The Transformative Role Of Advanced Logical Data Integration In Modern Business Enterprises

Other |

2026-06-04 11:03:01

As airlines, OEMs and electrification suppliers prepare capital and product roadmaps for 2026, the in-seat power systems market for commercial aircraft has moved from niche amenity to core cabin infrastructure. Our latest market study — Commercial Aircraft In Seat Power System Market — synthesizes historical performance (2020–2025), delivers a seven-year forecast (2026–2032), and combines quantitative scenarios with operational playbooks for procurement, linefit vs retrofit economics, and certification planning.

Commercial Aircraft In Seat Power System Market

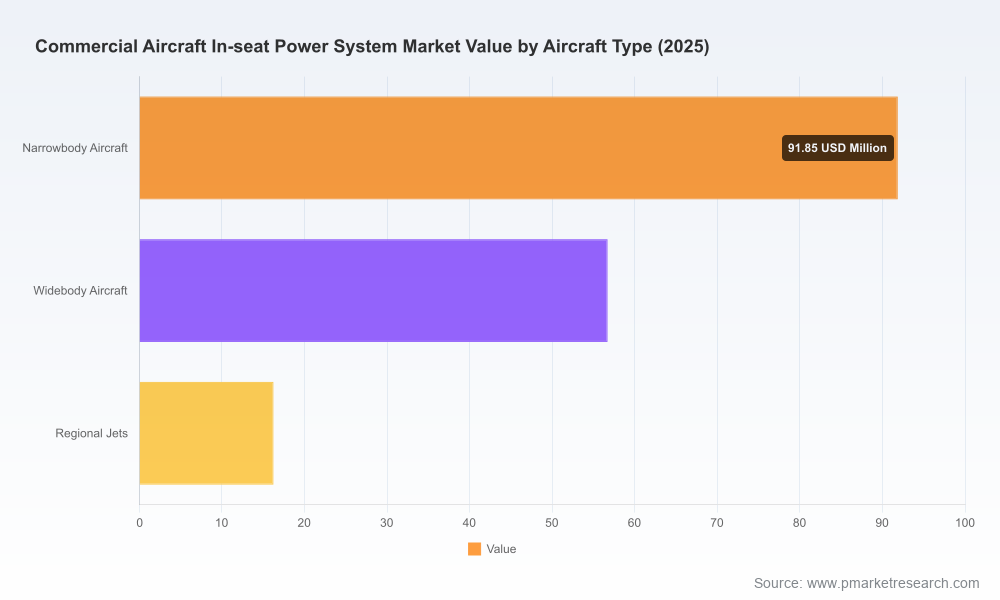

At the macro level, the market shows renewed momentum after pandemic-era disruptions, reaching an estimated USD 164.8 million in 2025 and projected to grow to approximately USD 173.4 million in 2026 on a compound annual growth rate (CAGR) of 4.85% through the forecast window. Our central scenario forecasts continued, structurally driven growth toward a multi-hundred-million dollar market by 2032. That trajectory signals both steady demand for replacement and retrofit programs and expanding line-fit requirements as USB-C and high-power delivery become standard passenger expectations.

Commercial Aircraft In Seat Power System Market

Decision-focused: Designed for airlines’ fleet planners, MRO and retrofit program managers, OEM procurement teams, and tier-1 cabin systems suppliers, the report translates market projections into investment choices and timing signals.

Commercial Aircraft In Seat Power System Market

Actionable scenarios: We present three pragmatic scenarios—Consolidation, Acceleration, and Fragmentation—each tied to OEM production rates, retrofit cycles, regulatory adoption of USB-C standards, and component supply constraints. For each scenario we quantify implications for procurement lead times, aftermarket demand, and pricing pressure.

Risk and resilience lens: The study integrates supply-chain constraints (notably high-grade copper availability and higher-voltage distribution adoption) and regulatory direction (universal USB-C ambitions, fuel-efficiency mandates) to build resilient sourcing and design strategies.

Competitive context and supplier playbook: The report distills supplier capabilities, certification footprints, and integration experience across the market’s leading providers—helping buyers shortlist vendors on technical, cost, and program-risk dimensions.

USB-C normalization: Regulators and industry bodies are converging on USB-C as a standard. This ushers in a near-term upgrade cycle for fleets that previously offered lower-power USB-A or legacy AC outlets. Operators must weigh unit cost against passenger satisfaction and ancillary revenue trade-offs.

Higher-power, lighter architectures: Demand for 60–100W device charging, coupled with fuel-efficiency mandates, is prompting suppliers to adopt higher-voltage distribution and slimline converters that reduce wiring mass and cavity space. Our analysis shows design choices now directly affect aircraft weight budgets and certification pathways.

Supply-chain adaptation: Copper shortages and higher raw-material costs have already driven innovation: alternative distribution topologies can cut conductive material usage by roughly 20% while maintaining power delivery — a material consideration for program managers setting 2026 procurement specifications.

BYOD and baseline expectations: Bring-Your-Own-Device behavior has made seat-level power a baseline expectation on a growing share of routes. What was once a premium differentiator has become an operational standard, shifting pricing dynamics and aftermarket replacement cycles.

The market exhibits moderate concentration: the top three suppliers account for a significant share of revenues, and the top five approach roughly two-thirds of the commercial value pool. That concentration has strategic implications for negotiation leverage, risk of single-source exposure, and the speed with which new standards propagate through fleets.

