Lithography Equipment Market: Insights and Competitive Analysis

Other |

2026-02-26 05:21:21

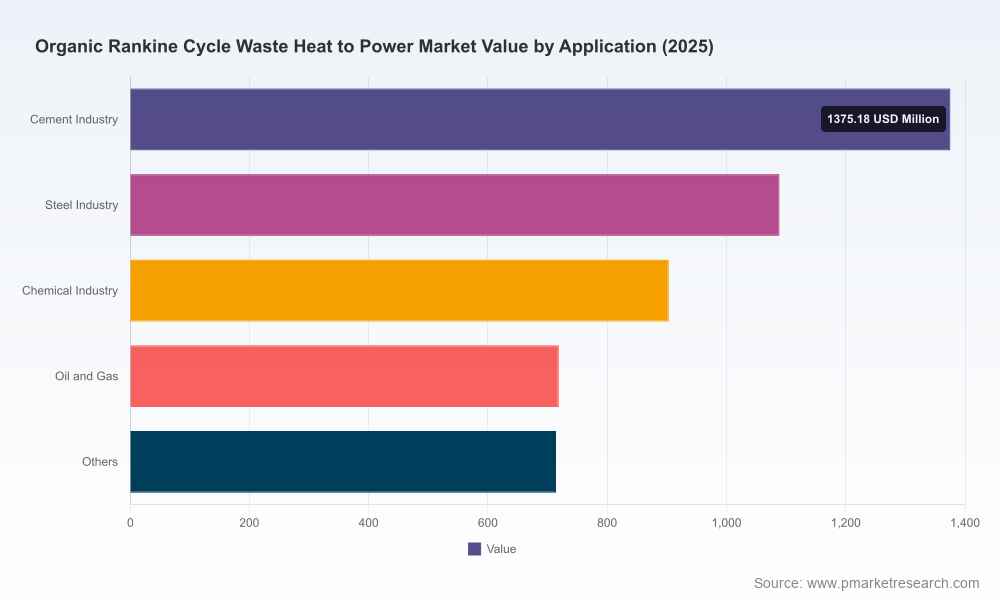

PW Consulting’s latest market study, Organic Rankine Cycle (ORC) Waste Heat to Power: Market Outlook and Strategic Playbook, uses 2025 as the base year and provides a detailed forecast for 2026–2032. Our analysis shows the market expanding at a compound annual growth rate (CAGR) of 10.65% from a 2025 base of USD 4.8 billion (USD Million units reported in the full study), approaching roughly USD 9.75 billion by 2032. This briefing highlights the report’s strategic value for corporate decision-makers preparing capital plans, product roadmaps, and M&A strategies in 2026, while intentionally preserving the granular segment tables and proprietary project-level data for subscribers of the full report.

Organic Rankine Cycle Waste Heat To Power Market

Three converging forces are driving ORC adoption into a near-term investment cycle: escalating industrial energy costs and grid volatility; regulatory pressure for industrial decarbonization and energy efficiency; and maturing technology variants that lower technical and commercial barriers to deployment. The EU’s Clean Industrial Deal and similar policy signals globally are elevating waste-heat recovery from a niche sustainability measure to a core energy-security strategy for energy-intensive sectors.

Organic Rankine Cycle Waste Heat To Power Market

From a commercial standpoint, demonstrated project economics are compelling for many end-users: our synthesis of industry data shows typical industrial payback windows for cement plant ORC retrofits commonly fall in the 4–8 year band, depending on electricity tariffs, operating hours, and system scale. That profile places ORC investments within the investment horizon of corporate CAPEX committees and infrastructure funds targeting stable, contracted returns.

Organic Rankine Cycle Waste Heat To Power Market

The ORC WHP market remains moderately fragmented. Market concentration metrics indicate that the top three providers account for under a quarter of market value, and the top five about one-third, leaving significant share for regional specialists, technology purveyors, and equipment integrators. That market structure creates parallel opportunities: scale and brand advantages for incumbents who can deliver global project execution, and white-space opportunities for agile entrants and niche specialists that can tailor solutions for low-temperature streams, micro-grid applications, or aftermarket service models.

The technology landscape includes a spectrum from micro-ORC modules for low-temperature applications to multi-megawatt units and multi-shaft solutions for high-temperature industrial plants. Fluids, turbines, heat-exchanger design, and balance-of-plant integration remain competitive battlegrounds, with innovation focused on improved turndown, lower parasitic losses, and simplified O&M.

Recent industry developments further crystallize market dynamics. Notably, Turboden’s commissioning of a 19 MW ORC plant at a SAGD facility in Alberta (Oct 2025) and its subsequent award to supply multiple compressor-station plants in North America (2026) demonstrate how oil-and-gas heat sources are becoming high-priority, baseload ORC markets. These projects also highlight the importance of strong EPC and O&M propositions when ORC systems are integrated into critical industrial operations.

The full study is structured to move executives from strategic intent to executable plans. Key deliverables include:

These practical tools are paired with PW Consulting’s proprietary database of vendor deployments, component pricing ranges, and reference plant performance metrics (available in the subscriber version). The public brief you are reading purposefully summarizes the findings without revealing the granular split tables and project-level inputs that underpin our valuations.

Key risks in the next 12–24 months include regulatory shifts around working fluids (PFAS/HFC restrictions), supply-chain constraints for specialized components, and variability in merchant power prices that can lengthen payback periods. Mitigation strategies we recommend include early selection of compliant fluids with proven supply chains, contractual pass-through mechanisms for long-lead items, and structuring of offtake agreements that include availability payments or capacity credits.

Technical risks — especially in retrofit projects — center on heat-source predictability and plant integration complexity. Robust site surveys, third-party thermal mapping, and staged commissioning protocols reduce execution risk. Financially, blending construction-period guarantees, performance bonds, and insurance for availability can make projects bankable to traditional infrastructure lenders.

This release is a strategic preview designed to convey PW Consulting’s core findings and recommended playbooks for 2026. The full report contains the granular segmentation, regional and application split tables, supplier deployment maps, and the downloadable financial model that corporate and investor clients use to make funding and procurement decisions. For clients ready to move from strategy to execution, PW Consulting offers a tailored 8–12 week Rapid Implementation sprint that combines site-level feasibility, procurement support, and due-diligence-ready financial modeling.

Contact PW Consulting to request the full report and schedule a briefing with our ORC practice leads. The window to influence 2026 CAPEX allocation and secure prime-of-the-market deployment slots is narrow; firms that align technology choice, off-take structures, and supply-chain partnerships now will lead the next wave of waste-heat monetization.

For detailed analysis of this topic, please visit the official page:Organic Rankine Cycle Waste Heat To Power Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com