Boc-L-Leucine Market 2026: Strategic Imperatives for Procurement, R&D and Supply-Chain Resilience

Executive snapshot

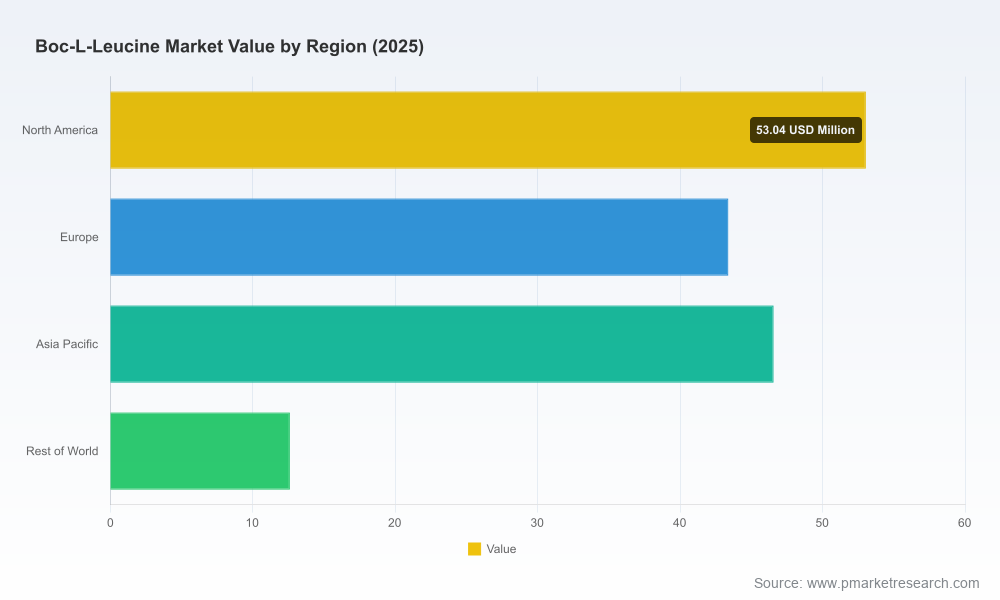

PW Consulting’s Boc-L-Leucine Market Report (base year: 2025) delivers a focused, decision-ready playbook for companies that will make sourcing, manufacturing or investing choices in 2026. The protected amino acid intermediate market that supports peptide synthesis and pharmaceutical manufacturing has expanded substantially in recent years, rising from an estimated market footprint in 2020 to roughly USD 155.6 Million (2025 base). Our forecast through the 2026–2032 horizon points to continued expansion at a compound annual growth rate (CAGR) of 7.45%, taking the overall market to a materially larger scale by 2032.

Boc L Leucine Market

Why this report matters for 2026 strategy

Companies planning supplier contracts, capacity investments or new product introductions in 2026 face a mosaic of supply-side concentration, raw-material volatility, and quality/regulatory expectations. This report translates market-scale dynamics into actionable options: which suppliers to shortlist for long-term contracts, how to structure pricing covenants to hedge raw-material swings, when to accelerate formulation or sourcing shifts to higher-purity grades, and what operational contingencies to build if logistics or fermentation feedstock availability tighten.

Boc L Leucine Market

- Data-driven timing: The market’s historical trajectory and our forecast envelope enable procurement teams to calibrate contract length and escalation clauses to the expected 7.45% CAGR environment.

- Risk-adjusted sourcing: We map supplier capability across quality certification, production technology and distribution reach—so R&D and manufacturing leaders can prioritize suppliers that match their regulatory and scale needs.

- Investment prioritization: For corporate development and M&A teams, the report highlights where scale economies and quality differentiation create margin capture opportunities without disclosing commercially sensitive granular splits.

What’s inside (practical deliverables)

This report is structured as a practical toolkit rather than a descriptive brochure. Key deliverables include:

Boc L Leucine Market

- Market sizing and trajectory: A validated historical series (2020–2025), a 2026 opening-year assessment and a granular forecast through 2032 with scenario sensitivity to raw-material and logistics shocks.

- Supply chain mapping: End-to-end flows from upstream L‑Leucine producers through Boc‑protection manufacturers to distributors and laboratory suppliers; identification of single‑point failure nodes and lead-time benchmarks.

- Supplier scorecards: Operational, quality, and commercial profiles for the competitive set (manufacturing footprint, ISO/regulatory posture, distribution channels, and platform partnerships) to support rapid supplier selection.

- Procurement playbook: Contract templates, hedging strategies tied to amino-acid price drivers, and KPIs to embed into supplier agreements for quality and delivery performance.

- Regulatory and compliance checklist: Practical steps to align procurement and QA/QC teams to expected handling, storage and documentation requirements for research- and pharma‑grade intermediates.

- Opportunity heatmaps: Prioritized routes for product and process improvement—purity upgrades, co-manufacturing partnerships, backward integration into L‑Leucine supply—scored by ROI and execution complexity.

Market dynamics you must consider in 2026

Three dynamics will shape near-term outcomes and should be embedded into next-year planning:

- Upstream feedstock sensitivity. Boc-L-Leucine production is fundamentally linked to the L‑Leucine supply chain. Fermentation-based production dominates high‑purity amino-acid supply, and the broader L‑Leucine complex was estimated at roughly the low‑to‑mid single‑billion USD range in 2025—meaning feedstock economics materially influence protected‑amino‑acid pricing and margin pools.

