Candidiasis Industry Growth Report: Key Drivers and Strategic Insights

Other |

2026-03-11 07:31:12

PW Consulting’s latest market study on Purpura Treatment provides a focused, decision-grade briefing for executives planning resource allocation, clinical development, commercial launches, or M&A activity in 2026. Built on a 2020–2025 historical base and forward-looking to 2026–2032, the study quantifies market momentum (project CAGR 5.85% through the forecast window) and translates epidemiology, regulatory change, payer behavior and supply-side constraints into explicit strategic options. The total market — measured in USD Million — demonstrates steady growth between the recent base year and our 2032 outlook; this trajectory underpins several near-term commercial inflection points that every biopharma and investor team must prepare for now.

Purpura Treatment Market

Validation of growth vectors: The market is expanding at a mid-single-digit compound rate, but that headline masks tactical opportunities and tactical risks that can materially affect 2026 P&L and 2027 planning cycles. Timing of label expansions, pediatric approvals, and late‑stage combination data will disproportionally influence uptake in targeted segments.

Purpura Treatment Market

Regulatory and reimbursement inflection: 2025 saw multiple regulatory events that reset clinical practice and payer coverage playbooks. Those approvals (including new mechanisms of action and pediatric label expansions) create immediate needs for real‑world evidence, value dossiers and refined contracting strategies as payers tighten prior‑therapy rules.

Purpura Treatment Market

Concentration and competitive tension: Market concentration is meaningful at the top — our CR3 and CR5 metrics show a market where a small group of incumbents controls a substantial share. That dynamic increases the value of differentiated clinical positioning and strategic partnerships for new entrants and mid‑sized players.

Supply and manufacturing constraints: IVIG‑dependent segments remain sensitive to plasma supply cycles. Manufacturers and downstream purchasers must integrate donor availability, fractionation capacity and inventory planning into their 2026 operating plans.

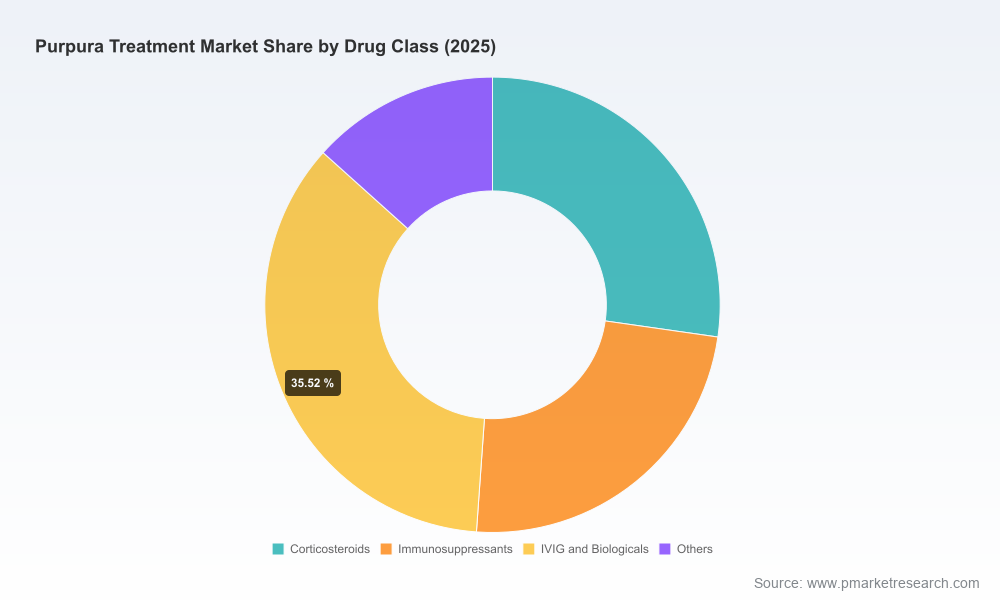

Transparent market-sizing methodology and downloadable models: an auditable synthesis from epidemiology to treated-patient forecasts and pricing assumptions. (Note: the full report contains detailed segmented splits by geography, drug class and indication; these segmentation tables are intentionally reserved for the full report.)

Commercial playbooks: launch-readiness checklists, payer engagement timelines, targeted evidence generation blueprints (randomized and RWE studies), and country‑level reimbursement scenarios to inform list & net pricing decisions.

Clinical and pipeline heat maps: molecule-level competitive positioning, expected launch windows, likely label scopes, and recommended head‑to‑head or combination trial designs to secure formulary preference.

Supply-chain risk matrix: plasma sourcing sensitivity analyses, inventory stress tests for IVIG suppliers, and contingency sourcing strategies for small molecules and biologics.

Deal and portfolio diagnostic: M&A targets, licensing candidates and partnership frameworks, prioritized by strategic fit and value creation potential over a 24–36 month horizon.

Our competitive review focuses on the established innovators and recent entrants that are shaping 2025–2026 dynamics. Below we summarize strategic posture and implications for planning.

