Global Luxury Niche Perfume Market Growing at 9.1% CAGR Through 2032

Other |

2026-06-30 13:34:24

PW Consulting's latest market study on Aerial Target Drones delivers a focused, decision-grade briefing for defense planners, program managers, and industrial strategists preparing procurement, production, and partnership choices in 2026. Built on a base year of 2025 and a seven-year forecast horizon through 2032, the report synthesizes commercial, programmatic and policy dynamics that will determine who wins and who lags in the rapidly evolving target drone ecosystem.

Aerial Target Drones Market

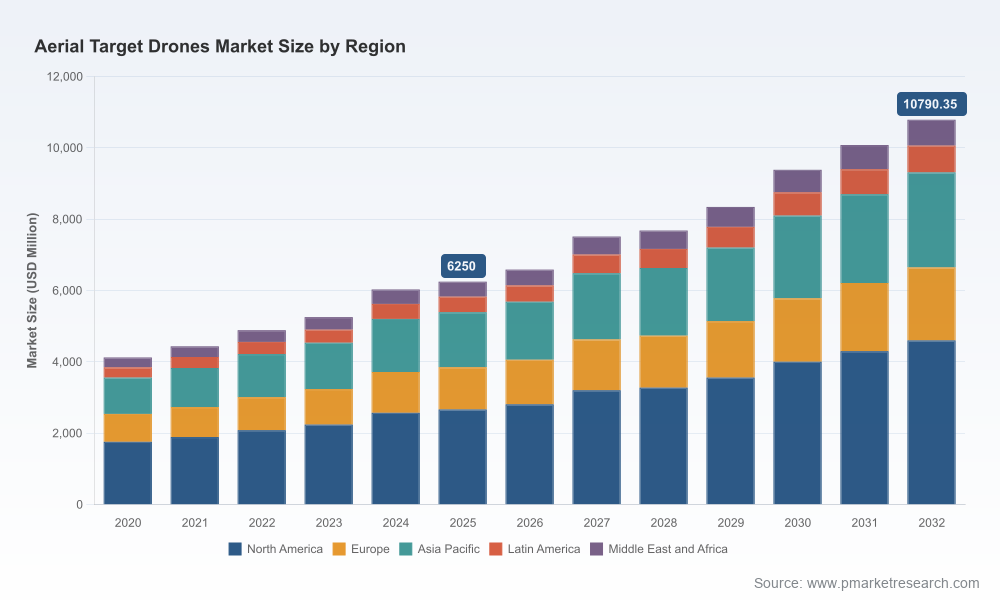

The aerial target drone market is at an inflection point. After steady growth in the first half of the decade, the market reached approximately USD 6.25 billion in 2025 and — under a baseline projected compound annual growth rate of 8.12% — is expected to expand meaningfully through the next phase of capability refresh cycles, live-fire training demand, and weapons testing programs. For defense buyers and industrial participants, 2026 is the year to convert strategy into procurement postures, supply‑chain decisions, and partnering choices that will shape mid-decade readiness and cost trajectories.

Aerial Target Drones Market

Growth drivers: Persistent investment in realistic training and lethality testing, scaled interest in low-cost, high-fidelity threat representation, and programs to convert legacy platforms into full-scale targets are sustaining demand. Markets that are maturing toward lifecycle sustainment and recurring production will reward firms that combine robust platform design with scalable production processes.

Aerial Target Drones Market

Forecast view: The report maps a continuous expansion from the mid‑decade baseline, with overall market size rising substantially by the end of the forecast window. That expansion is not uniform — it will be shaped by procurement phasing, sovereign sourcing mandates, and the pace of adoption of hybrid and expendable solutions.

Timing is critical: Acquisition timelines for training fleets and full-rate production decisions being made in 2026 will determine supplier backlogs and industrial capacity utilization during the following 24–36 months.

Our competitive assessment identifies a set of incumbent and diversified primes that anchor capability corridors across expendable subscale targets, high-performance jet targets, and full-scale conversions. Market leadership today reflects a combination of specialized platforms, program-primary supplier relationships, and geographic footprints aligned with major customer bases.

Kratos Defense & Security Solutions — A market leader in high-performance and subscale aerial target systems, Kratos supplies a range of expendable and reusable platforms used across naval and air force live-fire programs. Recent production awards and international collaboration activity underscore its role as a prime integrator for threat-representation missions.

QinetiQ — With a family of uncrewed aerial targets optimized for realistic threat emulation, QinetiQ maintains long-term service relationships with multiple navies and allies. Its follow-on support arrangements demonstrate the value of deep sustainment and training-service offerings in locking in recurring revenue.

Griffon Aerospace — Focused on subscale systems commonly used in air-defense and sensor-testing regimes, Griffon is notable for platform durability, production scalability, and service-provisioning to domestic customers.

Boeing — Boeing’s conversion of legacy fighter aircraft into full-scale aerial targets provides a unique, high-fidelity option for certain types of weapons testing and end-to-end training. That capability serves specific mission profiles where realistic signatures and flight envelopes are required.