- Price and logistics shocks. Market participants have already experienced meaningful upstream price moves and transport pressure; US amino‑acid price indices recorded a pronounced spike in early 2026 tied to tighter cargo availability. Procurement teams should therefore model both price volatility and transit reliability when structuring 2026 supplier agreements.

- Quality and regulatory bar. Boc‑protected intermediates are supplied across research and pharma channels, with multiple producers operating to ISO and pharmacopeial standards. Differentiation increasingly rests on certified quality systems, batch-traceability and demonstrated control strategies—attributes that buyers in regulated markets will pay a premium for.

Competitive landscape: who matters and why

The market exhibits a moderate level of concentration: leading vendors command a meaningful share of available capacity while a broad tail of regional and specialty suppliers serve niche and research markets. Our report includes company-level assessments for the principal manufacturers and distributors shaping the market:

- Fengchen Group Co., Ltd. (China) — A vertically integrated supplier offering pharmacopeial grades geared to peptide synthesis and intermediates; strength lies in scale and established export channels.

- Hangzhou Leap Chem Co., Ltd. (China) — A producer focused on custom and wholesale volumes for research and industrial peptide work; competitive on flexible lot sizes and rapid lead times.

- Wuhan Fortuna Chemical Co., Ltd. (China) — Bulk and wholesale supplier with an emphasis on industrial‑scale feedstock for chemical synthesis.

- Central Drug House (CDH) (India) — ISO‑certified manufacturer and exporter serving laboratory and fine‑chemical applications with an established regulatory positioning.

- BLD Pharmatech (China) — Supplier of high‑purity grades distributed through global reagent platforms; useful partner for clients seeking catalog availability and traceability.

- Chem‑Impex International and Peptide.com (AAPPTec) (USA) — Distribution and specialty‑reagent channels focused on North American research customers who prioritize lot-to-lot consistency and technical support.

- TCI Chemicals (Japan) and Biosynth (Switzerland/UK) — Regional leaders providing research-grade materials, with strong presence in academic and pharmaceutical R&D pipelines.

- Sinochem Nanjing Corporation (China) — A supplier that emphasizes industrial and research uses with robust quality protocols and exporting capacity.

Taken together, the landscape favors suppliers that combine certified quality, geographic reach and the ability to manage upstream feedstock risk. The market concentration metrics reflect a balance between incumbent scale and competitive pressures from regional specialists—a structure that rewards distributors and manufacturers who can offer both consistency and responsive service.

Strategic playbook for corporate leaders in 2026

Based on our analysis, advanced buyers and investors should prioritize five interlocking strategic moves in 2026:

- Reframe contracts around feedstock exposure: incorporate index-linked pricing corridors or capped escalation mechanisms tied to L‑Leucine benchmarks to buffer procurement from sharp upstream swings.

- Segment suppliers by role: designate anchor suppliers for volume continuity, specialty partners for high‑purity/regulated lots, and catalog distributors for rapid‑turn small‑lot needs—ensuring each role has explicit KPIs and penalty/reward clauses.

- Invest in near-term quality audits: allocate technical resources to audit key suppliers’ quality management and sterility/traceability controls to de‑risk the pipeline for clinical and commercial manufacturing.

- Explore backward integration selectively: for firms with sustained volume growth plans, evaluate co‑investment in upstream fermentation or toll‑manufacturing capacity to secure feedstock and realize margin capture.

- Build logistics resilience: diversify transport lanes, increase safety stock for critical intermediates, and negotiate vendor‑managed inventory arrangements for fast‑moving SKUs to reduce lead‑time variability.

Scenario thinking and what to model in 2026

The report provides scenario models that translate quantifiable shocks into P&L and operational outcomes. Three scenarios deserve board-level attention:

- Base‑case (steady growth): Assumes demand growth consistent with the 7.45% CAGR and normal supply churn—useful for budgeting and mid‑term capacity planning.

- Price‑shock (raw‑material squeeze): Models the impact of sustained L‑Leucine price increases and logistics bottlenecks on gross margins and working capital needs—useful for procurement restructuring and hedging strategies.

- Quality/regulatory uplift: Captures the incremental cost and time-to-market effects of stricter regulatory expectations for pharma‑grade intermediates—useful for assessing the ROI of supplier quality investments and internal QA expansion.

How PW Consulting supports execution

Beyond the report, PW Consulting offers a suite of execution services to translate strategy into results:

- Supplier due diligence and audit programs tailored to Boc‑protected intermediates;

- Negotiation support for index‑linked contracts and capacity reservation agreements;

- Technical benchmarking to align specification language between buyers and suppliers; and

- Financial modelling to evaluate backward integration and contract manufacturing partnerships under multiple price and demand scenarios.

Final note — what you won’t find here (and why)

This release is deliberately structured as a strategic preview: it presents macro market sizing, growth trajectory and the operational levers that will matter in 2026 while withholding the granular segment-level allocations and company revenue-by-segment figures that are included in the full PW Consulting report. Those detailed splits are essential for contract-level negotiations and investment underwriting; they are available in the complete dataset and appendices that accompany the full study.

Next steps

If your 2026 priorities include securing supply for peptide programs, optimizing procurement against volatile upstream inputs, or assessing acquisition targets in the Boc‑intermediate space, PW Consulting’s full Boc‑L‑Leucine Market Report and bespoke advisory services will provide the detailed segmentation, supplier revenue models and contract playbooks necessary to act with confidence. Contact our market team to request the full report package and to schedule a tailored briefing.

For detailed analysis of this topic, please visit the official page:Boc L Leucine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com