Financial Literacy Market Digital Learning Expansion

Networking |

2026-02-26 08:03:14

PW Consulting’s latest 44 Diphenylmethane Diisocyanate Market report (base year 2025) confirms a resilient, mid-single-digit growth trajectory for MDI through the coming decade. The global market is estimated at USD 11,450 Million in 2025 and is forecast to expand to approximately USD 16,306 Million by 2032, reflecting a compound annual growth rate (CAGR) of 5.18% over the 2026–2032 period. This trajectory masks a complex set of structural dynamics—feedstock volatility, regulatory headwinds in developed markets, and ongoing industrial consolidation—that will shape supplier strategies, capital allocation and commercial tactics in 2026.

44 Diphenylmethane Diisocyanate Market

Investment timing and capacity planning: A steady market expansion at ~5% CAGR supports continued rational capacity additions, but exposes new projects to feedstock cost and regulatory timing risk. Firms contemplating greenfield or debottlenecking projects need scenario-led IRR analysis that integrates both commodity cycles and compliance-related lead times.

44 Diphenylmethane Diisocyanate Market

Pricing and contract design: Recent supplier-led price adjustments and feedstock-driven cost pressure (notably aniline) emphasize the need for flexible contracting, indexation mechanisms and active risk-sharing clauses with key polyurethane customers.

44 Diphenylmethane Diisocyanate Market

M&A and portfolio repositioning: The market’s concentration profile—where a small group of global players account for the majority of volumes—continues to increase strategic value of bolt-on acquisitions and of entering adjacencies (specialty MDI grades, formulation services, downstream captive capacity).

Demand fundamentals remain underpinned by building insulation, appliance efficiencies and mobility applications that continue to consume polyurethane systems. However, the near-term supply equation is being reshaped by two forces. First, feedstock volatility—aniline price steps observed through late 2025 and into 2026 have materially elevated unit production costs at scale. Second, active pricing actions from leading producers have demonstrated an ability to pass through at least part of those cost increases, though the elasticity of downstream demand varies by application and region.

For buyers, these twin forces imply that procurement strategies should shift from single-period spot buying to multi-layered hedging and integrated supplier partnerships. For producers, the window for margin recovery is open but contingent on disciplined allocation of volumes and careful sequencing of contractual rollovers to avoid downstream demand erosion.

The regulatory environment is increasingly consequential. Notable recent policy steps include preliminary trade remedy actions affecting imports in important markets and targeted health-based assessments that focus on unreacted MDI in end-use systems. These developments raise compliance, trade policy and disclosure obligations for both producers and formulators. Companies must accelerate regulatory scenario planning, invest in product stewardship and tighten traceability across supply chains to avoid enforcement, liability and off-take disruption.

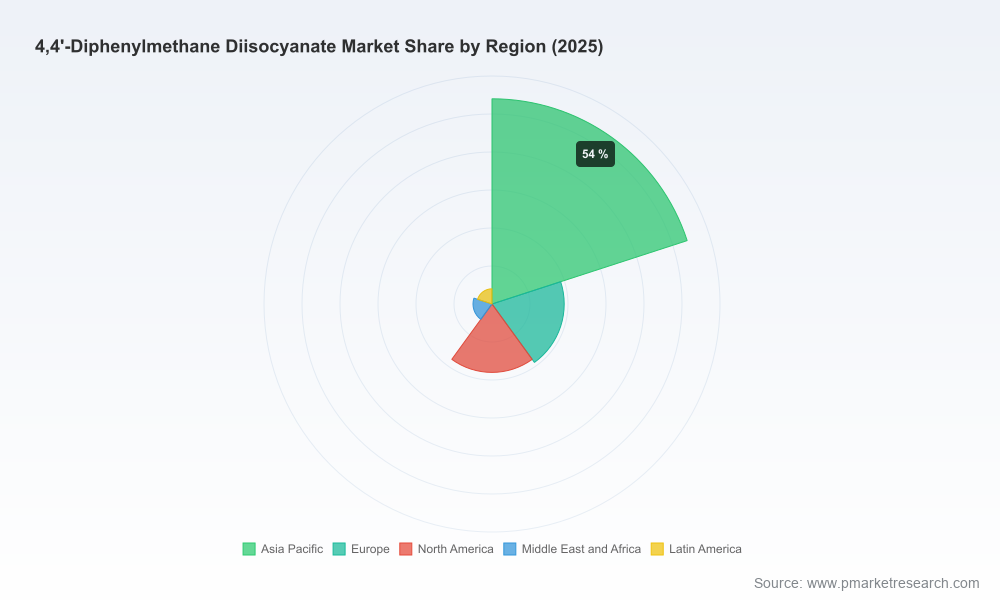

The global 4,4'-MDI market remains concentrated, with the top three producers holding a dominant share and the top five controlling a very large majority. This structure shapes competitive choices:

Scale players (vertical integration and cost leadership): Large integrated producers with global plants and backward feedstock access can manage cyclical margin pressure better and deploy pricing actions quickly. Recent industry pricing behavior shows these firms’ capacity to influence short- to mid-term pricing dynamics.

