Application Modernization Services Supporting Remote and Hybrid Work

Networking |

2026-01-29 08:21:05

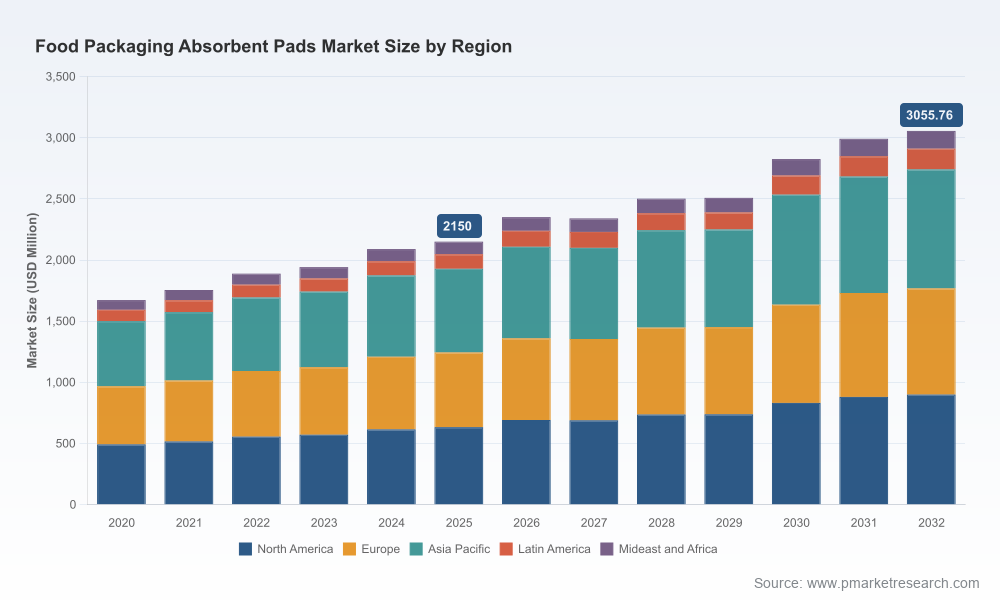

PW Consulting’s latest industry briefing on the Food Packaging Absorbent Pads market is designed as an operational playbook for executives making investment, sourcing, and product strategy decisions in 2026. The market we track has expanded steadily from a sub‑USD 1.7 billion base in 2020 to roughly USD 2.15 billion in our 2025 base year, and our updated forecast points to continued, mid‑single‑digit growth — a compound annual growth rate of approximately 5.15% across the 2026–2032 horizon, bringing total market value into the low‑USD 3.0 billion range by 2032. These macro dynamics create a landscape where incremental innovation, regulatory positioning, and supply‑chain design will determine winners and losers.

Food Packaging Absorbent Pads Market

Actionable foresight. We translate market trajectory and regulatory shifts into concrete tactical options for procurement, R&D, and commercial teams — not just forecasts. If you are evaluating manufacturing expansions, material substitution roadmaps, or commercial contracts to service major retail customers, the report is structured to shorten the path from insight to decision.

Food Packaging Absorbent Pads Market

Risk‑first framing. With regulations in Europe and the United States increasingly defining acceptable material chemistries and use cases, our scenario analysis maps regulatory outcomes to product design and labeling choices so you can prioritize compliance spend and certification timelines.

Food Packaging Absorbent Pads Market

Competitive and supplier playbook. The market remains moderately fragmented (CR3 ~25.5%; CR5 ~38.2%), which means scale matters for raw material sourcing and service reliability but there is room for targeted consolidation and niche leadership. We supply benchmark matrices and negotiation templates to improve supplier economics without sacrificing quality or compliance.

Top‑down market sizing and stress‑tested forecasts: We present audited historicals and scenario‑based forecasts through 2032. The 2020–2025 trendline and a mid‑case 5.15% CAGR form the foundation for demand planning.

Go‑to‑market playbooks: Retail pack size, private label economics, and channel segmentation analyses with turnkey recommendations for pricing tiers, margin corridors, and promotional allowances aligned to different retailer procurement models.

Materials and supply‑chain toolkit: Detailed cost drivers for cellulose, superabsorbent polymers (SAP), silica gel and bio‑based alternatives, plus decision trees for localizing versus centralizing production and guidance on contract structures to hedge raw material volatility.

Regulatory readiness checklist: Practical compliance steps for EU and US jurisdictions, including documentation, testing protocols, and labeling requirements that reduce lead time to shelf approval.

Product and sustainability roadmaps: Lifecycle assessment templates, compostability certification pathways, and retrofit guidelines for converting existing lines to handle biodegradable or cellulose‑dominant pads.

Commercial due diligence assets: Vendor scorecards, RFP templates, and KPI dashboards you can drop into procurement platforms to accelerate vendor selection or M&A diligence.

