Exosome Therapy and Its Role in Hair Restoration Science

Health |

2026-04-10 10:49:38

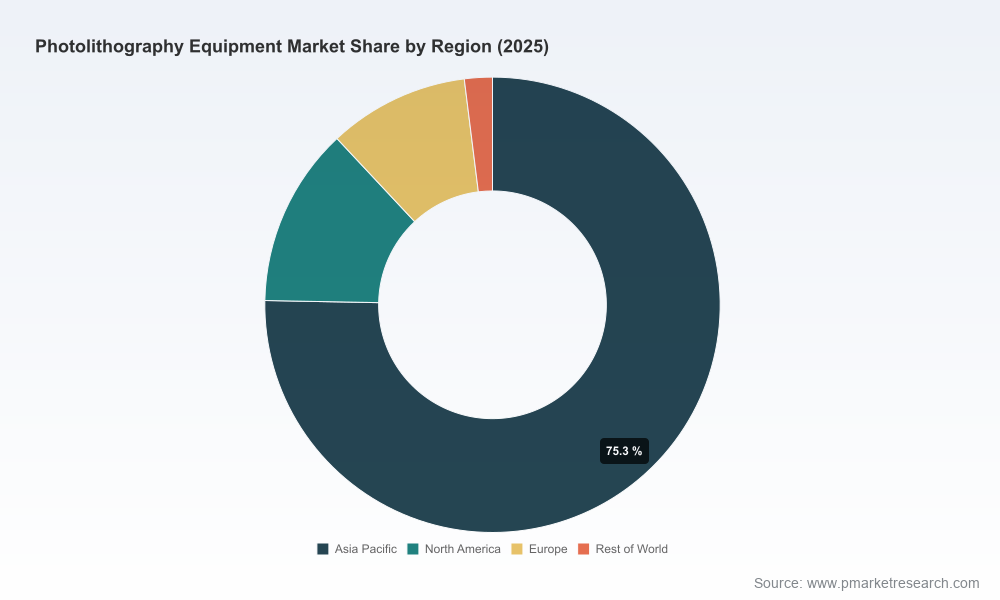

PW Consulting today publishes a focused industry brief drawn from our comprehensive Photolithography Equipment Market Research report. Designed as a decision-grade compass for C-suite and investment teams preparing for 2026, this briefing translates complex technology, supply-chain, and geopolitical signals into actionable strategic options. Our analysis is grounded in a macro forecast that tracks the market from a USD 14.5 billion baseline in 2020 to USD 32.45 billion in 2025, and projects sustained expansion at a 10.45% CAGR through 2032, when the market is expected to exceed USD 65 billion. While this release highlights the research’s most consequential insights, granular segment-level figures and proprietary scenario outputs are reserved for the full report to preserve its role as an indispensable operational tool.

Photolithography Equipment Market Research

Capital allocation timing: Semiconductor OEMs and fabless companies transitioning from design to production must reconcile multi-year equipment lead times with an accelerating capital cycle driven by AI and high-performance computing demand. Our forecast and CAPEX modeling templates enable finance teams to align tranche-based investment with expected throughput and node migration schedules.

Photolithography Equipment Market Research

Supplier strategy under concentrated supply: The industry sits behind a highly concentrated supplier structure (CR3: 98.5%; CR5: 99.85%), creating winner-takes-most dynamics. Procurement, legal, and manufacturing leaders must prioritize supplier governance, service-level guarantees, and contingency contracts now — 2026 is the pragmatic inflection point for locking in supply resilience.

Photolithography Equipment Market Research

Regulatory and geopolitical readiness: Export controls and localization policies are reshaping deployment geographies and partnerships. Companies should bake regulatory scenario planning into their market-entry, joint-venture, and M&A playbooks for approvals that will be sought and executed in 2026.

Demand shock from computational workloads: Macro forecasts underpinning this research incorporate industry guidance anticipating a meaningful wafer fab capacity increase by 2026, driven by AI, datacenter acceleration, and automotive electrification. The pace of node migration and mix of capacity expansion will materially affect photolithography tool demand profiles over the next two planning cycles.

Technology bifurcation and roadmap implications: High-end nodes are progressing toward higher numerical-aperture EUV systems while mature-node ecosystems continue to rely on advanced DUV platforms. Recent commercial milestones — including the first High-NA EUV deployment for sub-3nm process development and ongoing ArF immersion system upgrades — confirm a bifurcated investment landscape where product roadmaps and service capabilities differ sharply by supplier and region.

Supply chain constraints and cost pressure: Critical upstream materials and sub-suppliers (for example, multilayer EUV optics and specialty gases) have constrained ramp profiles and increased unit economics. Our cost-stack modeling quantifies a range of scenarios where inputs such as helium isotopes and optics coatings can shift total cost of ownership and service economics across the forecast period.

Policy-driven market shaping: Tighter export controls and national localization targets are fragmenting technology flows. This creates near-term demand for alternative sourcing and domestic capability building in certain markets — a strategic signal that impacts partner selection, IP licensing, and joint-development strategies through 2026 and beyond.

