Revealed: The Aluminium-Ion Battery Market is on the Verge of Transformation

Other |

2026-06-29 09:52:19

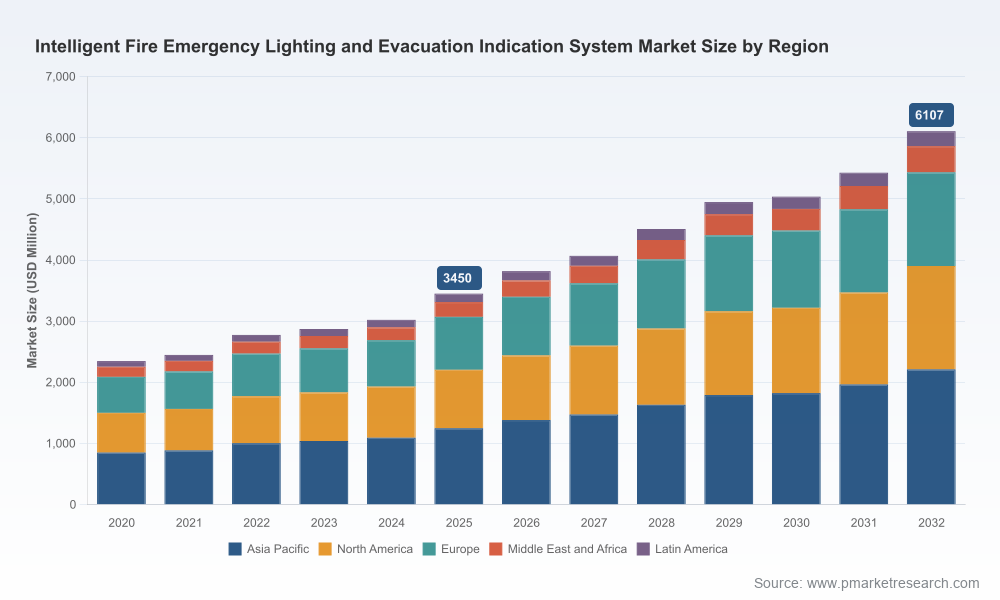

As governments, building owners, and system integrators navigate an accelerating wave of regulatory change and smart-building transformation, the Intelligent Fire Emergency Lighting and Evacuation Indication System market is entering a decisive phase. PW Consulting’s latest market study—anchored on a 2025 base year and forecasting through 2032—finds the global market at roughly USD 3.45 billion in 2025 and growing at a compound annual growth rate (CAGR) of approximately 8.5% through the 2026–2032 forecast window, reaching an estimated mid-single digit billions by 2032. For C-suite leaders and procurement heads preparing capital and product plans in 2026, this report is designed as a tactical briefing: it synthesizes regulatory inflection points, supplier dynamics, and technology trajectories into actionable options while deliberately reserving proprietary segmentation tables and company-level scorecards for the full report.

Intelligent Fire Emergency Lighting And Evacuation Indication System Market

Regulatory deadlines are compressing procurement windows. New national and regional standards released in 2024–2025 introduce functional requirements (adaptive lighting, personnel positioning, Bluetooth elements, stricter self-test and documentation regimes) that will materially affect system specifications, testing regimes, and certification timelines.

Intelligent Fire Emergency Lighting And Evacuation Indication System Market

System interoperability and lifecycle economics are becoming primary procurement criteria. Buyers now evaluate emergency lighting not as a discrete product but as a node in an integrated life-safety and building-management ecosystem.

Intelligent Fire Emergency Lighting And Evacuation Indication System Market

Market growth is robust but not hyper-consolidated. Competitive dynamics leave room for both global platforms and focused regional specialists to expand—making 2026 a window for strategic partnerships, targeted M&A, and product differentiation investments.

Three interlocking forces are driving the market’s steady expansion. First, regulatory modernization in core markets is redefining minimum capabilities and compliance checklists. Standards such as the updates to Europe’s luminous requirements and the revised national certification frameworks in large markets are increasing baseline product complexity and testing obligations. Second, the march of digital building infrastructure—IoT sensors, addressable fire panels, and cloud analytics—has turned emergency lighting into a source of operational data (status of luminaires, battery health, occupant flow indicators) that feeds safety analytics and facilities management workflows. Third, technology diffusion (LED efficiency improvements, networked emergency luminaires, adaptive escape lighting algorithms, and person-tracking aids) is enabling higher-value feature sets that buyers are willing to pay for, especially in critical public infrastructure and high-rise commercial portfolios.

Operationally, this combination means procurement teams must weigh not only unit costs but software lifecycle, cybersecurity posture, certification roadmaps, and service models (from central battery maintenance to automated test reporting). PW Consulting’s fieldwork indicates that, for many large asset owners, the total cost of ownership (TCO) advantage of intelligent systems—through reduced manual testing, predictive maintenance, and fewer false alarms—can become a decisive win once integration and rollout risks are managed.

