Riveting Tools Market: Size, Share, and Future Growth

Other |

2026-05-07 03:41:23

PW Consulting today releases a strategic briefing accompanying our full Chromatography Cartridges Market research report (base year 2025, historical 2020–2025, forecast 2026–2032). Our analysis shows a market that reached approximately USD 925.0 million in 2025 and is expected to expand at a compound annual growth rate (CAGR) of roughly 7.85% through the 2026–2032 forecast window, approaching an estimated USD 1.57 billion by 2032. This briefing highlights the most consequential trends and decision levers for corporate leaders in 2026, while deliberately withholding proprietary segment-level breakdowns to preserve the value of the full report and guide you to the source for the detailed intelligence required for transaction, product, and go‑to‑market decisions.

Chromatography Cartridges Market

Strategic exposure to biotherapeutics and large-molecule processing: Rising demand for monoclonal antibodies, vaccines, gene therapies and other biologics is reshaping cartridge requirements — from affinity media to process-scale monoliths — creating differentiated margin pools for suppliers who can meet GMP and traceability expectations.

Chromatography Cartridges Market

Analytical rigor across sectors: Regulatory tightening in food safety, environmental monitoring, and pharma analytics continues to push labs toward higher-performance, reproducible cartridge solutions that support robust method transfer and QA documentation.

Chromatography Cartridges Market

Product modularity and single-use economics: Prefilled cartridges, cartridge-based purification for discovery-to-preparative scales, and disposable formats are accelerating adoption in contract research, academic, and industrial workflows seeking speed and lower cross-contamination risk.

Material and technical differentiation: Silica-based stationary phases—especially spherical silica—remain the workhorse for many applications. At the same time, inert and specialty phases designed for metal-sensitive or high-purity biotherapeutic workflows are gaining traction, as evidenced by recent product launches across the supplier base.

Macro-growth is robust and broad-based, driven by converging forces: higher throughput needs in pharmaceutical development and QC, increased regulatory scrutiny across non-pharma testing segments, and technology enhancements that enable cartridge formats to migrate from analytical to preparative and process scales. The reported CAGR of about 7.85% reflects both volume growth and continuing product premiumization — customers are willing to pay for performance, traceability, and reduced lifecycle cost.

Market structure remains moderately concentrated. The top three companies account for a meaningful share of the market, while the top five deepen that concentration — leaving mid‑market and specialty vendors room to capture niche, high-value segments. This concentration profile creates a two-track competitive landscape: incumbents defending broad, integrated portfolios and agile specialists exploiting technical differentiation or custom manufacturing relationships.

Supply-chain and input risks deserve attention. Silica continues to dominate as the stationary phase material, and variations in quality, particle morphology, and supplier capacity materially affect downstream reproducibility and pricing. Procurement strategies that secure quality-assured silica supplies, coupled with dual-sourcing and supplier development programs, are practical hedges against volatility.

BUCHI Labortechnik — Strong in prefilled flash cartridges across silica and bonded phases; appeals to purification workflows that prioritize loading capacity and backpressure optimization.

Biotage — Offers prepacked options across normal and reversed phase chemistries; well-positioned in drug discovery and research scales where cartridge consistency and known chemistry platforms are critical.

Restek Corporation — Focused on guard cartridges and inert HPLC protection; recent launches underscore capabilities for handling metal‑sensitive compounds and improving column longevity.

Sartorius AG — Orients toward process-scale cartridges and monolithic formats for bioprocessing, targeting large-molecule purification needs in GMP environments.

Agilent Technologies — Expands high-performance inert column offerings for biotherapeutics and oligonucleotide work; signals a push to capture higher-margin analytical and biopharma segments.

Waters Corporation — Focused on protein and affinity solutions with advanced column technologies for biopharma analytics and purification.

Thermo Fisher Scientific — Leverages a comprehensive disposables portfolio spanning analytical to preparative applications; valuable for customers seeking one‑stop procurement.

Orochem Technologies — Competes on flash and HPLC consumables with a mix of analytical and industrial-scale offerings; attractive for price-sensitive or custom-volume customers.

Recent product introductions demonstrate two near-term inflections: (1) an acceleration in inert-phase cartridges and guard products to address metal‑sensitive chemistries, and (2) targeted HPLC/flash releases optimized for biotherapeutic workflows. These moves validate supplier strategies oriented around specialized chemistries and application-driven product design.

Historical and forecast market sizing (2020–2032) with scenario modeling and sensitivity analysis around pricing, raw material costs, and CAPEX for scale-up.

