Rare Earth Metals Market to Reach USD 30.9 Billion Amid Rising Demand from Clean Energy, Electric Vehicles, and Advanced Electronics

Other |

2026-06-10 10:04:20

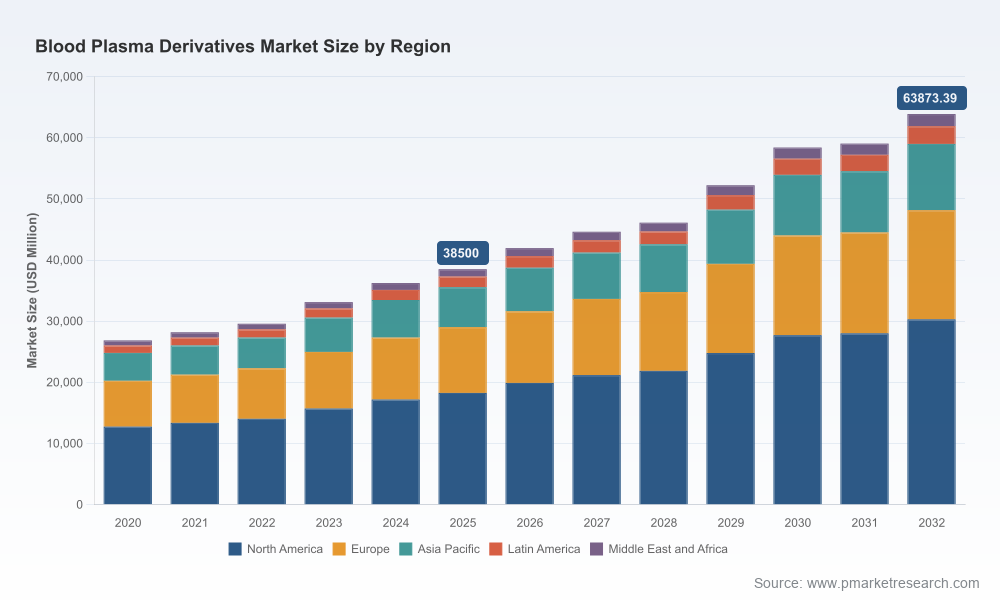

PW Consulting’s upcoming Blood Plasma Derivatives Market report (base year 2025) delivers an actionable strategic roadmap for executives planning through 2026 and beyond. After a steady expansion across 2020–2025, the market reached an estimated USD 38,500 Million in 2025 and our forward model projects continued momentum across the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 7.5%. By the end of the forecast horizon, the market dynamics we model indicate a materially larger addressable market, reflecting both demand expansion and structural reconfiguration across supply chains and manufacturing footprints.

Blood Plasma Derivatives Market

Demand-supply tightness is persistent. Manufacturing lead times for plasma-derived therapeutics and the intrinsic lag between collection and finished product (commonly measured in many months) mean that short-term imbalances can cascade into multi-quarter shortages. Companies that move early to shore up access to plasma, shorten conversion timelines, or expand flexible fractionation will materially alter competitive positioning.

Blood Plasma Derivatives Market

Regulatory and reimbursement regimes are increasing operational complexity. Standards from major regulators enforce rigorous safety and traceability requirements across collection and fractionation, which raises the bar for new entrants and elevates the importance of regulatory program management in site expansion and M&A.

Blood Plasma Derivatives Market

Concentration creates both risk and opportunity. The market remains concentrated among a small group of leaders, which creates predictable procurement dynamics but also amplifies system-wide vulnerability to facility outages, capacity shifts, or strategic investment cycles.

This is not a high-level academic exercise. The report is designed as an executive toolbox for 2026 decision-making: it combines an integrated market-sizing engine, scenario-driven demand-supply models, and an operational playbook that translates strategic choices into measurable KPIs. Key decision-use cases include capacity planning and timing, M&A and JV screening, supplier and geographic diversification strategies, pricing and reimbursement scenarios, and go-to-market sequencing for new plasma-derived indications.

Transparent market model: historical time series (2020–2025) and a detailed forecast (2026–2032) with adjustable assumptions for plasma availability, production yields, and pricing.

Scenario suite: stress tests for supply shocks, regulatory delays, and accelerated adoption of non-plasma alternatives; each scenario includes revenue, margin, and working capital implications.

Concentration and competitive maps: measures of market concentration and power dynamics that inform negotiation posture, pricing strategies, and partnership targets.

Operational playbooks: facility siting scorecards, CAPEX sizing templates, production ramp timelines, and plasma sourcing due-diligence checklists suitable for integration into investment memos.

