Vail Limousine Services | Luxury Travel in Vail

Other |

2026-06-27 18:21:47

PW Consulting today publishes an executive summary of our new Smart Wireless POS Terminal Device Market report, a decision-ready intelligence product built to inform C-suite strategy, product roadmaps, and commercial execution through 2032. Our analysis traces a robust multi-year rebound and acceleration in wireless POS adoption: from a global market base of roughly USD 4.5 billion in 2020 to an estimated USD 7.43 billion in 2025, and a projected expansion at a 9.25% compound annual growth rate across the 2026–2032 forecast window, reaching an estimated USD 13.80 billion by 2032. These macro trends set the economic context for capital allocation, channel strategy and product development choices that organizations must make in 2026.

Smart Wireless Pos Terminal Device Market

Capital allocation under constrained budgets — deciding which hardware classes and deployment footprints will deliver the fastest payback and the longest product lifecycle.

Smart Wireless Pos Terminal Device Market

Platform vs. commodity trade-offs — evaluating whether to pursue vertically integrated, Android-based SmartPOS platforms or lighter mPOS and accessory-led models that emphasize speed-to-market.

Smart Wireless Pos Terminal Device Market

Regulatory and security compliance timing — aligning procurement and certification schedules (e.g., next-generation PCI PTS requirements) with product launches to avoid time-to-revenue delays.

Channel and partnerships — determining white‑label opportunities, distributor plays and systems integrator partnerships in an increasingly concentrated vendor landscape.

The report is designed as a hands-on toolkit for leadership teams. Highlights include:

Market sizing and high-confidence forecasting through 2032, with scenario sensitivity to connectivity disruptions, chip shortages, and regulation-driven refresh cycles.

Decision frameworks: procurement scorecards, total cost of ownership (TCO) models, and ROI calculators tailored to different deployment profiles (fixed retail, handheld/hospitality, mobile field services).

Vendor evaluation matrices and vendor playbooks that translate capability gaps into competitive actions — from pricing strategies to partner incentive designs.

Integration blueprints and implementation checklists for payment rails, POS‑to‑ERP synchronization, and omnichannel reconciliation to reduce time-to-straight-through processing.

Regulatory compliance and certification roadmaps — practical steps to satisfy PCI PTS 7.x, EMV and NFC requirements in major markets, and mitigation plans for certification-dependent go-to-market risks.

Go-to-market playbooks for software providers and OEMs, including verticalization strategies for hospitality and restaurant use cases, sample pricing models, and pilot-to-scale conversion plans.

M&A and partnership scenarios — valuation levers, capex vs. opex considerations, and post‑deal integration checklists focused on hardware/software synergies.

The market presents a moderate level of concentration. The three largest incumbent groups collectively account for a meaningful share of global revenue, while the top five increase that footprint substantially — an environment that favors scale for channel reach, certification budgets and supply chain resilience. This concentration has two practical implications for 2026 planning:

Large vendors can amortize certification and R&D costs across broader portfolios, putting pressure on smaller vendors to specialize or partner for niche verticals.

Distributors and integrators will leverage preferred-supplier programs; gaining or defending trade position requires demonstrable differentiation in services, security, or economics.

Our vendor analysis synthesizes primary interviews, product dissections and channel checks. The following themes frame competitor positioning and near-term strategic intent:

Ingenico (Paris) — continues to anchor the high-end portable device segment with hardened wireless devices that emphasize multi-network connectivity (Wi‑Fi, Bluetooth, cellular) and field-service reliability. Their focus on secure mobile payment appliances positions them well in enterprise retail and service deployments.

Verifone (San Jose) — remains a leader in enterprise-grade terminals, pairing legacy reach with product modernization. Their strategy balances retrofit replacements for installed bases with newer form factors geared to contactless and mobile commerce.

PAX Technology (Shenzhen / North America HQ in Jacksonville) — is notable for aggressive Android SmartPOS innovation and channel expansion. Their product footprint and showfloor activity (including recent restaurant-focused showcases) emphasize vertical-tailored hardware combined with third-party app ecosystems.

Newland Payment Technology (Fuzhou) — competes on certification breadth and cost efficiency, positioning its Android-based devices for cross-border deployments where global compliance is required.

Castles Technology and NEXGO (Taipei & Shenzhen) — both emphasize compact, resilient devices with EMV/NFC and IP-rated designs for mobile and mPOS use-cases, pushing into SME and mobile-first segments.

Worldline (Bezons) — is executing a platform play, rolling out Android SmartPOS devices integrated with business apps for European SMEs; their recent product introductions underline a shift to value-added services bundled with terminals.

Square (Block), Toast and NCR Voyix (US-based) — represent divergent strategies: software-led hardware (Square, Toast) versus integrated enterprise systems (NCR Voyix). Each brings differentiated GTM approaches for hospitality and small business segments.

