Solder Materials Market Valued at US$ 1,477.2 Million in 2019 Set to Reach US$ 2,255.3 Million by 2030

Other |

2026-03-02 11:43:38

PW Consulting today publishes a focused industry brief built from our full Cerebrovascular Accident (CVA) Drug Market report. As health systems, pharma executives, and investors position portfolios for 2026 and beyond, this brief explains why the CVA drug arena demands strategic recalibration now — and how our report can accelerate evidence‑based decision making. The analysis combines longitudinal market sizing, regulatory inflection points, and competitive intelligence into an actionable roadmap for near‑term moves and medium‑term plays.

Cerebrovascular Accident Drug Market

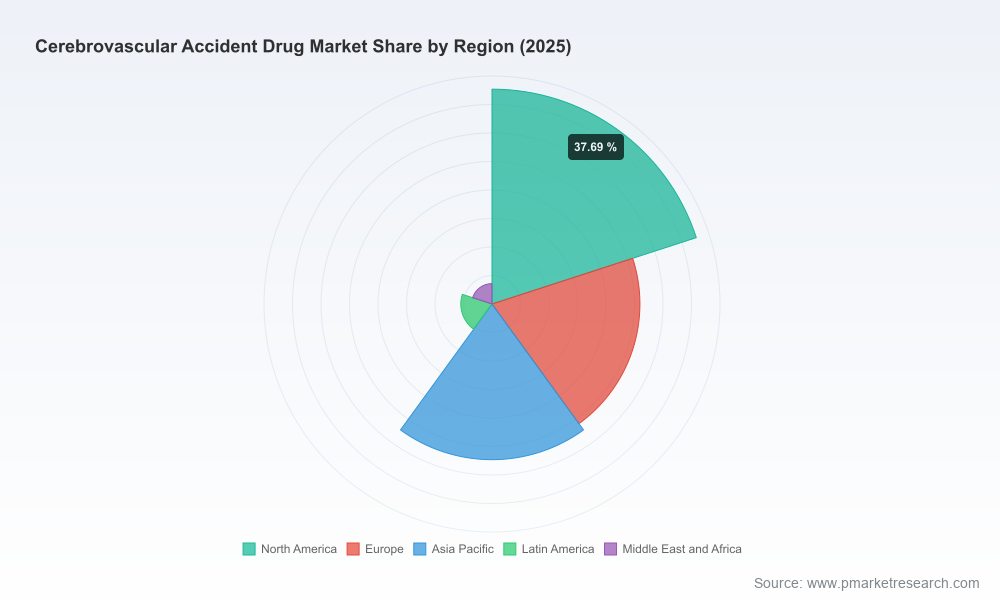

The CVA drug market is at an uncommon junction: long-standing standards of care have been disrupted by both regulatory and trial outcomes, while prevention-focused molecules are nearing late‑stage readouts that could materially change recurrent stroke dynamics. Our market model shows the overall market expanding from a mid‑decade base into the next planning horizon at a compound annual growth rate (CAGR) of 6.45% over the 2026–2032 forecast window, moving the market from an estimated USD ~16.85 billion base in 2025 toward the mid‑tens of billions by 2032. This combination of sustained growth and discrete catalytic events creates windows for market share shifts, pricing realignment, and capability investments — especially for organizations that blend clinical, regulatory and commercial expertise.

Cerebrovascular Accident Drug Market

Therapeutic re‑positioning of thrombolytics: Regulatory changes and guideline updates have altered acute stroke care workflows. The approval of tenecteplase as a single‑bolus thrombolytic and subsequent guideline endorsement has accelerated debate about first‑line thrombolytic strategy, site of care logistics and emergency medicine adoption curves.

Cerebrovascular Accident Drug Market

Shift toward secondary prevention innovations: Positive Phase 3 data in Factor XIa inhibition and other novel antithrombotic approaches signal a potential pivot from purely acute‑care spend to a larger, more sustained market for secondary prevention. That reallocation of clinical focus can compress acute therapy volumes while expanding chronic therapy revenue pools.

Consolidation and concentration: Market concentration remains meaningful — the top three and top five players control a significant share of prescription economics — creating both barriers and opportunities for new entrants depending on product differentiation and go‑to‑market partnerships.

Operational and manufacturing constraints: Thrombolytic agents reliant on biologic processes introduce capacity and supply‑chain considerations; manufacturers and contract partners must reconcile scale‑up timelines with evolving demand patterns.

Payer and hospital reimbursement context: Acute thrombolytics retain standard‑of‑care reimbursement in major systems, but payers are demanding stronger real‑world evidence for newer agents and for combinations that change length‑of‑stay or downstream resource use.

The full PW Consulting report is an operational deliverable designed for commercial teams, corporate strategy groups, BD&L desks, and private equity investors. Key features include:

Integrated market model: a multi‑scenario forecast built on historical trajectories and forward assumptions, with sensitivity toggles for adoption rates, pricing scenarios and impact of secondary‑prevention successes.

