Aircraft Auxiliary Power Unit Market Segmentation, Demand, and Future Opportunities

Crafts |

2026-06-04 07:08:24

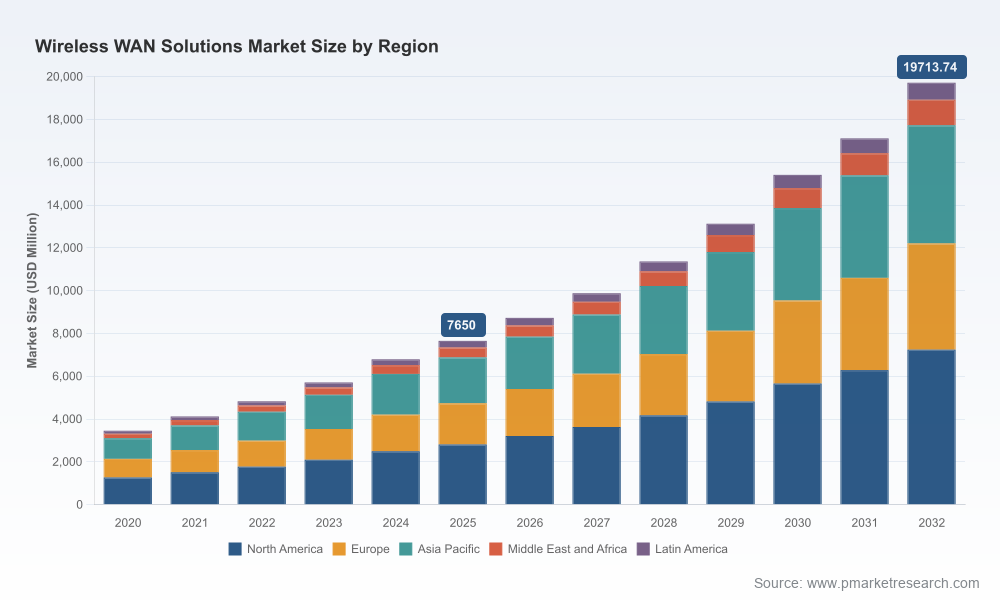

PW Consulting today publishes an executive-level briefing accompanying our full Wireless WAN Solutions Market research report. The briefing synthesizes the strategic implications of a market that has expanded from a multi-billion-dollar base in 2020 to an estimated USD 7,650 million in 2025, and is now forecast to approach roughly USD 19.7 billion by 2032 — representing a compound annual growth rate of 14.48% over the 2026–2032 forecast window. For enterprise and infrastructure decision-makers planning 2026 budgets and multi-year roadmaps, this trajectory is both an opportunity and a constraint: it signals rapid supplier innovation and competitive consolidation, while raising the bar for disciplined vendor selection, TCO planning, and regulatory risk management.

Wireless Wan Solutions Market

Timing procurement and pilots: With accelerated adoption cycles driven by 5G and SD-WAN convergence, 2026 will be a pivot year for pilots that need to scale in 2027–2028. Our analysis identifies the inflection points that recommend starting pilots in 2026 versus deferring to later windows.

Wireless Wan Solutions Market

Capital allocation and TCO discipline: Strong market growth masks a wide dispersion in unit economics across deployment types. The report equips CFOs and network leads with scenario-adjusted cost models to compare private 5G, managed wireless WAN, and hybrid cellular failover architectures.

Wireless Wan Solutions Market

Regulatory & supply-chain risk: Spectrum policy, export controls, and regional standards will materially affect vendor viability and deployment timetables — elements that must be embedded into contracts signed in 2026.

Granular market sizing and trend maps: We model the Wireless WAN market from 2020 through 2032, supplying a transparent methodology, historical reconciliation, and forward scenarios that underpin procurement decisions.

Segmentation frameworks: The study breaks the market into region, component (hardware vs software & services), and technology (notably 4G LTE vs 5G categories), enabling comparison of demand drivers without exposing proprietary client-level data.

Competitive intelligence dossiers: Structured profiles on the leading vendors, with capability matrices, go-to-market plays, partnership footprints, and an M&A watchlist to inform vendor shortlists and partnership strategies.

Deployment playbooks and RFP templates: Step-by-step blueprints for enterprise pilots, edge routing architectures, site selection heuristics, and pre-configured RFQs to speed procurement cycles.

Operational readiness tools: KPIs for SLA negotiation, security checklists for wireless uplinks, and failure-mode cost calculators to model availability requirements for branch, industrial, and mobile use cases.

Regulatory and compliance guide: A practical digest of spectrum, export control, and net neutrality considerations tailored to multi-jurisdiction deployments, with compliance checkpoints for commercial contracts.

