Strategic Preview: Robotics in Shipbuilding Market — PW Consulting 2026 Outlook

Executive summary

As global shipyards confront a confluence of labor shortages, tighter safety standards, and accelerated delivery timetables, robotics and physical AI are moving from pilot projects to critical-path production enablers. PW Consulting’s latest Robotics in Shipbuilding Market report (base year 2025, forecast 2026–2032) finds that the market expanded from roughly USD 295 million in 2020 to USD 420 million in 2025, and is expected to grow to approximately USD 697 million by 2032 at a compound annual growth rate (CAGR) of 7.5%. The market structure is neither highly fragmented nor tightly consolidated — the top three firms hold a clear lead while a broader set of specialised providers capture meaningful share — creating windows for both incumbent robotics OEMs and focused specialists to scale.

Robotics in Shipbuilding Market

This preview outlines the report’s strategic value for executive decision-making in 2026: what to prioritize in capital planning, how to structure vendor and partner selection, where to deploy digital twins and physical AI to safeguard throughput, and which implementation risks deserve board-level attention. Detailed segment-level data, proprietary supplier matrices, and modelled ROI scenarios remain reserved for the full report and online portal to preserve actionable differentiation for our subscribers.

Robotics in Shipbuilding Market

What the report delivers — practical, decision-ready intelligence

- Market sizing and growth trajectories (2020–2032) with scenario modelling under alternative adoption and supply-chain stress assumptions.

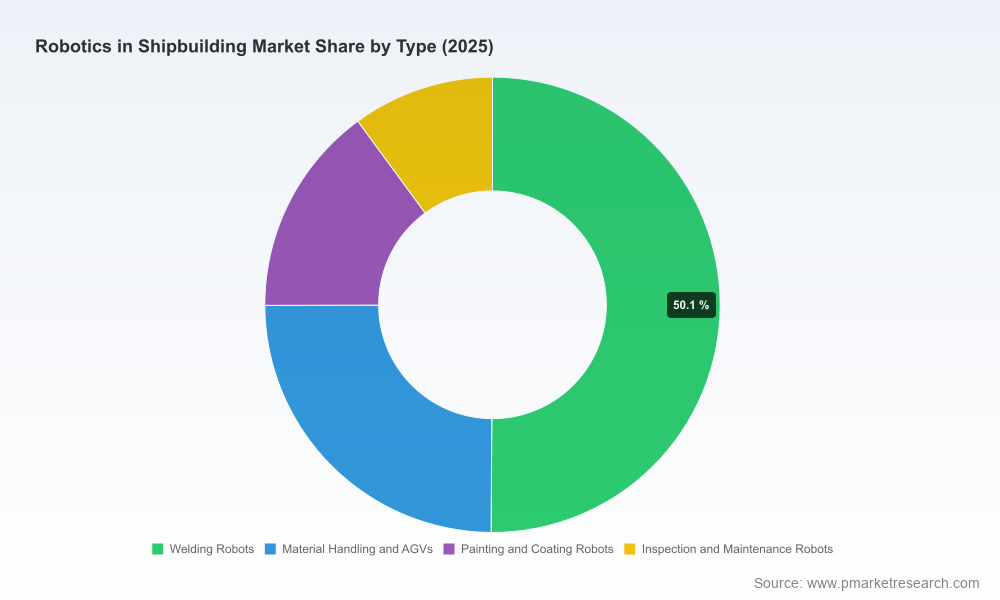

- Technology and commercial segmentation frameworks mapping robotics solutions to shipyard functional needs — welding, material handling, surface treatment, inspection and maintenance — with buyer use-cases and readiness criteria.

- Capital planning tools: unit-level acquisition ranges, total installed cost multipliers, and multi-year TCO / ROI calculators for greenfield and retrofit deployments.

- Implementation playbooks: site readiness checklists, integration sequencing (mechanical, controls, safety), and workforce transition plans to de-risk production ramp-up.

- Vendor evaluation matrix: capability, scale, deployment maturity, and ecosystem fit — including assessments of leading industrial OEMs and niche innovators.

- Strategic M&A and partnership playbook highlighting how buyers, system integrators, and defence primes can accelerate capability with limited internal R&D.

- Regulatory and safety compliance guidance for collaborative robotics and physical AI deployments to support human-robot interaction without traditional fencing.

- Case studies and site-level performance benchmarks — anonymized — showing realized productivity uplifts and learning curves across early adopters.

Key market dynamics shaping 2026 decisions

Three systemic forces are driving the 7.5% CAGR and reshaping investment priorities:

Robotics in Shipbuilding Market

- Labor scarcity and skills mismatch. Persistent shortages of skilled welders and fabricators are a principal demand driver for adaptive robotic welding and autonomous surface-treatment systems. For executives, robotics is increasingly a capacity-preservation strategy rather than purely a cost play.

- Capital and integration economics. Typical industrial robotic units employed in marine production range in acquisition price at a modest capital level per unit, yet total installed costs commonly run multiple times the equipment price once integration, tooling, fixturing, programming and commissioning are included. Our report’s CapEx and site-level cash-flow templates translate these realities into finance-ready capital requests.

- Component and enabling-technology deflation. Key sensor modules — notably six-axis force-torque sensors — have seen rapid price declines thanks to tighter integration and scale. That trend materially reduces unit costs for force-aware welding and sanding/grinding cells, improving payback timelines for retrofit projects.

- Regulatory and safety acceleration. The increasing acceptance of collaborative robots and certified physical AI frameworks allows human-robot collaboration in tighter shop-floor footprints, lowering facility modification costs and accelerating deployment windows.

