Iron tv Pro: A Simple Way to Enjoy Live TV and Entertainment

Other |

2026-06-05 12:56:43

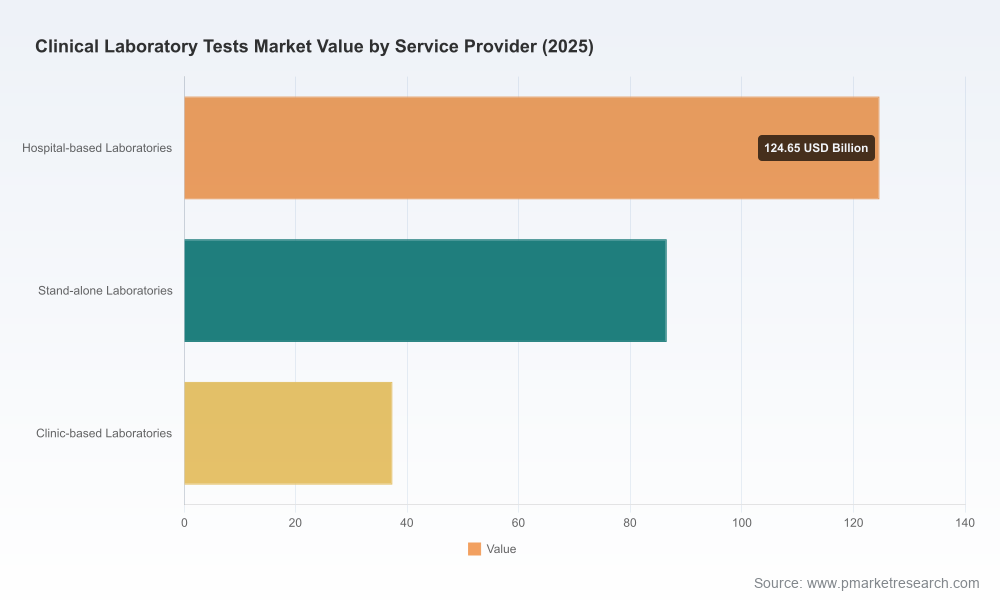

PW Consulting’s latest market intelligence brief — the Clinical Laboratory Tests Market report (base year 2025) — is designed as an operational playbook for executives, investors, and policy teams who must make durable 2026 decisions under regulatory and reimbursement flux. The global market reached approximately USD 248.5 Billion in 2025 and, on the trajectory we model, will exceed USD 377 Billion by 2032 at a 6.15% compound annual growth rate (CAGR). This release summarizes the report’s strategic value, highlights the most consequential dynamics shaping the sector in 2026, and outlines the practical actions our clients are already taking. In keeping with the “trailer” principle, we demonstrate analytical depth while intentionally withholding granular segment tables — the full dataset and interactive dashboards are available through our report portal.

Clinical Laboratory Tests Market

Regulatory reset and uncertainty: A pivotal U.S. judicial development and subsequent agency actions have altered the operating environment for laboratory-developed tests (LDTs). The reversion of the regulatory definition that was contested in 2024–2025 materially changes compliance risk profiles for many reference and hospital labs. Our scenario analyses show that labs dependent on LDT revenue need a near-term regulatory playbook to avoid sudden margin compression.

Clinical Laboratory Tests Market

Reimbursement re-pricing and coding churn: CMS updates for 2026 — including the introduction of new Proprietary Laboratory Analysis (PLA) codes and HCPCS/CLIA edits — create both revenue risk and arbitrage opportunities. New codes initially priced by Medicare Administrative Contractors (MACs) mean regional variance in realized pricing; organizations that operationalize targeted coding strategies will capture asymmetric value.

Clinical Laboratory Tests Market

Technology and product cadence accelerating adoption: 2025–2026 product introductions and automation platform upgrades are increasing throughput and enabling consolidation of test menus. Early adopters can deploy platform-driven cost-per-test reductions that change competitive positioning regionally and for specialty testing categories.

Validated market sizing and forecast model (2020–2032) with transparent assumptions and sensitivity runs. We provide a base-case projection consistent with the USD 248.5 Billion 2025 baseline and offer downside/upside scenarios tied to regulatory and reimbursement shocks.

Commercial opportunity maps for executives: where to invest in automation, which test portfolios to in-source versus partner/contract, and how to structure regional expansion to maximize realized reimbursement.

Regulatory risk matrix and compliance playbooks: step-by-step options for LDT governance, New York CLEP considerations, and device-submission routing — prioritized by impact and implementation complexity.

Reimbursement optimization toolkit: PLA code mapping, payer negotiation templates, and impact simulations for CMS pricing cycles through 2028.

M&A and partnership playbook: target profiles, integration checklists, and five-year synergies schedules, with worked examples for common deal archetypes in lab services.

Vendor and OEM engagement guide: procurement frameworks for instruments, test reagents, and lab automation that align capital expenditure to throughput and cost-per-test objectives.