Regulatory and guideline matrix: timed mapping of approvals, label expansions and major guideline changes, with impact notes keyed to hospital protocols and reimbursement levers.

Commercial playbooks: evidence generation roadmaps, KOL engagement plans, hospital system segmentation criteria and sales force deployment scenarios tailored to product archetypes (acute thrombolytic, chronic anticoagulant, neuroprotective adjuncts).

Pipeline and competitor dossiers: strategic synopses of leading organizations with priority intel on late‑stage assets, partnerships and likely strategic responses — enabling rapid counter‑strategy development.

Deal and valuation frameworks: checklist for M&A, licensing and manufacturing alliances, with precedent transaction analysis and harmonized valuation multipliers calibrated to CVA‑specific risk factors.

Operational readiness templates: manufacturing capacity planning, clinical trial site selection heuristics for acute care studies, and regulatory submission timelines by major jurisdiction.

Executive dashboards and slide kits: executive summaries, investor decks and an interactive dataset so leadership can stress‑test scenarios in board and investor settings.

Our competitive mapping focuses on market positioning and strategic intent rather than exhaustive revenue minutiae. Several datapoints merit attention:

Genentech (Roche Group) remains central to the acute‑care conversation following the regulatory approval of tenecteplase for acute ischemic stroke in March 2025. The product’s single‑bolus administration changes emergency department workflows and is already shifting protocol discussions at stroke centers.

Boehringer Ingelheim continues to be a stalwart provider of thrombolytic therapies in territories outside certain regulatory jurisdictions, maintaining deep clinician relationships and supply expertise critical to hospital adoption.

Bristol Myers Squibb, in collaboration with Janssen, and Bayer have both pursued Factor XIa inhibitors with late‑stage success signals. Positive Phase 3 readouts for asundexian and ongoing development of milvexian embody the market’s pivot toward safer, effective secondary prevention strategies.

Large integrated pharma players — Pfizer, AstraZeneca, Johnson & Johnson, Sanofi, Daiichi Sankyo and Novartis — continue to influence the market through broad cardiovascular franchises and distribution strength, translating well for cross‑label and combination therapy positioning.

For incumbents, these developments require careful posture: defend core acute‑care revenue streams by demonstrating superior outcome and cost‑of‑care benefits for thrombolytic offerings, while allocating R&D and commercial resources to promising secondary prevention assets that can capture long‑term patient cohorts.

We translate the market’s macro trajectory and competitive moves into a short set of prioritized strategic actions for 2026 planning cycles. These are designed to be implementable within common corporate governance and budgeting timelines.

Immediate (0–12 months): Re‑baseline commercial KPIs to reflect tenecteplase adoption curves and revised guideline windows. Accelerate payer evidence generation for new thrombolytic dosing regimens and invest in hospital education programs that lower treatment delays.

Mid‑term (12–36 months): Prioritize partnerships and licensing deals to shore up secondary prevention pipelines. For manufacturers, pre‑empt supply risks by locking capacity agreements or expanding CMO options for biologics production.

Longer term (36+ months): Build or acquire capabilities in chronic care management and digital triage solutions that can capture post‑acute patient flows, supporting adherence, risk stratification and real‑world outcomes collection.

Clients who have used our full CVA dataset report that the most valuable elements are not headline market numbers but the actionable crosswalks between clinical evidence, payer models and hospital adoption economics. Our deliverables remove friction from boardroom discussions by providing:

Scenario‑ready financial models that integrate clinical adoption curves with pricing and reimbursement contingencies;

Stakeholder maps that identify the referral, emergency and specialty networks most likely to adopt new protocols;

A negotiation playbook for BD&L teams, including clauses and milestones that protect acquirers from late‑stage clinical and regulatory risk.

The CVA drug market will remain sizable and growing over the next planning cycle, but the composition of demand is shifting. Organizations that treat 2026 as a tactical baseline year — recalibrating acute therapy positioning while investing in secondary prevention and health‑system integration — will be best placed to capture disproportionate value as the market evolves. The combination of regulatory endorsements, late‑stage trial readouts, and persistent operational frictions (manufacturing and hospital logistics) creates an environment where well‑timed investments and partnerships can yield outsized returns.

PW Consulting’s full report offers the granular forecasting, competitor modeling and execution templates needed to convert strategic intent into measurable commercial outcomes. For decision makers preparing budgets and M&A priorities for 2026, our work serves as both a diagnostic and playbook — demonstrating where to defend, where to disrupt, and how to sequence resource allocation against measurable adoption milestones.

Access the full report and interactive models to review proprietary scenario outputs and competitor revenue simulations.

Request a bespoke briefing to map the findings to your portfolio and a 12‑month implementation plan.

To explore the detailed datasets, model assumptions, and the complete competitive dossiers referenced in this brief, visit the PW Consulting research portal or contact our Cerebrovascular Accident practice lead for a tailored walkthrough.

For detailed analysis of this topic, please visit the official page:Cerebrovascular Accident Drug Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com