The Wireless WAN market’s growth is being driven by several convergent forces. First, the maturation of 5G — and its continued evolution through releases such as 3GPP Release 17 — is unlocking new enterprise use cases that require low latency and deterministic behaviors (e.g., mission-critical push-to-talk, remote robotics). Second, SD-WAN and edge compute architectures are making heterogeneous access (fiber + fixed wireless + cellular) a practical operations model for distributed enterprises. Third, cost and deployment economics for densification — notably small cells — remain a material constraint; recent industry benchmarks place average 5G small-cell deployment cost per site in the tens of thousands of dollars, which must be built into ROI calculations for urban and industrial rollouts.

Policy and regulation will be decisive. Past spectrum allocations and auctions have set the stage for mid-band 5G growth; meanwhile, regional regulations on network neutrality and export controls are reshaping vendor selection and contract language. Organizations must assume that cross-border deployments will require bespoke compliance paths and contingency sourcing to avoid late-stage project delays.

The market exhibits moderate concentration: the top three vendors capture a substantial share of supply, and the top five consolidate a clear majority of the market’s revenue pool. This concentration has important implications for pricing power, innovation diffusion, and partnership strategies.

Cisco Systems (San Jose, CA) — Strengths: integrated edge-to-cloud portfolio (Meraki gateways, Catalyst industrial routers) and mature SD-WAN integrations. Strategic posture: focus on managed services and enterprise-grade orchestration.

VMware (Broadcom, Palo Alto, CA) — Strengths: VeloCloud SD-WAN with robust cellular uplink options. Strategic posture: software-led differentiation and partnerships with carriers for managed offerings.

Ericsson (Stockholm, Sweden) — Strengths: RAN and core for large-scale wireless WAN infrastructure. Notable: launched 5G Advanced connectivity solutions in late 2025 to broaden IoT and reduced-capability device support.

Nokia (Espoo, Finland) — Strengths: end-to-end RAN and service routing; recent deployments of standalone 5G core in multiple live networks expand capacity for enterprise WAN use cases.

Huawei Technologies (Shenzhen, China) — Strengths: cost-competitive RAN and SD-WAN appliances for global deployments; faces geopolitical and export control considerations in certain markets.

Pepwave (Hong Kong) — Strengths: rugged multi-WAN routers and LTE/5G bonding for resilient failover at the edge — a practical choice for remote and vehicular deployments.

Major carriers (Verizon, T-Mobile US, Sprint post-merger, Cricket Wireless) — Strengths: nationwide footprint and private 5G offerings; their coverage expansions and protocol activations materially change the service economics for enterprises choosing managed wireless WAN.

Recent vendor moves — including Ericsson’s 2025 product launches, Nokia’s standalone core deployments, Cisco’s industrial router upgrades, Verizon’s mmWave expansion, and carrier protocol rollouts — underscore the pace of technological and commercial innovation. Procurement teams should assume support timelines for new features will be measured in quarters, not years.

Run dual-track pilots: parallel proof-of-value for private 5G (in controlled campuses) and managed cellular SD-WAN (for distributed branches). This hedges vendor and spectrum risk while accelerating operational learning.

Embed regulatory clauses in contracts: require vendor evidence of export compliance and a remediation plan for firmware/crypto restrictions that could affect device shipments across borders.

Optimize CAPEX/OPEX mix: favor phased CAPEX with performance-linked milestones and managed service overlays to convert unpredictable rollout costs into contractually bounded OPEX where appropriate.

Prioritize resilience and multi-provider strategies: design for multi-carrier uplinks and active-active routing at critical edge sites to mitigate single-vendor coverage failures.

Insist on measurable SLAs for wireless performance and include penalties for availability/latency breaches; use the report’s standardized KPI set when negotiating.

PW Consulting’s full report is intentionally structured to be executable. Beyond the market narrative, it includes downloadable models, vendor scorecards, RFP artifacts, and pilot checklists that procurement and network teams can adapt immediately. Given our “trailer” approach in this briefing, readers will find the complete datasets — including the full segmentation tables, granular regional forecasts, and proprietary vendor scoring — in the core report and online data appendices.

For executives building 2026 roadmaps, the critical choices are not whether Wireless WAN will matter — it already does — but how to sequence investments, allocate risk, and choose partners that align with strategic priorities (latency, security, scale, or cost). The evidence supports a disciplined, scenario-based approach: start small with high-impact pilots, secure contractual protections that reflect regulatory realities, and use vendor competition to preserve optionality as the market consolidates.

Download the full report and supporting data to access detailed segmentation, the vendor scorecards, and the financial models that underlie our forecasts.

Book a strategy workshop with PW Consulting for a customised migration plan, vendor selection process, and pilot design tailored to your industry and footprint.

PW Consulting’s Wireless WAN Solutions Market report combines market rigor with operational practicality. For 2026 planning cycles — whether you are an enterprise CIO, a network architect, or a carrier strategy lead — the report offers the tools required to translate market momentum into measurable business outcomes while managing the regulatory and supplier risks that define the competitive landscape.

For detailed analysis of this topic, please visit the official page:Wireless Wan Solutions Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com