Refined Wood Vinegar Market: Strategic Imperatives for 2026 — PW Consulting Release

Executive Summary

PW Consulting’s new market intelligence on Refined Wood Vinegar synthesizes multi-year primary research and modelling to equip executives with the evidence they need for 2026 strategic planning. Our baseline shows the global refined wood vinegar market expanding from USD 5.6 Million in 2020 to USD 7.54 Million in 2025, and we project continued growth across the 2026–2032 forecast window—reaching USD 11.35 Million by 2032 under the base-case scenario. The modeled compound annual growth rate for the forecast period is 6.02%, reflecting steady demand growth driven by agricultural adoption, food and cosmetic applications, and the increasing industrialization of pyrolysis value chains.

Refined Wood Vinegar Market

Why this report matters for 2026 decision cycles

- Provides a defensible top‑line market sizing that supports capital allocation and go/no‑go decisions for new processing capacity and purification investments.

- Maps the dual nature of wood vinegar as both a higher‑value refined product and a byproduct of biochar/carbon removal projects—enabling new circular-business models for agritech and bioenergy players.

- Delivers supplier performance analytics and a risk matrix that help procurement and commercial teams prioritize supply relationships and certification pathways ahead of scale-up.

Market Dynamics: Drivers, frictions and inflection points

Three structural forces are shaping the refined wood vinegar market heading into 2026:

Refined Wood Vinegar Market

- Circular bioeconomy scaling. Industrial-scale pyrolysis projects (often centered on biochar for carbon removal) are producing incremental volumes of wood vinegar as a co‑product. Where projects are structured for high‑integrity MRV and carbon credit frameworks, wood vinegar becomes an additional value stream—strengthening project economics and creating integration opportunities for agricultural supply chains.

- Premiumization via refinement and certification. Refined grades—created through controlled distillation, tar removal and targeted organic acid standardization—command a pricing premium versus crude byproducts because they enable feed, food and cosmetic applications. Certification for organic use (e.g., OMRI) and documented purity parameters materially expand accessible end markets.

- Operational and supply-side variability. Feedstock heterogeneity, production temperature regimes and purification choices create meaningful divergence in product quality and suitability. Our analysis highlights short windows of mid‑horizon volatility driven by capacity additions and feedstock seasonality; companies must plan for both demand acceleration and episodic supply fluctuations.

Segmentation and growth pathways (what we analyze)

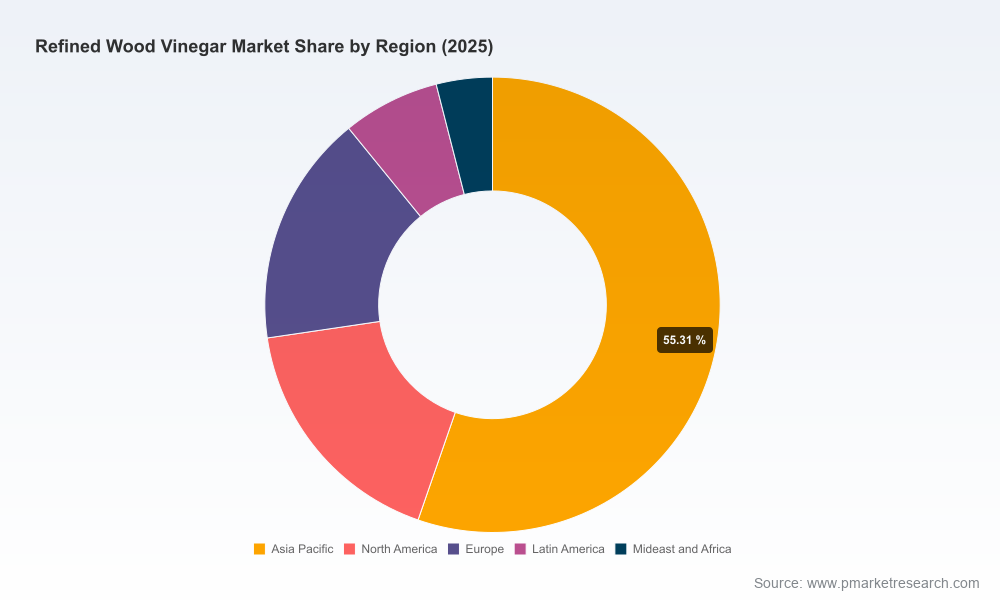

The report dissects the refined wood vinegar market across interlocking dimensions—product grade, application verticals and regional demand centers—then models addressable market trajectories under alternative adoption scenarios. Rather than reproduce granular segment tables here, we outline how executives can use the segmentation analysis:

Refined Wood Vinegar Market

- Prioritize investment by grade: our score‑card links refining intensity, unit economics and addressable revenue pools to identify the highest‑return purification investments.

- Go‑to‑market sequencing: channel and pricing playbooks aligned to high‑margin applications reduce time to revenue when launching refined offerings.