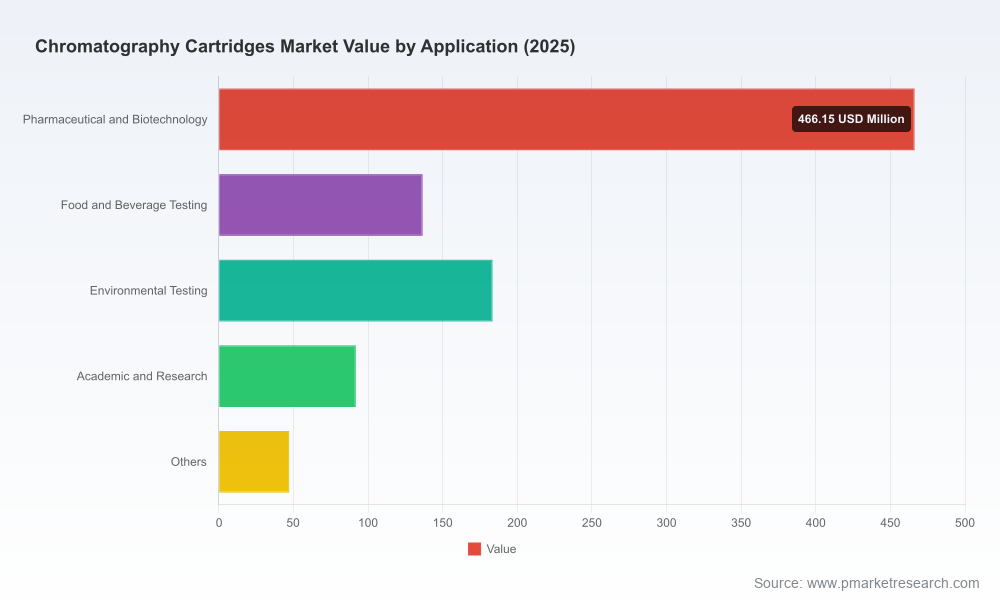

Segment-level diagnostics by type, application and region — including growth vectors and TAM estimates (note: detailed segment splits are intentionally omitted from this brief; full data available in the report).

Price and margin benchmarking across cartridge types and manufacturing scales, plus a unit-cost build-up model for silica-based and specialty phases.

Supplier maturity and capability maps, vendor scorecards, and go-to-market archetypes to support partner selection or acquisition screening.

Regulatory and quality playbook for GMP adoption in process-scale cartridges: traceability workflows, documentation templates, and inspection readiness checklists.

Supply-chain stress test toolkit: dual-sourcing scenarios, inventory sizing guidance, and contingency playbooks for silica or key consumable shortages.

Commercial playbooks — product positioning, channel strategies, and sample-led account penetration plans tailored to pharma, CROs, food & environmental labs, and academic customers.

Prioritize biopharma-compatible formats: Accelerate development or licensing of cartridges designed for large-molecule purification and affinity capture. Invest in validation packages and GMP-ready documentation to shorten customer adoption cycles.

Differentiate on chemistry and inertness: Develop or acquire inert-phase and metal-tolerant chemistries to capture rising demand in metal-sensitive compound analysis and biotherapeutic assays.

Secure critical inputs: Implement supplier development programs for high-quality silica and establish dual-source agreements with performance-based SLAs to mitigate supply risk and protect gross margins.

Monetize convenience: Expand prefilled and single-use cartridge offerings with tiered pricing and service bundles (technical support, method transfer) to increase wallet share.

Optimize route-to-market: Tailor channel strategies for CROs, CMOs, academic accounts, and in-house pharma labs — balancing direct sales, distributors, and e-commerce for maximum coverage and cost-efficiency.

Use M&A selectively: Pursue tuck-ins that provide unique chemistries, manufacturing scale for cartridges, or GMP-compliant process cartridges to accelerate entry into process-scale bioprocessing segments.

Embed regulatory excellence: Make compliance and traceability a marketable capability; customers increasingly shortlist vendors on GMP readiness and QA transparency.

Invest in data and services: Offer analytical method libraries, digital lot-tracking, and application support as differentiators that deepen customer stickiness and justify premium pricing.

Our full Chromatography Cartridges Market report contains the granular data, financial models, and executable playbooks necessary to operationalize the recommendations above. The published brief is intentionally a “trailer”: it highlights the trends and strategic choices without disclosing the proprietary segmentation and pricing matrices that underpin investment decisions. For executive teams evaluating product roadmaps, partnership strategies, or acquisition targets in 2026, we offer tailored deliverables including bespoke TAM decompositions, competitor impact simulations, and M&A target screening using our proprietary scoring framework.

To obtain the full dataset, receive a custom briefing, or commission scenario-based models aligned to your corporate objectives, contact PW Consulting. Our analysts will provide a confidential walkthrough of the report, an extract of the Excel workbook, and a prioritized action plan calibrated to your risk appetite and time horizon.

For detailed analysis of this topic, please visit the official page:Chromatography Cartridges Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com