AeroTargets International (ATI) and Air Affairs Australia (QinetiQ) — Both firms supply targeted point solutions for air-defense training, counter‑UAS trials, and RDT&E missions, emphasizing modular payload integration and mission tailoring.

Northrop Grumman and Lockheed Martin — These large primes participate through systems integration, program-level offerings, and by providing sustainment and engineering depth to nation-scale training programs.

Collectively, leading vendors exhibit a mix of proprietary platforms, sole-source program relationships, and regional service footprints. That mix favours firms that can couple platform performance with secure supply chains, long-term sustainment, and tailored training services.

Program awards and follow-on sole-source support contracts indicate customers prefer to consolidate training fleets around proven suppliers that can deliver test-firing reliability and sustainment predictability.

Full-rate production awards for key jet-target platforms and conversion programs for legacy fighters into full-scale targets confirm a two-track demand model: high-fidelity, higher-cost full-scale targets coexist with scalable, expendable subscale fleets. Procurement portfolios that balance both tracks deliver resiliency for different training and testing missions.

International collaborations and co-development activity signal a push toward localized production, transfer of sustainment responsibilities, and partnering arrangements that reduce program risk for sovereign customers.

Two non-market forces are materially shifting strategy:

Export and sourcing policy. New export-control clarifications and domestic-sourcing mandates introduced in recent policy cycles change where and how target drone systems can be procured and sustained. That dynamic increases the value of suppliers with local production footprints or validated supply chains that meet sovereign requirements.

Critical input chokepoints. Dependencies in rare-earth magnets, lithium-ion energy storage, and advanced semiconductors create upstream risk that can constrain production ramp rates. The market is responding with investment in alternative suppliers, inventory strategies, and component certification regimes to reduce exposure to single-country dependencies.

Our full study is organized to convert intelligence into action. Key deliverables include:

Scenario-based market forecasts calibrated to procurement cycles and contingency demand; stress-tested cases for high/low spending environments.

Supplier scorecards covering technical readiness, production capacity, sustainment performance, exportability, and program-risk indicators — designed for rapid integration into RFx evaluation frameworks.

Supply‑chain vulnerability maps with mitigation playbooks: alternative sourcing pathways, nearshoring options, and inventory buffers keyed to critical BOM items.

Program cost models and lifecycle Total Cost of Ownership (TCO) templates that let acquisition teams compare full-scale conversions versus subscale fleet strategies across training, testing, and target/recover missions.

Operational playbooks for training range modernization: sorties-per-dollar metrics, signature management and telemetry recommendations, and runway/airspace integration checklists for range operators.

Deal structuring guidance and M&A target screening criteria for industrial players seeking capability or capacity expansion, including integration timelines and likely valuation multipliers for platform and sustainment assets.

Regulatory impact scenarios illustrating how recent export-rule clarifications and sovereign-sourcing provisions could alter supplier eligibility, procurement timelines, and lifecycle costs for allies and partners.

Acquirers: Use supplier scorecards and TCO templates to validate incumbent proposals and to structure performance‑based contracts that align supplier incentives with sortie availability and signature fidelity objectives.

Industry: Prioritize investments in component supply alternative sourcing and manufacturing scalability. Consider partnerships or JV models to secure market access where sovereign sourcing is decisive.

Program offices: Build procurement timelines that account for certification cycles and critical component lead times highlighted in our supply‑chain maps — earlier contract awards for long‑lead items will materially reduce schedule risk.

Investors and M&A teams: Use the report’s scenario outputs and target-screen frameworks to identify acquisition candidates that will gain value from near‑term recapitalization or capability integration.

Our approach blends program-level sourcing reality with market forecasting and operational tooling. Rather than produce only high-level curves, the study provides procurement-ready templates, risk mitigations, and a competitive map tied to likely procurement outcomes. The result is an actionable intelligence package that reduces decision latency and improves negotiation posture — while preserving the confidentiality controls defense customers require.

This briefing intentionally highlights strategic implications and our methodological rigor without publishing the full segmentation matrices, regional splits, and application-level revenue breakdowns that clients use to execute bid/no‑bid and industrial investment decisions. To review the complete dataset, supplier benchmarking tables, and the downloadable decision-tool kit, please visit our report landing page or contact PW Consulting’s defense practice. The full report contains the granular intelligence and reproducible models required to move from strategy to contract award with confidence.

For program teams preparing 2026 procurement packages, and for suppliers positioning for capture and scale, the window to act is now. PW Consulting’s Aerial Target Drones Market study is designed to be the last market study you need before locking procurement strategy — proving the hypotheses you bring to negotiations and revealing the risk-reward tradeoffs you cannot see from public reporting alone.

Contact PW Consulting for an executive briefing, sample data extracts, or a tailored workshop to map the report’s insights directly onto your procurement roadmap or business-growth plan.

For detailed analysis of this topic, please visit the official page:Aerial Target Drones Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com