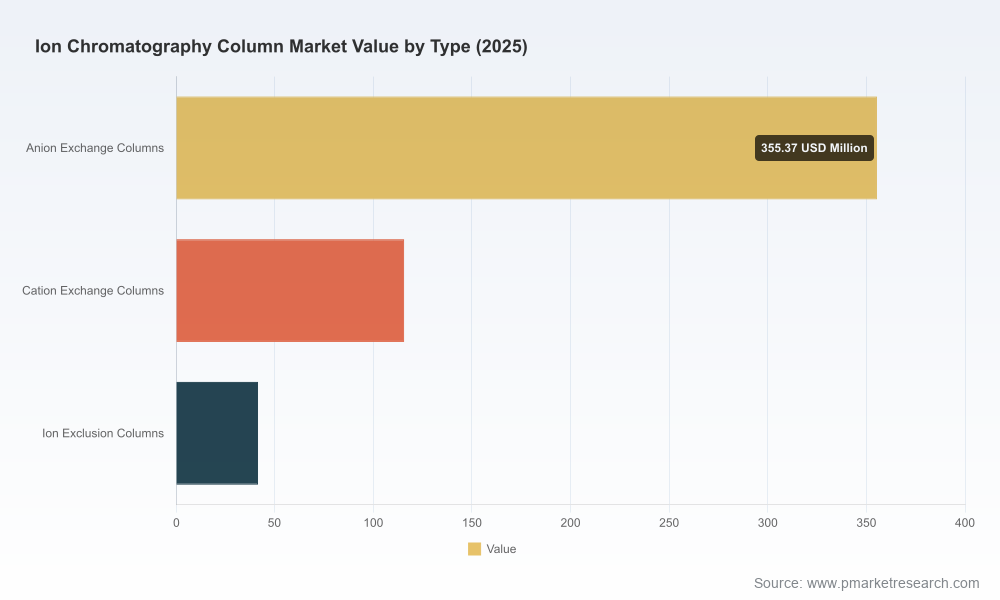

PW Consulting’s latest market study on the Ion Chromatography (IC) Column market equips executives with the fact base and strategic frameworks needed to make high-confidence decisions in 2026. The market expanded steadily through the first half of the decade — from an industry-wide baseline in 2020 to a global market size of approximately USD 512.5 Million in the report base year of 2025 — and our forecasting framework projects continued expansion through 2032. Under our central scenario the market grows at a compound annual growth rate (CAGR) of 7.24% across the 2026–2032 forecast window, reaching an expected market size by 2032 consistent with the continued adoption of IC in regulated testing, process control, and specialty analytics.

Ion Chromatography Column Market

Two structural features define the competitive environment: a materially concentrated supplier landscape (reported CR3 and CR5 metrics indicate a high share of market revenue controlled by the leading firms) and a persistent aftermarket opportunity driven by consumables, service and software. These twin characteristics shape both the near-term battlegrounds for share and the mid-term plays for margin expansion.

Ion Chromatography Column Market

Why this report matters to 2026 decision-makers

2026 will be a decision-heavy year for IC market participants: product roadmaps must align with accelerated regulatory adoption, go-to-market models need to capture recurring consumable revenue, and supply-chain resilience has become a board-level priority. Our report is designed not as an academic exercise but as a practical decision support tool. It translates market trajectories into executable options for three executive use cases:

Ion Chromatography Column Market

- Commercial leaders deciding where to allocate R&D and field sales resources

- Corporate development teams assessing bolt-on acquisition or partnership targets

- Operations executives balancing manufacturing scale investments with risk mitigation

For each use case we provide prioritized plays, estimated economic upside ranges derived from our bottom-up sizing, and sensitivity analyses tied to regulatory and technology contingencies.

Key market dynamics shaping strategy in 2026

- Regulatory and standards tailwinds — Recent compendial and environmental standard updates have increased the acceptability of IC for compendial assays and water analysis. Organizations that can demonstrate compliance with regulatory frameworks (including recognized EPA and pharmacopeial methods and 21 CFR Part 11–compatible software practices) are positioned to win a disproportionate share of regulated testing spend.

- Product innovation and platform bundling — Compact, automated platforms introduced by established instrument OEMs are shortening sales cycles for complete system solutions while creating new attachment points for column consumables and maintenance services.

- Concentration and aftermarket leverage — The market’s high CR3/CR5 indicators highlight two realities: scale matters for reagent and column manufacturing economics, and independent and OEM-affiliated aftermarket channels represent a meaningful, defensible source of recurring margin.

- Supply chain and manufacturing economics — Rapid scaling of polymer- and resin-based stationary phases and precision packing processes favors players with manufacturing depth or contract-manufacturing partnerships. Firms able to de-risk raw-material exposures and shorten lead times will capture share during demand surges.

Competitive landscape — who matters, and how they compete

The IC column ecosystem is anchored by global instrumentation and consumable leaders, regional specialists with deep regulatory relationships, and manufacturing-scale challengers. Our vendor analysis synthesizes public strategy signals, product portfolios, patent positions and go-to-market models to map where each firm competes on product breadth, regulatory trust, price, and aftermarket reach.