- Public-sector and defence adoption. Strategic programmes and grants (including recent public funding for digital twins and AI-based deviation handling) are accelerating applied R&D, shortening the commercialization pathway for robot-enabled repair and retrofit services.

Competitive landscape — what leaders and challengers reveal about strategy

The market is characterized by a mix of large industrial automation incumbents and specialised innovators. PW Consulting’s competitive analysis synthesises capability, scale, service model, and go-to-market posture for the leading players.

- ABB (Switzerland) — Established industrial-robot supplier with broad automation stacks for welding, material handling, and precision assembly. ABB’s strength lies in end-to-end automation platforms, integration with power and motion systems, and a global service footprint. Ideal for large-scale shipyard modernisations that demand system-level reliability and long-term service contracts. (See company at https://www.abb.com)

- FANUC Corporation (Japan) — Known for high-reliability, high-throughput industrial robots optimized for welding and heavy manipulation. FANUC’s installed base in high-volume Asian shipyards makes it a first-choice for shipbuilders focused on throughput scaling and repeatability. (https://www.fanuc.com)

- KUKA AG (Germany) — Strong in complex automation where integration with digital engineering and flexible cell design is required. KUKA’s value proposition is in orchestrating multi-robot workflows for complex assembly and outfitting tasks. (https://www.kuka.com)

- Yaskawa Electric Corporation (Japan) — Offers robust industrial arms (Motoman) tuned for heavy fabrication and arc welding robustness. Yaskawa’s appeal is in operational durability in heavy industrial environments. (https://www.yaskawa-global.com)

- Kawasaki Heavy Industries (Japan) — Provides robotics solutions that leverage heavy machinery expertise, notably for painting and structural assembly in marine environments. Kawasaki’s domain knowledge in marine equipment supports integrated mechanical solutions. (https://www.kawasakirobotics.com)

- KRANENDONK (Netherlands) — Niche specialist in intelligent automation for panel, block and pipe fabrication with adaptive gantries suited to low-repetition production typical of shipbuilding. Offers pragmatic retrofit solutions for shipyards with high product mix.

- Inrotech (Lincoln Electric, Denmark) — Focused on adaptive mobile welding robots that minimise CAD programming needs for variable joint geometries. Their tooling reduces engineering overhead for shipyards with heterogeneous build profiles. (https://www.inrotech.com)

- GrayMatter Robotics (USA) — Physical-AI specialist delivering surface preparation, coating and inspection systems. Partnerships with major naval primes underline a path to scaled defence adoption for autonomous finishing and inspection. (https://www.graymatter-robotics.com)

- Path Robotics (USA) — Delivers AI-driven autonomous welding cells suitable for manned and unmanned production lines, with notable recent collaboration activity aimed at naval shipbuilding acceleration. (https://www.path-robotics.com)

Market concentration is meaningful: the top three vendors capture a material portion of market value while the top five extend the share further, indicating space for vertical specialists and systems integrators to capture niche mandates and value-add services.

Recent ecosystem developments illustrative of near-term adoption

- Strategic alliances between defence primes and physical-AI vendors to accelerate welding, surface treatment and autonomous inspection programs have moved from pilots to signed MOUs in 2026 — signalling a step-change in procurement appetite.

- University-industry research grants targeting AI and digital twins were awarded in 2026 to address design deviation handling — a practical barrier to autonomous assembly in high-variation shipbuilding contexts.

- Public and private investments are increasingly targeted at systems that reduce dependency on scarce craft labour while delivering measurable throughput gains — creating procurement mandates that prioritise speed-to-value.

Strategic implications & recommended actions for 2026

- For shipyard CEOs and COOs: treat robotics as capacity insurance. Prioritise deployments that protect critical-path operations (welding and hull assembly) and validate ROI with real production KPIs rather than vendor-supplied benchmarks.

- For CTOs and program managers: mandate site-level readiness assessments and use the report’s integration sequencing templates to avoid typical scope creep and cost escalation associated with retrofit installs.

- For finance and procurement: use our TCO templates to reconcile headline equipment prices with realistic installed-cost multipliers and to stage capital spend across modular deployments that reduce payback risk.

- For OEMs and system integrators: target fast-follow niches where component cost declines (e.g., sensors) enable new business models — such as-as-a-service offerings for finishing and inspection that convert CapEx into predictable Opex.

- For investors and M&A teams: prioritise assets that combine domain knowledge in marine fabrication with software/IP for variance handling (digital twins, physical AI) and proven integration playbooks with defence primes or large commercial shipyards.

Conclusion — why PW Consulting’s 2026 report matters

Robotics in shipbuilding is transitioning from a technology play to an operational imperative. The market’s projected expansion to roughly USD 697 million by 2032 at a 7.5% CAGR underpins clear commercial opportunity, but realization depends on pragmatic integration, supplier selection, and workforce transition. PW Consulting’s report translates macro forecasts into executable plans: from procurement-ready CapEx models and ROI calculators to vendor matrices and safety-compliant integration playbooks.

This briefing highlights the strategic contours and actionable priorities; detailed segmentation, supplier scoring, and our proprietary datasets that underpin financial models and adoption scenarios have been intentionally reserved for the full report. For program teams preparing 2026 capital requests or partners evaluating strategic collaborations, the full dataset provides the granular evidence to make defensible, board-ready decisions.

How to access the full analysis

To obtain the complete report, including full segmentation tables, ROI models, and the proprietary vendor matrix, please visit the PW Consulting research portal. Subscribers will receive the model workbooks and implementation checklists required to convert strategic intent into measurable production outcomes.

For detailed analysis of this topic, please visit the official page:Robotics in Shipbuilding Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com