Revealed: The Expanding Scope of the Plastic Injection Moulding Machine Market by 2035

Other |

2026-06-12 10:48:40

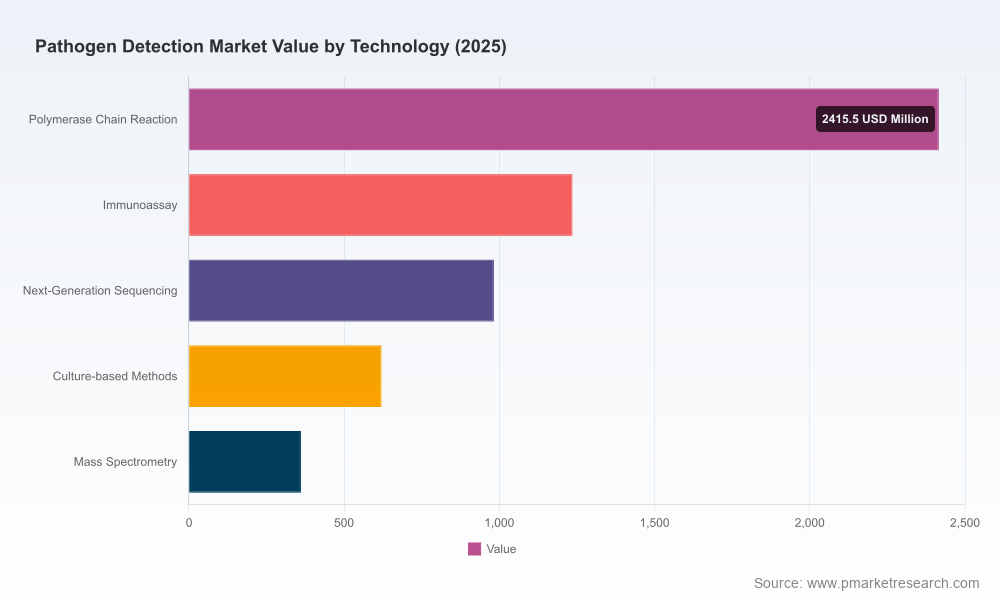

PW Consulting’s Pathogen Detection Market report (base year 2025) offers C-suite and investment teams a decision-grade perspective for actions through 2026 and beyond. The market has demonstrated a robust recovery and expansion trajectory from 2020–2025, reaching an estimated USD 5,615 Million in 2025 and continuing to grow at a compound annual growth rate (CAGR) of 7.8% through our 2026–2032 forecast horizon. Under our base forecast the market is projected to approach approximately USD 9,500 Million by 2032, underscoring sustained opportunity across molecular, immunoassay and emerging sequencing approaches.

Pathogen Detection Market

Timing: 2026 is a pivotal year in which reimbursement clarity, regulatory momentum and supply-chain normalization converge to shape platform adoption and procurement cycles. Companies that align regulatory filings, commercial partnerships and supply guarantees in 1H–2H 2026 will capture disproportionate share of near-term demand.

Pathogen Detection Market

Value creation: The market’s mid- to long-term expansion (7.8% CAGR) means incremental revenue is predictable, but margin and competitive advantage will be set by assay breadth, automation, and service models rather than merely instrument sales. Strategic choices made in 2026 about product portfolio focus and channel design will materially affect five-year profitability.

Pathogen Detection Market

Risk-reward: Industry-level concentration metrics (CR3 ~38%; CR5 ~52%) indicate a market where a handful of established players exercise meaningful influence but where significant white space remains for focused entrants and fast-follower strategies, especially in specialized applications and low-resource settings.

PW Consulting’s offering is built for activation. Beyond narrative, the study supplies:

Financial-grade market models (historical 2020–2025 and forecast 2026–2032) with scenario toggles for adoption speed, reimbursement shifts and reagent-cost inflation;

Go-to-market playbooks differentiated by end-user segment (hospital labs, point-of-care, food safety, pharmaceutical QC, and low-resource programs), including contract structures, channel economics and sample workflows;

Vendor scorecards and strategic options (organic R&D vs. bolt-on M&A) that synthesize technical differentiation, regulatory footprint and commercial reach for the leading competitors;

Regulatory and reimbursement maps tied to action calendars — highlighting windows for CLIA-waiver submissions, CE/IVD clearances and national procurement cycles;

Supply-chain and cost-pressure assessments with mitigations (multi-sourcing strategies, buffer inventory thresholds, reagent-substitution roadmaps) calibrated across likely demand scenarios;

Investor and M&A screening criteria with targets prioritized by technology fit, margin profile and geographic access — all linked to modeled impact on combined pro-forma revenues and synergies.