- Major OEMs with integrated platforms: Firms with a long-standing presence in chromatography offer broad column portfolios and integrated IC systems, leveraging installed base, brand trust, and cross-sell opportunities into pharmaceuticals and environmental testing.

- Specialist manufacturers and regional champions: Companies with deep expertise in ion-exchange media or targeted applications bring differentiated chemistries and local regulatory familiarity—critical for adoption in regulated environments.

- Manufacturing-focused challengers: High-volume producers focused on cost-competitive consumables and patentable process improvements are actively pursuing scale advantages and export growth.

Notable recent corporate actions underscore these dynamics. Early-2026 product introductions of compact, fully automated IC systems emphasize ease-of-use and workflow integration, accelerating adoption in water quality testing workflows. Catalog and product-line refreshes by several established column manufacturers reinforce ongoing investments in portfolio rationalization and aftermarket positioning. Collectively, these moves create short windows of opportunity for competitors to partner, differentiate, or seek consolidation.

What’s inside the report — practical deliverables

The report is organized to support immediate, actionable decision-making:

- Market sizing model (historical 2020–2025 and forecast 2026–2032) with scenario toggles that allow executives to model upside and downside regulatory outcomes and technology adoption curves.

- Market concentration and competitive intensity analysis (including CR3/CR5 metrics) and an assessment of the aftermarket revenue pools that underpin recurring margin.

- Vendor benchmarking across nine dimensions: product breadth, regulatory certifications, installed base strength, pricing strategy, manufacturing footprint, IP position, channel reach, digital capabilities and service proposition.

- Go-to-market playbooks tailored to three strategic archetypes: incumbent OEMs, contract manufacturers, and lean challengers—each with a prioritized 12–24 month action plan.

- M&A and partnership screening framework that produces a ranked shortlist of candidate targets by strategic fit, integration risk, and expected payback — presented without disclosing proprietary target metrics to preserve confidentiality.

- Supply-chain stress tests and mitigation levers, including dual-sourcing scenarios, inventory policy adjustments and nearshoring trade-offs.

- Price-to-win models and value-capture tactics for post-installation consumables and software subscriptions.

- Case studies and primary interviews with laboratory managers, procurement heads and R&D leaders to ground recommendations in customer economics and operational realities.

Strategic implications and recommended actions for 2026

We translate market dynamics into three priority strategic moves that executives should consider in 2026:

- Protect and expand recurring revenue: Prioritize initiatives that convert instrument sales into locked-in consumable and service streams — for example, bundled service contracts, subscription pricing for maintenance and remote diagnostics, and certified-equivalency programs that reduce customer switching.

- Invest selectively in automation and compatibility: The adoption of compact, automated IC platforms creates demand for plug-and-play columns and validated methods. Allocate R&D to develop validated column-solution packages for priority workflows and to ensure compatibility with leading instrument platforms.

- De-risk and industrialize supply: Evaluate contract manufacturing partners and consider capacity investments for critical stationary-phase chemistries. Implement dual-sourcing and localized inventory strategies for key geographies to prevent revenue leakage during supply disruptions.

For M&A-minded strategists, our analysis clarifies where scale buys market access versus where technology acquisitions buy differentiation. For nimble challengers, partnering with system OEMs on validated column packages offers a fast route to installed base access without the upfront instrument sales cost.

90-day tactical playbook (what to do first)

- Days 0–30: Run a revenue-at-risk assessment by product family using the report’s model. Map installed-base customers and identify top accounts for rapid consumable-capture programs.

- Days 30–60: Initiate regulatory-compliance audits for core product lines; prioritize obtaining endorsements or method validations that align with EPA/compendial requirements referenced by customers.

- Days 60–90: Launch two pilot initiatives — a bundled service subscription with one existing account and a compatibility validation program with a major instrument platform — and measure uptake, gross margin and churn impact.

Why PW Consulting — methodology and credibility

Our analysis combines a bottom-up market-sizing engine, primary interviews across the value chain, and proprietary benchmarking frameworks. We reconcile supplier public filings and product disclosures with a network of laboratory procurement and regulatory contacts to translate technical trends into commercial outcomes. The report provides both the quantitative models executives need to stress-test strategies and the qualitative playbooks required to act quickly.

Next steps

PW Consulting’s Ion Chromatography Column Market report is intentionally structured as a decision tool: it signals where value will be created over the next six years while withholding granular proprietary segmentation tables that we deliver to licensed clients. Executives ready to align their 2026 plans with empirically grounded scenarios can access the full intelligence package — including the interactive forecast model and vendor scorecards — through our report portal.

For strategy teams, corporate development groups, and operations leaders preparing 2026 budgets, this report converts market momentum into prioritized actions and measurable KPIs. Reach out to PW Consulting to commission a tailored workshop that translates our findings into a 12-month implementation roadmap for your organization.

For detailed analysis of this topic, please visit the official page:Ion Chromatography Column Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com