Duchenne Muscular Dystrophy Treatment Market Size, Share, Trends, and Industry Forecast by 2030

Other |

2026-06-04 07:57:31

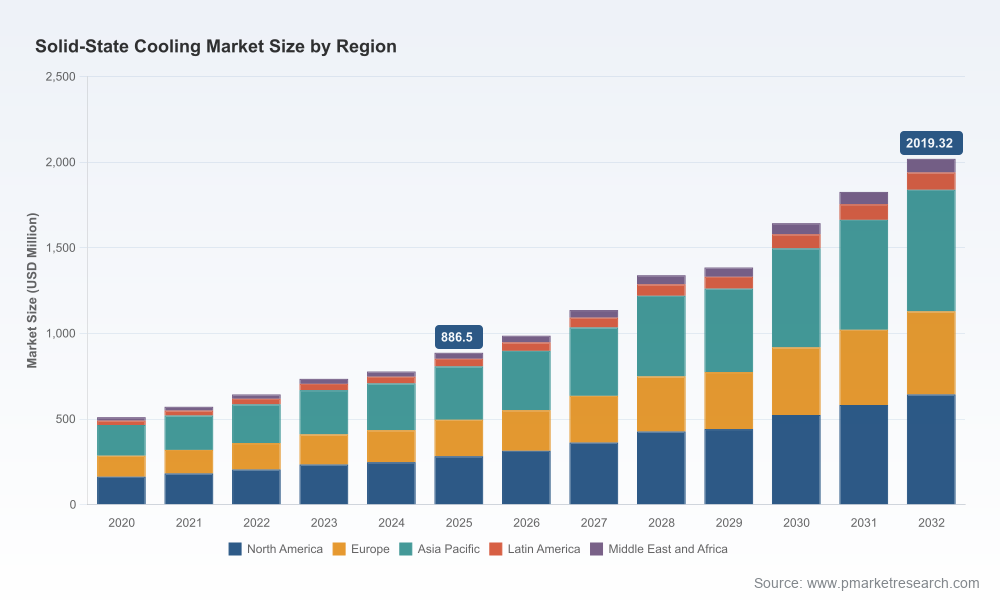

PW Consulting today releases a strategic industry brief drawn from our forthcoming Solid State Cooling Market research report (base year 2025, forecast 2026–2032). The analysis quantifies a market that has moved from approximately USD 510 million in 2020 to roughly USD 886.5 million in 2025, and which our modelling projects to exceed USD 2.0 billion by 2032 — a trajectory underpinned by a 12.48% compound annual growth rate over the forecast period. For corporate leaders and investors preparing 2026 budgets and roadmaps, this report translates growth forecasts into a practical set of go-to-market and technology decisions, risk mitigations, and near-term investment priorities.

Solid State Cooling Market

Solid-state cooling is transitioning from niche, application-specific deployments into broader adoption vectors driven by three converging forces: regulatory pressure on HFC refrigerants, vibrant innovation in thermoelectric and thin-film materials, and accelerating demand for compact, precise thermal management in electronics, medical devices, and cold chain logistics. The market’s mid-teens growth rate is not uniform across use-cases or regions — and that variability is the very reason firms must make targeted decisions in 2026 rather than broad, undifferentiated bets.

Solid State Cooling Market

Capital allocation: Firms that wait risk over-investing in legacy cooling modalities or, conversely, being late to field-proven solid-state solutions where they are already cost-competitive.

Solid State Cooling Market

Technology adoption: Breakthroughs in materials science can compress time-to-market for higher-efficiency modules; license vs build choices made in 2026 will determine competitive positioning through 2030.

Supply chain and regulatory exposure: Dependence on specific thermoelectric raw materials creates procurement and geopolitical risk that requires active mitigation this fiscal year.

PW Consulting’s full report is built for actionable decision-making. It blends top-down market sizing and five-point scenario modelling with bottom-up commercial tactics. Highlights include:

Market sizing and near-term demand curves (2026–2032) with sensitivity testing for price, efficiency, and regulatory drivers.

Segment maps by technology class, end-market use-case, and go-to-market readiness — each accompanied by supplier capability matrices and win-loss archetypes.

Supply chain stress-tests focused on key thermoelectric materials and component procurement lead times, plus suggested sourcing playbooks.

Commercial templates: vendor selection scorecards, CAPEX/OPEX modelling spreadsheets, and pilot-to-scale rollout checklists that procurement, engineering, and corporate development teams can adopt immediately.

Investment and M&A playbook: rationale, valuation heuristics, and integration risks tailored for acquirers and PE investors evaluating buy-and-build strategies in 2026.

IP and standards landscape: patent mapping, regulatory compliance requirements (e.g., laboratory and industrial safety standards), and recommended engagement pathways with standards bodies.