To uphold the “trailer” principle and preserve the efficacy of our dataset for subscribers, the report demonstrates the analytical approach and overall market size path but omits public disclosure of granular region/application shares and per-segment dollar tables in this summary. Those detailed segmentation matrices and downloadable models are available in the full report.

The pathogen-detection landscape blends large diagnostics incumbents, specialized molecular players and a set of nimble innovators focused on point-of-care and syndromic panels. The competitive posture of the top vendors reflects differentiated bets across platform architecture, assay content and channel execution.

Large systems vendors (examples include established players with broad instrument and assay ecosystems) benefit from installed-base economics and integrated reagent streams. Their strategic priorities in 2026 will be sustaining assay pipelines and defending consumable economics while expanding point-of-care credentials where permissible.

Mid-sized and niche innovators (companies focused on isothermal methods, high-multiplex consumables or rapid transcription-mediated amplification) can capture pockets of high-margin volume by specializing in distinct workflows, faster time-to-result or lower-cost per test in targeted channels.

New entrants and platform-agnostic assay developers are leveraging partnerships and distribution agreements to accelerate access without heavy capital expenditure. Careful structuring of these alliances will determine whether they achieve meaningful penetration or remain marginal suppliers.

Recent market moves reinforce these dynamics. Notable events in 2025–2026 include an FDA 510(k) clearance for a new BV assay on a cartridge-based platform, launches of multiplex respiratory panels that bundle emerging pathogens, point-of-care CE-IVD approvals for influenza/RSV triage tests, and distribution agreements that expand hospital access for rapid molecular platforms. Positive clinical validations for enhanced sensitivity in enteric panels and strategic distribution partnerships underscore how near-term regulatory and commercial wins translate directly into adoption acceleration.

Regulatory gating: Regulatory pathways that enable CLIA-waived or point-of-care designations materially expand the addressable market. Firms with prioritized submissions and robust human factors data packages should secure outsized share of decentralized testing growth in 2026.

Reimbursement shifts: Recent updates to coding and payment frameworks have improved economics for certain respiratory and infectious-disease tests. Companies should align clinical evidence generation to reimbursement milestones to unlock higher-margin volumes.

Raw-material cost pressure: The industry continues to face upward pressure on medical-grade reagents and consumables. Expect mid-teens cost inflation in certain reagent and plastics categories unless supply contracts or alternative sourcing strategies are implemented. Successful players in 2026 will have secured multi-year supply agreements or modularized consumable designs to reduce exposure.

Global access programs: The WHO’s expanded prequalification footprints for rapid pathogen tests have opened procurement channels in low-resource markets. Suppliers that tailor product configurations and distribution partnerships to meet these procurement terms will benefit from accelerated public-sector adoption.

For executives and investors mapping strategy in 2026, PW Consulting highlights five pragmatic priorities:

Prioritize platform modularity and assay breadth: Invest in multiplexing and modular consumable designs to capture recurring reagent revenue while enabling quick assay updates for emerging pathogens.

Lock in supply resilience: Negotiate multi-year reagent and plastics contracts with tiered pricing and capacity commitments; consider strategic inventory and nearshoring to blunt cost volatility.

Align clinical evidence to reimbursement windows: Sequence clinical trials and real-world evidence generation to coincide with coding and payment updates to maximize realized ARPU per test.

Go-to-market segmentation: Differentiate channel strategies — strengthen hospital lab partnerships for high-throughput assays, while pursuing CLIA-waiver and CE-mark pathways to capture decentralized point-of-care demand.

M&A and partnership discipline: Target bolt-on acquisitions that either extend assay content into underpenetrated applications or provide low-cost manufacturing capability. Use our M&A screening criteria to prioritize targets that deliver immediate consumable synergies and improve margin profiles.

Subscribers receive an action pack: a downloadable financial model (scenario-enabled), competitive heatmaps, regulatory submission calendars, a supply-chain risk matrix, and transaction playbooks including valuation benchmarks. These tools are designed to convert market insight into executable 90- to 180-day plans that materially de-risk strategy and speed time-to-value.

This preview highlights the strategic contours of the pathogen detection market and the levers that will determine winners in 2026. For the complete segmentation matrices, company-by-company scorecards, downloadable models and the full set of tactical recommendations, visit PW Consulting’s report page or contact our industry team. The full dataset will enable your organization to stress-test strategic options, prioritize investments and align regulatory and commercial calendars for maximal impact.

For detailed analysis of this topic, please visit the official page:Pathogen Detection Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com