Amgen: With a mature thrombopoietin receptor agonist franchise, Amgen benefits from established physician familiarity and broad clinical experience. Its strategic choices in label expansion, patient support services and contracting will be decisive for defense against novel modalities; incumbency confers bargaining leverage but also heightens the need for incremental evidence to justify premium positioning.

Novartis: Combination approaches demonstrated by recent phase‑III results point to opportunity for differentiated regimens that alter the treatment sequence. Novartis’s data suggest potential to carve out share by combining established agents with immunomodulatory partners — an important signal for competitors to consider alliance or trial strategies that test synergistic positioning quickly.

Sobi: Pediatric label extensions and formulation innovations are meaningful revenue accelerants and improve access in a previously under‑served population. For competitors, pediatric approvals raise the bar for evidence generation and post‑market support; for payers, they create new coverage questions that can be shaped with targeted health‑economics submissions.

Sanofi: The arrival of a BTK inhibitor for chronic cases introduces a new mechanism into standard of care. Strategic playbooks should evaluate sequencing scenarios (e.g., where BTK fits versus TPO‑RAs, SYK inhibitors or FcRn blockers), and competitors should prioritize comparative effectiveness and bleed‑risk data to defend or attack this segment.

Rigel: With an oral SYK inhibitor in market, commercialization execution and IP management remain focal. Ongoing litigation resolution and reinforcement of real‑world value will determine its sustainable share; alliance partners should assess litigation outcomes when modeling acquisition or co‑promotion angles.

Grifols: As a major IVIG supplier, Grifols’s operational capacity, donor base and fractionation footprint directly influence availability and pricing of IVIG therapies. Supply disruptions or pricing pressure in IVIG affect downstream demand for alternative agents — an effect we model across multiple coverage and supply scenarios.

argenx: FcRn blockade is altering the mechanism set available to clinicians. Where FcRn entry is broad and durable, it changes the calculus for retreatment intervals and total cost of care; manufacturers of other novel modalities should prioritize head‑to‑head comparative programs or seek combination data where biologically rational.

Regulatory volatility: 2025’s approvals broaden treatment options but also invite stricter utilization management. Expect intensified dialogue with regulators and payers on pediatric labeling, off‑label use and long‑term safety surveillance.

Payer policies: Coverage often remains contingent on prior therapy failure and documented bleeding risk. Manufacturers must prepare durable value evidence, including cost offsets from reduced hospitalizations and transfusion avoidance.

Raw‑material constraints: Plasma‑derived product availability is not static. Donor programs, fractionation lead times and inventory practices are levers that commercial teams must manage proactively.

Clinical uncertainty: Late‑stage combination trials and real‑world adoption will determine whether new modalities displace or complement existing therapies; scenario planning is essential to avoid misallocated commercial spend.

Prioritize evidence that moves payers. Invest selectively in head‑to‑head or pragmatic trials and high‑quality RWE that target payer concerns (bleeding events, hospitalization avoidance, total cost of care). Time submissions to coincide with product launches or label extensions.

Design segmentation-based launch plans — but validate locally. Use our country‑level demand models to sequence market entries and tailor patient access programs; reserve capital to accelerate uptake in markets with favorable net pricing and less restrictive prior‑authorization rules.

Mitigate supply risk for IVIG-dependent portfolios. Secure longer‑term agreements with fractionators, diversify plasma sourcing, and build inventory buffers tied to stress‑test scenarios we provide in the report.

Leverage strategic partnerships to accelerate differentiation. Consider co‑development, licensing or combo trials with companies holding complementary mechanisms (e.g., BTK, FcRn, TPO‑RA). Partnerships can be quicker and less capital‑intensive than stand‑alone development.

Embed commercial and payer intelligence into R&D prioritization. Align molecule development decisions with modeled net revenue and uptake timelines under multiple reimbursement scenarios — use threshold analyses to determine go/no‑go and resource allocation.

We provide bespoke advisory services that translate our market model and competitive insights into operational plans: launch readiness workshops, bespoke payer evidence generation blueprints, M&A target screening and due diligence, contract & pricing simulation, and plasma‑supply advisory. For product, commercial and corporate development teams facing 2026 inflection points, we deliver the applied analyses and playbooks that reduce time‑to‑value and de‑risk execution.

In keeping with the “preview” approach, this release highlights strategic implications and the types of analyses included in the full study. We have intentionally omitted the granular segmented tables and numeric splits by region, drug class and indication — these detailed breakdowns, along with interactive model files and downloadable scenario outputs, are available in the complete PW Consulting Purpura Treatment Market report.

To obtain the full dataset, segmentation matrices, and the spreadsheet models that power our forecasts and recommended actions, visit PW Consulting’s market research portal or contact our subscription desk for access. Equip your 2026 planning with the empirically grounded intelligence that reduces execution risk and surfaces the highest‑value strategic moves.

For detailed analysis of this topic, please visit the official page:Purpura Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com