Specialty differentiators (quality, sustainability, formulation support): Firms focusing on high-purity grades, specialty functionalities, or sustainability-linked product lines are carving out insulated niches that are less price-sensitive but require higher technical service investment.

Regional challengers and supply chain arbitrage: Localized production hubs remain important for certain value chains where logistics and regulatory exposure penalize long-range supply. Trade measures and regional regulatory divergence will make regional footprint strategy a live issue for 2026.

Our competitive profiles in the report dissect the strategic positioning of leading players—highlighting global integrated producers, specialty-focused firms, and regional champions—mapping their asset footprints, portfolio tilts and recent commercial actions. That analysis is essential for bidders, partners and investors considering any transaction or long-term supply agreement in 2026.

Supplier pricing behavior: Major producers implemented staged price increases across 2025–2026. These moves reveal a willingness to defend margins and to coordinate commercially where feedstock pressures are persistent. For buyers, this requires contingency in procurement and stronger pass-through clauses in downstream contracts.

Feedstock cost creep: Regional aniline pricing trends have moved materially higher in early 2026 versus late 2025, driven by benzene-related dynamics and robust demand for MDI. This highlights the necessity for feedstock risk models in every production-capex appraisal.

Regulatory actions: Trade-litigation and targeted safety determinations in high-value markets add timing and execution risk to exports and to product development pipelines, especially for spray-applied systems. Proactive regulatory engagement and reformulation capability are no longer optional.

Supplier resilience playbook: Establish multi-sourcing arrangements, longer-term offtake with indexed pricing, and joint working-capital mechanisms with strategic suppliers. Shadow-price scenarios should be part of every procurement RFx for PU system customers.

CapEx and timing discipline: Defer commodity-exposed greenfield investments unless accompanied by secured-feedstock agreements or offtake contracts. Prioritize projects that deliver optionality (e.g., debottlenecking with modular expansion capability) and lower lead-time.

Product and service differentiation: Invest in higher-margin specialty MDI grades, formulation support services, and sustainability certifications that meet downstream OEM and regulatory demands. Technical service capability can be a durable margin lever.

Regulatory readiness: Accelerate product stewardship, implement robust residual-MDI testing and documentation in spray polyurethane systems, and develop mitigation plans for markets with evolving restrictions.

M&A and portfolio actions: For mid-sized players, consider bolt-ons that add specialty grades or regional logistics capability. For large firms, evaluate divestitures of non-core assets to free capital for sustainability-linked upgrades and digitalization.

This report is built for 2026 decision calendars. It goes beyond topline forecasts to provide:

Actionable scenario models that combine demand elasticity by end-use with supplier concentration and feedstock-price shock pathways.

Commercial playbooks and contracting templates to capture upside or protect margins during price volatility periods.

Regulatory impact matrices that translate policy changes into financial and operational exposures by market and by product family.

A competitive intelligence suite profiling capex pipelines, recent price moves and strategic initiatives from the major players, enabling rapid benchmarking and counter-strategy design.

Detailed regional and application segmentation datasets, price curves and supply/demand balances—with user-configurable inputs for custom scenario testing.

Importantly, the report intentionally refrains from publishing certain granular segment-level exposures in public summaries; those detailed tables and model workbooks are provided to licensed report subscribers and discussion clients. This “teaser” approach is designed to deliver strategic insight in public form while reserving the transaction-grade granularity for engaged partners.

C-suite and corporate development teams: Use the concentration and pricing context to prioritize M&A screening and to recalibrate ROI thresholds for commodity versus specialty investments.

Procurement and commercial teams: Rework sourcing and pricing playbooks, operationalize indexation clauses, and pilot alternative feedstock contracts linked to benzene/aniline hedges.

R&D and product compliance: Accelerate development of lower-residual MDI systems, and ensure documentation and testing protocols meet the latest regulatory expectations in major end markets.

Investors and lenders: Apply the report’s scenario outputs to stress-test downside commodity cycles and to identify sponsors with sustainable margin insulation strategies.

For teams making capital, procurement or M&A decisions in 2026, the difference between a resilient outcome and an avoidable setback will be in the granularity of market intelligence and the quality of scenario-stress testing. PW Consulting’s full 44 Diphenylmethane Diisocyanate Market report contains the detailed segment-level datasets, company scorecards, and downloadable model workbooks that enable transaction-grade analysis and contract negotiation support.

Contact PW Consulting to request the full report package, licensing options for the model workbooks, or a tailored executive briefing. Our advisory team can translate the report’s insights into a short, targeted action plan aligned to your organization’s risk appetite and strategic horizon for 2026.

For detailed analysis of this topic, please visit the official page:44 Diphenylmethane Diisocyanate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com