Market structure: The photolithography equipment market is an oligopoly at the global scale. A small set of global suppliers dominate advanced-node systems, while other vendors specialize in established-node DUV platforms and regionally focused offerings. This concentration drives sustained pricing power, long order books, and differentiated aftermarket economics.

Profiles of leading players: Our company dossiers synthesize strategy, product roadmaps, and service models for the industry’s core participants. Highlights include:

ASML Holding N.V. (Veldhoven, Netherlands) — Dominant provider of EUV and DUV platforms; recent commercial High-NA shipment underscores their technological leadership and implications for partners targeting sub-5nm nodes. (asml.com)

Nikon Corporation (Tokyo, Japan) — Strengths in DUV steppers/scanners serving a range of legacy and mid-node processes; ongoing product showcases signal incremental performance upgrades for cost-sensitive high-volume manufacturing. (nikon.com)

Canon Inc. (Tokyo, Japan) — Competitive in ArF immersion and KrF systems with an emphasis on throughput and HVM upgrades; complementary nanoimprint approaches represent potential disruptive adjacencies. (global.canon)

Shanghai Micro Electronics Equipment (SMEE) (Shanghai, China) — Focused on domestic DUV immersion platforms aimed at accelerating local node capabilities amid localization policies. (smee.com.cn)

Recent developments and implications: The bulk of recent industry activity has reinforced technology-specific leadership and aftermarket advantage. Publicized events in 2024 — a High-NA EUV system shipment, new ArF immersion product showcases, and production-focused system upgrades — each have discrete downstream impacts that our strategic playbooks translate into procurement lead times, integration risk, and TCO sensitivity for different buyer archetypes.

What we do not disclose here: To preserve the report’s value as a strategic asset, detailed segment-level demand splits, per-region deployment curves, and unit-volume forecasts are excluded from this press briefing. The full report contains granular datasets, supplier scorecards, and scenario matrices necessary to execute supplier selections and capital plans.

Actionable forecasting: Top-down and bottom-up market models across a 2026–2032 horizon, with scenario toggles for policy, materials, and demand shocks.

Supplier heatmaps and risk matrices: Comparative analysis of product roadmaps, service footprints, and strategic options for securing capacity or entering partnerships.

Supply-chain decomposition: Cost-stack templates, critical-material exposure assessments, and mitigation strategies for optics, specialty gases, and consumables.

Regulatory and policy tracker: A dynamic framework for assessing export control impacts, localization incentives, and compliance timelines across relevant jurisdictions.

CapEx and ROI playbooks: Decision trees, sensitivity analyses, and an investment timing guide aligned to node migration and demand elasticity assumptions.

M&A and partnership screening: Criteria-based shortlists and diligence checklists tailored to acquirers seeking near-term capacity or technology access.

Secure multi-modal supply routes: Firms should build layered agreements that combine direct OEM commitments, regional service contracts, and strategic inventory positions for consumables. Given supplier concentration, negotiating service-level protections and spares agreements is a high-return risk reduction move.

Invest selectively in node diversity: Not all logic or memory opportunities require the latest node equipment. A nuanced build-versus-buy framework helps prioritize capital to match product lifecycles and margin profiles.

Pursue strategic partnerships with optics and materials suppliers: Optical coatings capacity and specialty gas supply are single points of friction; co-investment and long-term purchase agreements with these tiers materially reduce schedule and cost risk.

Embed regulatory scenario planning: Anticipate export control shifts by structuring licensing, JV terms, and dual-sourcing strategies in a manner that preserves agility across alternative deployment geographies.

Prioritize aftermarket and uptime economics: In a concentrated market, service contracts, upgrade paths, and retrofitability drive lifetime value more than initial equipment price.

For strategic leaders preparing 2026 budgets: Use our high-level forecasts and CAPEX templates to stress-test investment scenarios across optimistic, baseline, and constrained supply cases.

For procurement and operations teams: Leverage the supplier heatmap and risk matrices to re-run vendor negotiations with an emphasis on guaranteed throughput, spares, and retrofit options.

For investors and M&A teams: The report’s integration of technological milestones, supply constraints, and policy shifts enables refined valuation assumptions and identification of strategic targets.

PW Consulting’s full Photolithography Equipment Market Research report contains the proprietary datasets, supplier scorecards, and scenario engines referenced above. For decision-makers who must convert forecast conviction into executable plans in 2026, the report provides the empirical foundation and operational toolset to prioritize investments, secure capacity, and mitigate regulatory and supply-chain threats. Visit PW Consulting to download the full study and access custom advisory services tailored to your role in the value chain.

Contact our industry analysts to arrange a briefing session and to explore bespoke modeling aligned to your portfolio, geography, and node targets. The strategic window for decisive action is now — use the remainder of 2025 to prepare a defensible, opportunity-focused plan for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Photolithography Equipment Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com