- Supply integration strategies: we model win‑win partnership structures between biochar project developers and off‑takers to stabilize supply while preserving carbon integrity.

If your team needs the exact segment tables and regional breakouts to quantify ROI by use case, the full dataset and downloadable spreadsheets are available on the report page.

Competitive Landscape — concentration and profiles

The refined wood vinegar market exhibits a moderate level of concentration: our CR3 sits in the low‑40s percentile and CR5 approaches the high‑50s percentile, indicating meaningful market share for headline suppliers while leaving room for specialist entrants and project‑level aggregators.

- VerdiLife (United States) — Supplies high‑quality distilled and purified wood vinegar optimized for organic agriculture and crop biostimulant use. https://verdilife.com/

- Nara Tanka Industries Co., Ltd. (Japan) — Produces high‑temperature refined vinegar using Bincho charcoal processes, emphasizing pH control and removal of adverse components for horticultural and deodorization applications. https://naratanka.com/en/wood-vinegar/

- Hongsen Carbon (Shijiazhuang Hongsen Activated Carbon Co., Ltd.) (China) — Factory‑scale manufacturer of industrial‑grade wood vinegar, offering bulk stabilization and QA certifications for agricultural and industrial users. https://www.hongsencarbon.com/

- Other active suppliers and innovators: Nettenergy B.V., ACE (Singapore) Pte Ltd, TAGROW CO., LTD., Canada Renewable Bioenergy Corp., Byron Biochar, Seneca Farms Biochar LLC, and PyroAg Pty Ltd. These companies reflect a mix of technology‑led processors, biochar ecosystem participants and regional champions.

Recent industry developments reinforce consolidation around integrated pyrolysis projects and product differentiation. Notably, a 2026 partnership to deploy large‑scale biochar carbon removal projects in India underlined how industrial pyrolysis lines can codify wood vinegar as a planned co‑product for local farmland application. Similarly, supplier branding moves—such as Seneca Farms’ rebranding of its agricultural product line—signal a maturing market where purity claims and OMRI‑style listings become commercial levers.

Regulatory and certification context

Regulatory recognition and certification materially alter demand curves for refined products. When wood vinegar meets organic standards and documented impurity limits, it unlocks segments in certified agriculture and specialty food/cosmetics. Concurrently, alignment with high‑integrity carbon MRV frameworks for biochar projects creates a compliance advantage for integrated producers—particularly where wood vinegar use is explicitly contemplated in project economics.

Practical playbook for 2026: actions by role

- CEOs & CFOs — Reassess capital allocation to purification capacity vs. long‑term supply contracts; model blended returns accounting for co‑product revenue from biochar projects and the probability‑weighted uptake of premium applications.

- Commercial teams — Lock early‑adopter contracts in high‑value end markets (organic farming, feed additives, food flavor segments) and articulate purity and certification roadmaps in customer offers.

- R&D & Operations — Prioritize investments in scalable tar removal, standardized acetic‑acid titration, and QA/QC protocols that reduce batch variability; explore partnerships for pyrolysis process optimization to secure predictable co‑product quality.

- Corporate Development — Target tuck‑ins that expand purification capability, secure feedstock, or provide certification pathways; our M&A shortlist in the full report highlights candidate profiles and valuation heuristics.

What the PW Consulting report contains (high‑utility deliverables)

- Verified market sizing (historical 2020–2025) and modelled projections for 2026–2032 with alternate scenarios.

- Supplier scorecards and comparative technology assessments, including distillation and stabilization options.

- Price and margin framework for refined vs. crude grades, and sensitivity diagnostics for feedstock and purification costs.

- Regulatory heatmaps and certification pathways (organic listings, MRV alignment for biochar projects).

- Commercial playbooks: channel segmentation, contract templates, and sample off‑take structures tied to carbon projects.

- M&A and partnership shortlist, with integration risk checklists and valuation anchors.

To protect competitive integrity and to comply with our “prequel” principle, the report presents full tabular detail, Excel models and company revenue estimates in the paid report package—these granular assets are intentionally withheld from this summary.

Implications for 2026 planning

For firms that move early to align purification capability with certification pathways and secure integrated supply from pyrolysis/biochar projects, refined wood vinegar can become a differentiated, margin‑accretive business line. Conversely, firms that defer investment risk losing premium market share to processors that marry quality assurance with organic and carbon credentials. The market’s measured CAGR of 6.02% masks important pockets of faster adoption; our report helps identify those pockets and quantify the upside to targeted investments.

Next steps

Executives preparing 2026 strategies should request PW Consulting’s full Refined Wood Vinegar Market report to access the complete dataset, supplier scorecards, and executable go‑to‑market templates. The full report includes downloadable models and a one‑hour briefing with our senior analysts to walk through scenario outcomes and answer bespoke questions about your portfolio or project pipeline.

For detailed analysis of this topic, please visit the official page:Refined Wood Vinegar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com