The vendor landscape is characterized by a mix of long-established component manufacturers, system integrators, and start-ups pursuing higher-efficiency materials and novel architectures. Market concentration metrics indicate a moderately consolidated market: the top three players account for roughly 38% of industry revenue, while the top five account for just over half. This structure creates strategic openings for both scale-driven incumbents and agile specialists.

Ferrotec Holdings Corporation (Japan) — a leading global manufacturer focused on thermoelectric modules and assemblies. Their scale in component production and established industrial channels makes them a natural partner for OEMs seeking reliable supply and integration support.

Coherent Corp. (United States) — leveraging legacy thermal management expertise (including the II-VI Marlow portfolio) to serve precision electronics and research markets. Their strength lies in high-reliability modules for sensitive applications.

Laird Thermal Systems (United States) — a solutions-oriented provider for medical and industrial customers where compliance and lifecycle support matter more than raw price.

Phononic, Delta Electronics, Solid State Cooling Systems, TECA Corporation, and TE Technology — each occupies a differentiated niche from systems-level refrigeration to integrated power-and-thermal solutions, enabling a range of partnership or competitive responses depending on a buyer’s strategic priority.

Regional and specialist producers (including several smaller, regionally focused manufacturers) provide alternative sourcing options but present variability in capacity and standards alignment — factors our procurement playbook addresses.

Strategic implication: 2026 is the year to choose whether to consolidate via M&A to secure scale and margins, or to form multi-party alliances to accelerate adoption of advanced materials and shared manufacturing investments. The market structure supports both options.

Two dynamics are particularly material for strategic planning:

Materials and efficiency breakthroughs. In 2025, a nano-engineered thin-film thermoelectric material (CHESS) demonstrated by Johns Hopkins Applied Physics Laboratory showed near-doubling of device efficiency in lab validation. The technology has attracted awards and attention — and it is the type of innovation that accelerates commercial tipping points when coupled with scalable manufacturing and licensing pathways.

Regulatory and standards pressure. International guidelines for data center thermal envelopes, laboratory safety requirements, and the global drive to phase down HFC refrigerants are creating demand-side incentives for refrigerant-free, solid-state solutions. Compliance with safety standards remains a gating factor for medical and lab deployments.

Operational risk: thermoelectric modules today largely rely on materials such as bismuth telluride. That concentration of raw-material dependency, combined with localized manufacturing capacity, creates supply and price volatility that should be mitigated in 2026 through multi-sourcing, recycling programs, and conditional long-term purchase agreements.

For executives charting strategy in 2026, PW Consulting recommends a three-horizon approach with measurable near-term moves:

Run technology scouting sprints focused on thin-film and advanced thermoelectric IP (including licensing opportunity assessments for CHESS-style innovations).

Initiate pilot deployments in high-value, low-volume applications where solid-state cooling already meets economic thresholds (e.g., telecom, precision lab equipment, select cold-chain use-cases).

Hedge material supply: execute conditional offtake and recycled-material programs for bismuth telluride and establish alternate supplier qualification tracks.

Lock in integration partnerships with established module suppliers for rapid scale while concurrently accelerating in-house expertise for systems integration.

Deploy the report’s vendor selection scorecards and CAPEX/OPEX templates to validate unit economics across target use-cases.

Engage with standards bodies and regulators to de-risk compliance pathways for medical and industrial certifications.

Pursue targeted M&A to acquire manufacturing scale or differentiating IP where valuation and integration risk align with long-term cost curves.

Scale pilots into commercial rollouts in high-growth verticals informed by ongoing COP (coefficient of performance) and lifecycle cost measurements.

Cost per watt of cooling and COP improvement trajectories for deployed modules.

Supplier lead times and concentration ratios for key raw materials.

Patent filings and licensing activity around advanced thermoelectric films.

Pilot-to-production conversion rates and total cost of ownership deltas versus vapor-compression alternatives.

This release is designed as a strategic preview: it synthesizes market momentum, offers actionable recommendations for 2026, and maps the competitive terrain. The full PW Consulting report includes granular segment modeling, downloadable decision tools, detailed supplier scorecards, and proprietary excel-based scenario models that quantify ROI across 20+ use-case permutations. To preserve client value and encourage informed engagement, we intentionally exclude the detailed segmentation tables and per-region/application revenue splits in this public summary — those detailed outputs are provided to report purchasers and advisory clients.

As the solid-state cooling market moves beyond laboratory milestones toward commercial utility, 2026 will be a pivotal year for strategy. Firms that combine disciplined technology evaluation, prudent supply-chain hedging, and targeted commercial pilots will be best positioned to capture share as the market scales toward the multi-billion-dollar horizon we forecast for 2032. PW Consulting’s report converts that horizon into a set of near-term actions — the kind of playbook we recommend every executive use to turn market potential into competitive advantage.

For detailed analysis of this topic, please visit the official page:Solid State Cooling Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com