Astronics Corporation (East Aurora, NY) remains a leading provider of in-seat power solutions. Its EmPower family, including the award-winning UltraLite G2 and a recent EmPower 1327-27 dual USB-C outlet introduced in April 2026, positions Astronics strongly across both linefit and retrofit programs. The company’s broad OEM relationships and certification portfolio make it a frequent first-choice for system integrators.

KID-Systeme GmbH (Buxtehude, Germany) brings deep cabin-electronics integration capability. Its profile emphasizes bespoke in-seat power, connectivity, and cabin systems—relevant to operators prioritizing tailored cabin experiences and close seat-manufacturer integration.

Collins Aerospace (RTX) (Charlotte, NC) pairs power delivery with data-port and IFE integration—an important differentiator for operators seeking consolidated cabin system contracts that reduce interface risk.

Burrana Pty Ltd (Cannon Hill, Australia) is active in the narrowbody segment with its RISE cabin technology. Recent product positioning at AIX 2026 underscores Burrana’s push to present in-seat power as part of broader cabin modernization platforms, attractive for retrofit bundling opportunities.

IFPL Group (Isle of Wight, UK) combines volume manufacturing scale with product breadth—over three million units shipped—and brand longevity, underscored by its 30th anniversary showcase at AIX 2026.

Mid-Continent Instrument Co. (True Blue Power) (Wichita, KS) and Astrodyne TDI (Hackettstown, NJ) play important roles in delivering certified USB power modules, converters and EMI management components, particularly for operators focused on TSO/ETSO compliance and retrofit safety cases.

Panasonic Avionics (Lake Forest, CA) is notable for deeply integrating high-power USB-C delivery into its IFE platforms—recently entering service with a major carrier—which is relevant to airlines evaluating bundled IFE-plus-power strategies to simplify retrofit logistics.

Astronics launched a dual USB-C in-seat outlet in April 2026 and earlier won industry recognition for its UltraLite G2 product family—moves that reinforce its competitive positioning in both retrofit and linefit opportunities.

Burrana and IFPL used AIX 2026 to restate product roadmaps and market positioning, signaling intensified competition in the narrowbody retrofit corridor during 2026–2028.

Panasonic’s integration of up to 67W USB-C in live service highlights the feasibility of high-power cabin deployments at scale and sets a service-readiness benchmark that other vendors and airlines will evaluate for their fleets.

Comprehensive market sizing and forecast (2020–2032) with base year analysis and scenario modelling to stress-test procurement timelines and capex planning.

Segment-level sizing and growth drivers (by seating class, aircraft type and region) presented together with a confidence matrix. Note: the public brief intentionally withholds detailed subsegment tables—access to the full dataset is available through our subscription portal for procurement/commercial teams requiring vendor-level granularity.

Supplier capability matrix including certification footprints, linefit/retrofit experience, unit economics, and recommended negotiation levers for 2026 sourcing rounds.

Retrofit vs. linefit decision framework: total cost of ownership (TCO) templates, break-even calculators, lead-time maps, and MRO integration checklists.

Technical design guide: power architecture options (centralized vs. distributed), EMI mitigation practices, weight and cavity-space tradeoffs, and a compliance checklist aligned to current regulatory expectations.

Implementation playbook: step-by-step operating model for program rollout, supplier audits, spares provisioning, and aftermarket support contracts optimized for 2026 timelines.

Prioritize modular, standard-based designs: Move toward USB-C universal interfaces in new purchases and retrofit scopes to minimize future rework and to align with regulatory direction. Specify power delivery tiers (e.g., baseline vs. high-power) and require backward-compatible firmware/firmware update pathways.

Adopt a hybrid sourcing strategy: Combine the scale and certification maturity of large incumbents with the specialized capabilities of niche suppliers for rapid integration. Use pilot retrofit programs to validate supplier interfaces before fleet-wide rollouts.

Build supply-chain resiliency clauses: Given material constraints, include alternative-material acceptance criteria, multi-sourcing options for critical components (converters, cables, EMI filters), and inventory hedging for long-lead items.

Embed weight and cavity metrics into procurement KPIs: Require supplier-provided delta weight and cavity-space impact analyses as part of technical bids to ensure alignment with fuel-efficiency mandates.

Plan for mixed-fleet serviceability: Create spare-part and training pools that support multiple vendor platforms, focusing on maintenance commonality to reduce MRO complexity and downtime.

We combine quantitative market models with hands-on program playbooks and supplier negotiation tools. Our deliverables include spreadsheet-ready TCO models, retrofit scheduling matrices tied to maintenance events, and vendor shortlists aligned to your technical and commercial thresholds.

For procurement directors, the report is immediately operational: it reduces vendor selection time, clarifies risk-adjusted pricing ranges, and identifies certification bottlenecks likely to affect 2026 retrofit windows. For systems engineers and product owners, the technical guidance shortens qualification timelines and helps reconcile weight/space tradeoffs in early design phases.

This press brief highlights the strategic contours of the in-seat power systems market and provides a preview of the operational intelligence contained in the full report. To access the complete market dataset, segment breakdowns, vendor scorecards and downloadable TCO tools, please visit our official report page or contact PW Consulting’s Commercial Aircraft team for a tailored briefing.

In a market where passenger expectations and regulatory standards are accelerating change, 2026 will reward organizations that pair disciplined procurement with forward-looking technical specifications. Our study equips leaders with the market foresight and actionable steps to make those choices with confidence.

For detailed analysis of this topic, please visit the official page:Commercial Aircraft In Seat Power System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com