New national certification revisions now require embedded self-test functionality, expanded scope definitions for distribution equipment, and explicit support for wireless augmentation (e.g., Bluetooth for positioning) in certain jurisdictions. These changes create near-term certification backlogs and conversion requirements that vendors and suppliers must plan around.

European updates to luminous requirements and the inclusion of adaptive escape lighting in public/workplace contexts will force specification changes for projects with cross-border compliance exposure.

Revisions to national guidance on risk assessment and documentation (including prescriptive periodic measurement intervals) raise the bar for project handover deliverables and maintenance contracting.

The competitive field comprises global platform providers, multinational electrical groups, specialist signage and adaptive-escape vendors, and regionally strong manufacturers. Leading multinational technology and industrial players—such as Siemens, Honeywell, and Eaton—leverage entrenched installed bases in fire alarm and building management systems to market integrated emergency lighting solutions that emphasize reliability and systems-level interoperability. Specialist firms—examples include Evaclite and Advanced—differentiate on adaptive exit signage, addressable test automation, and compliance with stringent regional standards.

Strong regional players from Asia offer competitive product-cost profiles and rapid certification turnaround. Several Chinese manufacturers and suppliers have expanded export footprints while also serving large domestic retrofit programs. Across supplier types, capability gaps separate those who can deliver full software-enabled lifecycle services (remote monitoring, predictive maintenance analytics, integrated testing records) from those who remain focused on hardware-first offerings.

Market concentration metrics indicate a moderate level of supplier consolidation at the top (a relatively small share captured by the three largest firms, and a modestly larger share by the top five). In practice, this concentration level is consistent with a market where platform integration and certification expertise provide advantages, yet niche innovation and local certification agility can still win meaningful contracts.

Buyers (owners, integrators, FM companies): Re-frame procurement around lifecycle outcomes rather than unit costs. Require demonstrable end-to-end integration testing, software-update SLAs, and clear document trails for risk assessments and five-year illuminance verification plans where applicable.

System suppliers: Prioritize modular architectures and open-API strategies that reduce integration friction with leading fire panels and building management systems. Invest in certification roadmaps aligned to key markets and publish transparent migration plans for customers to convert older equipment.

Product managers: Differentiate through software-enabled maintenance savings—automated testing and battery health analytics provide quick ROI narratives for building owners under tighter compliance regimes.

Investors and M&A teams: Look for targets that combine a strong regional certification footprint with software-enabled services. Companies that can turn compliance complexity into a recurring-service advantage will command premium valuations.

Consulting and integrator partners: Offer standardized assessment packages (baseline compliance gap analysis, 100-day remediation plan, and 3-year upgrade roadmap) to accelerate project pipelines during the regulation transition window.

The report is structured to support decision-making from strategic board debates to operational procurement. Key deliverables include:

A transparent market-sizing and forecasting model with scenario outputs across vendor strategies for 2026–2032.

An interactive regulatory impact matrix that maps new and forthcoming standards to product features, test regimes, and certification timelines.

Supplier profiles and comparative capability assessments covering technical stack, certification reach, service models, and pricing archetypes—crafted from primary interviews and product bench-testing.

Actionable procurement templates (RFP language, evaluation scorecards, service-level clauses) and a step-by-step implementation playbook for retrofit and greenfield projects.

Risk and scenario planning tools—covering supply-chain disruptions, certification delays, and cybersecurity events—with contingency playbooks and estimated financial exposures.

Case studies and ROI calculators illustrating TCO outcomes for commercial, industrial, and critical infrastructure deployments.

To preserve the strategic value of our primary research, detailed segmentation tables and the proprietary company scoring matrices are available exclusively in the full report—this press release provides a synthesis and contextual roadmap rather than the raw segmentation figures.

90 days: Complete a compliance gap assessment against the latest national and regional standards; prioritize critical assets where adaptive lighting or personnel positioning are required.

180 days: Issue supplier RFIs focused on certification timelines, software upgrade policies, and TCO scenarios; secure supply or conversion slots if a vendor’s certification capacity is constrained.

365 days: Implement pilot integrations with one or two preferred vendors, focusing on data capture, automated test reporting, and maintenance workflow integration to validate anticipated OPEX savings.

For executives and procurement leaders preparing strategy in 2026, the decision horizon is defined by regulatory compliance timing, integration capability, and the ability to convert product features into sustained service value. PW Consulting’s market forecast and pragmatic toolset are designed to shorten timelines from decision to deployment, minimize certification risk, and sharpen vendor selection through evidence-based evaluation. The market opportunity is clear: steady growth driven by regulation and digitalization opens concrete paths to value capture, but success hinges on a disciplined approach to standards alignment, interoperable architectures, and service-led monetization.

For organizations that want the full dataset, segmentation detail, and supplier scorecards to execute board-level decisions and procurement actions, PW Consulting’s full Intelligent Fire Emergency Lighting and Evacuation Indication System Market report is available on our research portal. The full deliverable includes the proprietary models, appendices of primary interviews, and downloadable procurement templates referenced above.

For detailed analysis of this topic, please visit the official page:Intelligent Fire Emergency Lighting And Evacuation Indication System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com