Defend and rationalize margins through automation and test consolidation. Our cost models show that mid-size reference labs that invest in platform consolidation and end-to-end sample handling can materially reduce variable unit costs within 18–30 months of deployment.

Build a two-track portfolio strategy: protect cash-generating routine volumes while actively investing in high-growth specialty and molecular assays. Blood-based biomarkers, oncology panels, and select genetic services will continue to command higher value-per-test, but scale economics are essential to capture the margin premium.

Operationalize reimbursement intelligence as a competitive capability. With PLA codes initially MAC-priced, regional pricing variability will persist — organizations should combine payer contracting with targeted test routing to maximize realized revenue.

Prepare for regulatory contingency. Even where enforcement discretion remains, firms should treat LDT-related processes as if device regulation could apply in phases. That means establishing evidence generation pipelines, quality systems, and labeling governance that meet higher regulatory thresholds.

Pursue selective consolidation and partnerships. The market remains fragmented — concentration metrics indicate a low combined share among top firms, leaving space for regional champions, specialty players and cross-border consolidators to realize meaningful scale benefits. Strategic buyers who can combine geographic reach, platform compatibility, and payor relationships will create outsized value.

The market is shaped by a mix of large national reference laboratories, regional integrated networks, specialist centers of excellence, and diagnostic OEMs that supply instruments and reagents. Leading organizations are taking divergent but complementary paths:

Quest Diagnostics (Secaucus, NJ): A global diagnostic services leader that leverages breadth of test menus and national logistics to capture volume-driven advantages. Its sustained brand recognition and diversified customer base remain strategic assets.

Laboratory Corporation of America (Labcorp) (Burlington, NC): Labcorp’s rollout of blood-based biomarkers for neurodegenerative disease illustrates how test launches can create platform advantages in high-value clinical areas; continued investment in specialty assays is central to their growth play.

Sonic Healthcare (Sydney): Focused on integrated laboratory networks and quality pathology services across markets, Sonic’s playbook emphasizes localized clinical partnerships and diagnostic-plus-care models.

Eurofins (Luxembourg) & SYNLAB (Munich): Pan-regional players expanding specialty and genomic testing at scale, often through bolt-on acquisitions and capability aggregation to serve both clinical and commercial testing demand.

Academic and niche reference labs (ARUP, Mayo Clinic Laboratories): These institutions leverage clinical depth and esoteric test expertise to command referral flows and support complex diagnostics.

Specialty oncology and molecular players (NeoGenomics, BioReference/OPKO): Their focused portfolios and clinician relationships in oncology and genetics underpin differentiated revenue streams tied to precision medicine trends.

Diagnostics OEMs (Siemens Healthineers, Abbott): Instrument vendors remain strategic partners for high-volume labs; new automation and next-gen systems introduced in 2025–2026 materially affect throughput, consolidation potential, and service economics.

Recent industry events underscore these dynamics: large-scale product upgrades announced by major OEMs in late 2025 accelerate opportunities for labs to rationalize test menus and improve throughput; Labcorp’s national rollout of a blood biomarker for Alzheimer’s in 2025 demonstrates the speed at which newer assays can scale; and shifts in U.S. regulatory language for LDTs in 2025 have already changed risk calculus for many operators.

Private equity should prioritize targets with demonstrable scale levers — predictable payor mixes, opportunity for PLA-code capture, and scope for back-office consolidation. Our due diligence modules identify the 12 leading diligence triggers that most often determine deal value erosion for lab investments.

Strategic buyers should use our scenario-planning tool to stress-test portfolio choices against regulatory reconfirmations and CMS pricing cycles through 2028. Small differences in assumed reimbursement curves can change projected returns by double-digit percentages.

Hospital systems and health networks must assess which services to retain in-house vs. outsource to reference partners. We provide an operational decision matrix that ties clinical risk, turnaround-time requirements, and margin economics to vendor selection.

The report combines bottom-up test-volume analysis with top-down revenue triangulation, payer-adjudicated pricing datasets, interviews with lab executives and OEM procurement leads, and regulatory scenario modeling. We publish full transparency on assumptions and provide an interactive model enabling users to run custom scenarios. In keeping with our “trailer” approach for this announcement, we have deliberately excluded granular tables and percentage splits by region, test type, and provider channel from this summary in order to encourage direct access to the full report and interactive datasets available on our portal.

For 2026 planning, the principal strategic priority is to translate the macro growth tailwinds (a forecast CAGR of 6.15% through 2032) into defensible, operationally executable initiatives that protect margin and create scale in specialty services. The combination of coding volatility, regulatory redefinition, and rapid instrument refresh cycles means that tactical choices made this year — about platform investments, coding governance, M&A targets, and clinical focus areas — will determine competitive positioning for the next decade.

PW Consulting’s Clinical Laboratory Tests Market report is crafted to move executives from awareness to action: detailed scenarios, executable playbooks, and valuation-grade models built for 2026 decision-making. To access the complete report, data tables, and the interactive model, please visit the PW Consulting market research portal.

For detailed analysis of this topic, please visit the official page:Clinical Laboratory Tests Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com