Notable recent moves include regional Android SmartPOS launches and product refreshes that underscore two concurrent market dynamics: (1) the steady migration to Android-based platforms that support third-party app ecosystems, and (2) incremental product launches that aim to satisfy new certification baselines such as PCI PTS 7.x.

Security certifications: PCI PTS 7.x and equivalent standards are now a gating factor for global deployments; procurement teams must budget for certification timelines and device revalidation.

Contactless and EMV/NFC ubiquity: Compliance with EMV and NFC standards is a baseline expectation in major markets; Android SmartPOS platforms are increasingly the vector for rapid feature delivery.

Platformization: Android-based SmartPOS devices accounted for a meaningful share of global POS shipments as of 2023, and their role in enabling app ecosystems is accelerating monetization opportunities for ISVs and payment service providers.

For CEOs: Reassess portfolio exposure to hardware-margin pressure versus software services. Prioritize partnerships that guarantee supply continuity and certification bandwidth.

For CFOs: Adopt a lifecycle cost metric that captures certification, security updates and end-of-support migration costs; favor procurement terms that convert sizeable capital outlays into flexible opex options where possible.

For CTOs and Product Heads: Standardize on secure, modular architectures that support over‑the‑air updates and third‑party app ecosystems. Build integration staircases to major POS middleware and payment gateways.

For Heads of Sales & Channels: Reconfigure incentives to support bundled solutions (hardware+software+services). Target vertical pilots that can scale quickly—restaurant and hospitality pilots remain high-value proving grounds.

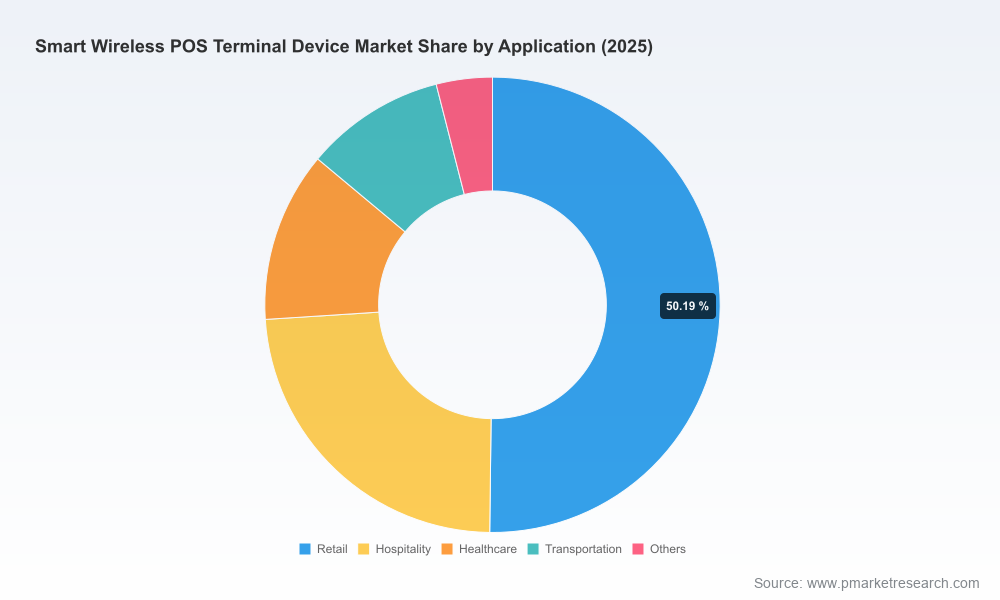

In keeping with our “prequel” approach, this release highlights strategic insights and actionable frameworks while withholding the granular regional and application breakdowns that buyers use for execution (e.g., precise regional revenue splits, fine-grained application share by country, and vendor-specific market share by segment). These core segmentation layers are available exclusively in the full PW Consulting report, together with downloadable TCO models, vendor scorecards and primary‑source interview transcripts that underpin our findings.

Download the complete report to access: (1) the full segmentation model and interactive regional dashboards used to stress-test your market entry assumptions; (2) vendor scorecards with validated product specs and certification status; (3) executable playbooks and procurement templates ready for board approval. The full package is designed to convert insight into executable projects within 60–120 days.

For executive briefings, tailored scenario modeling, or to license the full report and associated tools, PW Consulting offers private advisory sessions and industry workshops designed to accelerate time-to-decision. In a market expanding at a mid‑single-digit to low‑double‑digit pace, the difference between leading and lagging organizations will be determined by how quickly they translate certification-aware product roadmaps into channel-ready offers.

For detailed analysis of this topic, please visit the official page:Smart Wireless Pos Terminal Device Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com