Regulatory re‑classification and product design. European rules treating certain SAP‑containing absorbers as active packaging devices require manufacturers to demonstrate containment and capacity to prevent leakage or food contact. In parallel, US food‑contact approvals remain a gating factor for new materials. These dynamics elevate testing, third‑party certification, and traceability as non‑negotiable tasks for any product launch or cross‑border sale.

Sustainability and material substitution. Public and regulatory pressure to reduce single‑use plastics is accelerating adoption of cellulose‑based and compostable pads, especially in markets with advanced waste‑management infrastructure. However, material substitution is not a one‑size‑fits‑all decision: absorption profile, odor control, and cost must be balanced against end‑of‑life claims and retailer shelf expectations.

Performance innovations. Recent product announcements indicate the near‑term battleground will be absorption speed, biodegradability, and integrated odor control. Faster uptake and compostability together create compelling retail propositions, but require re‑engineering of film perforation and pad construction to preserve hygiene and shelf life.

Profiles to watch. The market is populated by a mix of global suppliers and specialist regional manufacturers. Leaders combine SQF/BRCGS/FDA‑compliant manufacturing footprints with strong retailer relationships and innovation pipelines. Notable operators include Novipax, which emphasizes multiple SQF‑certified sites and supply reliability in North America; Sirane, with a product range focused on odor control and custom absorbency; and Aptar Food Protection, offering patented food‑safe pad systems. European and Asian players round out the ecosystem with differentiated capabilities in nonwovens and cost leadership.

Recent strategic moves. Product innovation and capacity expansion are accelerating: manufacturers have introduced biodegradable pads with faster absorption rates and expanded facilities to meet growing demand for odor‑controlling solutions. These moves highlight two concurrent strategies — premium differentiation through performance and sustainability, and volume capture via expanded, regionalized manufacturing.

Implication for incumbents and new entrants. Incumbents with diversified geographies and certification portfolios can defend accounts by bundling logistics and testing services. New entrants can still establish footholds by targeting niche channels (e.g., premium seafood or compostable produce packs) and partnering with pack film specialists to reduce time‑to‑shelf.

1. Short‑term (0–12 months): Secure supply and certify. Prioritize multi‑sourcing for critical raw inputs (cellulose pulp, food‑grade SAP) and complete FDA/EU documentation for any new material. Use short‑term offtake agreements to stabilize price exposure while piloting alternative materials with select retail partners.

2. Medium‑term (12–36 months): Product differentiation and footprint optimization. Invest selectively in R&D for faster‑absorbing, compostable pads; deploy pilot lines rather than full greenfield sites where possible. Evaluate contract manufacturing partnerships to accelerate geographic coverage while preserving capital.

3. Strategic (36+ months): Scale through partnerships and targeted M&A. With the market still moderately fragmented, acquisitive deals to secure proprietary formulations, certifications, or regional production capacity can be value‑accretive. Prioritize targets with demonstrable certificate status and established retail contracts.

Sourcing: Shift procurement KPIs to include certification lead times and product changeover costs, not just unit price. Build contingency inventories for key components timed to certification renewals and seasonal demand peaks.

Manufacturing: Standardize modular lines that can switch between cellulose and SAP formulations with limited downtime. Add inline testing for absorption and particulate leakage to reduce shelf‑level failures.

Commercial: Negotiate tiered pricing tied to sustainability metrics and guaranteed shelf life. Offer retailers pilot programs that split development risk and provide co‑branded sustainability narratives.

Decision‑ready diagnostics. We provide CapEx calculators, payback models, and sensitivity analyses that translate market growth and material cost assumptions into approval‑ready investment cases.

Regulatory and safety matrices. Our step‑by‑step compliance checklists remove ambiguity around EU active‑packaging classifications and FDA food‑contact requirements so teams can budget for testing and certification accurately.

Competitive intelligence. The report contains vendor profiles, recent deal tracking, and innovation tracking that help you identify partnership and acquisition targets; however, to preserve competitive value, detailed segment revenue breakdowns and region/application‑level shares are reserved for report subscribers and our client portal.

As the absorbent pads market moves from a mature product category into a performance and sustainability play, executives must treat the next 12–24 months as a window to lock in sourcing resilience, complete regulatory pre‑work, and trial differentiated products with major customers. The market’s steady compounding growth creates opportunity for both scale and specialization — but success will hinge on operational rigor, certification velocity, and the ability to align product claims with verifiable lifecycle credentials.

PW Consulting’s full Food Packaging Absorbent Pads Market report contains the granular segmentation, supplier scorecards, and executable templates referenced above. For teams preparing board materials, RFPs, or capital requests in 2026, the report is structured to convert market intelligence into executable plans that reduce time to market and de‑risk investment.

For detailed analysis of this topic, please visit the official page:Food Packaging Absorbent Pads Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com