Commercial execution guides: product positioning matrices, payer engagement frameworks, and patient-access program templates tailored to varying reimbursement environments.

Acquisition and partnership heatmaps: prioritized targets, integration risk scoring, and modeled transaction synergies calibrated to the plasma-derivatives value chain.

The market’s competitive fabric is shaped by integrated players that combine plasma collection networks with large-scale fractionation and global distribution. The report profiles incumbent leaders and fast-scaling specialists, assessing their strategic intents and operational postures:

Grifols — a vertically integrated producer with a broad product slate and ongoing European capacity expansion plans aimed at improving regional supply resilience.

CSL Behring — a global leader investing in large-scale manufacturing modernization and automation to reduce unit costs and improve throughput, while pursuing facility expansions in core markets.

Takeda — a diversified pharmaceutical player that couples plasma-derived portfolios with broader rare-disease assets and targeted manufacturing investments to support specialty product launches.

Octapharma — focused on manufacturing scale-up and operational enhancements to meet growing demand for immunoglobulins and coagulation factors across multiple regions.

Kedrion, BPL, LFB, Biotest, Sanquin, SK Plasma — a mix of regional champions and specialized manufacturers whose strategic moves (capacity upgrades, partnership activity, and selective market entry) materially affect regional supply dynamics.

Recent industry activity underscores two themes: incumbents are accelerating capital investments to expand and modernize fractionation capacity, and several players are optimizing for automation and sustainability in new facilities. These shifts compress time-to-market for capacity expansions and change the calculus for both brownfield expansions and greenfield site selection.

Our forecasting engine embeds sensitivity levers that matter to executives in 2026:

Plasma availability: scenarios model a range from stable collection volumes to protracted constraints; even modest deviations materially affect capacity utilization and near-term pricing power.

Regulatory timelines: acceleration or delay in approvals for facilities and product variations can shift break-even horizons and influence whether an internal expansion or strategic partnership is the better route.

Technology and manufacturing yield improvements: incremental gains in downstream yield or automation can offset a significant portion of raw-material supply pressure and shorten investment payback periods.

Commercial reimbursement shifts: payers’ willingness to reimburse high-cost therapies influences market penetration curves, with asymmetric effects across geographies.

Secure access to plasma upstream. Negotiate long-term supply agreements with diversified collection partners, and evaluate off-take structures that include quality and traceability covenants.

Prioritize modular, flexible capacity. Invest in fractionation that supports multiple product families and allows rapid reallocation of throughput to respond to demand shocks.

De-risk regulatory pathways early. Integrate regulatory strategy into site-selection and capex planning to avoid costly post-commissioning delays.

Use M&A selectively to acquire concentrated capabilities—either incremental capacity or specialized product lines—while ensuring cultural and process compatibility to limit integration risk.

Engage payers and policymakers. Shape reimbursement models and national self-sufficiency initiatives through evidence-based value dossiers and public-private dialogues.

The report includes a risk taxonomy that maps likelihood and impact across operational, regulatory, supply-chain, and commercial axes, and prescribes mitigation levers—inventory strategy, multi-sourcing, contract design, and capital allocation trade-offs—tailored to organizational risk appetite and balance-sheet capacity.

This preview demonstrates our analytical depth and pragmatic orientation: we disclose market-scale trends, growth trajectory, concentration dynamics, and the kinds of operational tools buyers need to execute. In keeping with the “preview” principle, we intentionally withhold certain granular segmentation figures and the full data annex so decision-makers are encouraged to consult the complete report for transaction-ready numbers, regional and application-level forecasts, and the detailed financial templates that underpin our recommendations.

Week 1–2: Executive team workshop—align on demand scenarios and strategic objectives using our scenario dashboard.

Week 3–6: Execute tactical actions—initiate supplier negotiations, launch regulatory gap assessments, and size potential capital projects using our templates.

Week 7–12: Transaction and implementation—use our M&A heatmap and integration playbook to pursue partnerships or greenfield/brownfield investments with validated ROI cases.

PW Consulting’s full Blood Plasma Derivatives Market report provides the complete dataset, regional and application-level forecasts, and executable templates required for confident decision-making in 2026. For access to the full analysis, the detailed financial models, and bespoke advisory engagements, please visit the PW Consulting reports page to download the complete report or contact our strategy team to arrange a briefing tailored to your organization’s priorities.

For detailed analysis of this topic, please visit the official page:Blood Plasma Derivatives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com