Pediatric Radiation Therapy Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-15 10:03:15

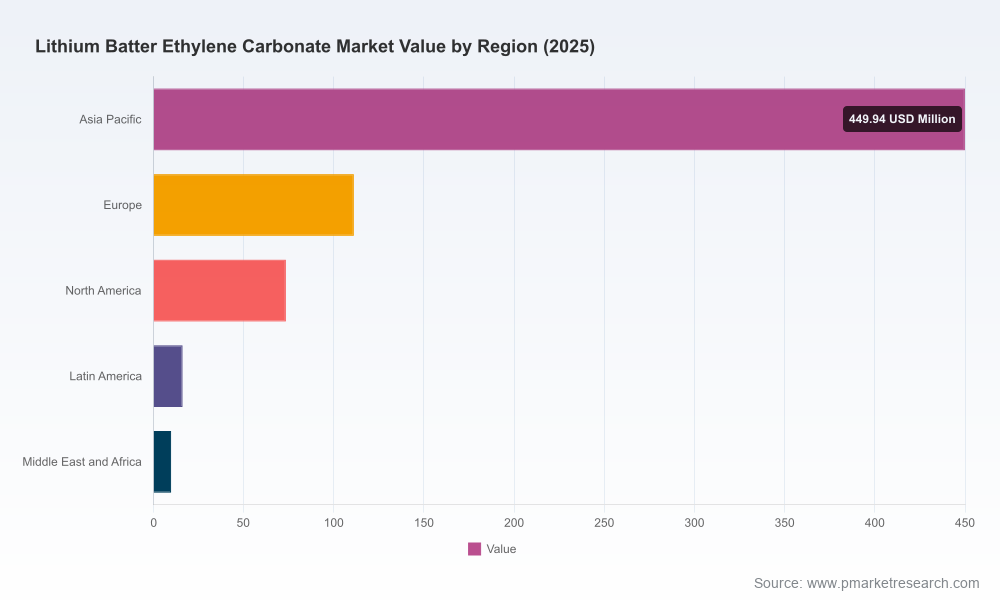

As the lithium-ion battery ecosystem accelerates into its next phase of commercialization, ethylene carbonate (EC) remains a strategic raw material at the heart of electrolyte formulations. PW Consulting’s newest market study — built on a 2020–2025 historical base and projecting through 2032 — quantifies this transition and translates it into decision-grade guidance for executives planning actions in 2026. At the macro level, the global EC market has moved from a mid-hundreds million USD base in 2025 and is forecast to more than double by 2032, tracking at a robust compound annual growth rate (CAGR) of approximately 13.15% over the 2026–2032 forecast window. This growth trajectory underscores both clear commercial opportunities and material strategic risks for producers, battery manufacturers, traders, and investors.

Lithium Batter Ethylene Carbonate Market

Timing capital allocation: Our modeling reconciles near-term demand pull from electric vehicle (EV) supply chains with longer-term structural demand from stationary storage and consumer electronics. It identifies when greenfield and brownfield investments become cash-generative under alternative pricing scenarios.

Lithium Batter Ethylene Carbonate Market

Procurement and contract design: The report translates feedstock cost dynamics into practical contracting levers — from indexation approaches to capacity reservation agreements — so procurement teams can lock favorable economics without forfeiting flexibility.

Lithium Batter Ethylene Carbonate Market

Regulatory and technology risk management: We map regulatory pressure points and emerging electrolyte innovations (including EC-lean and EC-free formulations) to quantify upside and downside scenarios for incumbent EC demand.

M&A and partnership screening: Our competitive benchmarking and target filtering accelerate target selection by highlighting which assets deliver feedstock security, quality differentiation, or rapid scale-up potential.

EC’s role as a high-dielectric, high-boiling-point cyclic carbonate keeps it central to mainstream lithium-ion electrolyte chemistries. Historical demand through 2025 reflected steady adoption across EVs, portable electronics, and grid-scale storage, with a notable acceleration driven by automotive electrification cycles and battery chemistry upgrades. Industry production volumes in the mid-decade indicate that a large proportion of global EC output is already consumed by lithium-ion battery electrolytes, and that underlying feedstock dynamics — particularly the cost and availability of ethylene oxide — materially influence producer margins, representing a dominant share of production input costs.

At the same time, the market is not a one-way street. Two countervailing trends merit careful monitoring: first, environmental policy and manufacturer commitments are driving roughly half of producers to shift to lower-emission synthesis routes, often through CO2-based feedstock processes, which has implications for CAPEX profiles and unit costs. Second, battery chemistry research continues to explore EC-reduced or EC-free electrolytes as a pathway to mitigate high-temperature side reactions and improve cell safety. While these innovations are not yet a mainstream replacement, they are an explicit downside scenario for long-duration EC demand and are modeled as such in our scenario suite.

The EC value chain exhibits a moderate-to-high concentration at its top tiers. The three largest integrated producers capture a significant portion of global volumes, and the top five account for a clear majority — a structure that creates both pricing power and capacity bottleneck risk in certain geographies. However, quality requirements and technical entry barriers for battery-grade EC (>99.99% purity) mean that not every chemical producer can address the battery market without dedicated investment in purification, quality management systems, and contamination-control supply chains.

Leading incumbent profiles and strategic postures that the report examines in depth include:

Long-established multinational chemical groups that combine global sourcing reach with advanced high-purity production platforms — positioning them to serve both automotive-tier OEMs and specialty-electrolyte formulators.

Regional leaders with localized production capabilities serving domestic battery manufacturers, often competing on lead time and integrated logistics rather than absolute lowest cost.

China-based manufacturers with vertically integrated feedstock chains that can move aggressively on price and capacity but face increasing scrutiny on emissions and product quality for export-grade battery applications.

Recent industry activity illustrates these dynamics: capacity additions and strategic network reconfigurations by major producers are focused on proximity to battery manufacturing hubs and on optimizing feedstock supply. Additionally, announced investments in new electrolyte solvent plants reflect an intent by both specialty-electrolyte players and integrated chemical producers to lock-in carbonate output. For market participants, these moves signal a shift toward more regionally balanced supply and a window for countervailing strategies (e.g., toll manufacturing, long-term tolling agreements, and joint ventures).

PW Consulting’s full study is deliberately practical. It is structured to answer the “what do I do tomorrow?” question for commercial, technical, and corporate development teams. Key deliverables include:

A calibrated supply–demand model with monthly and annual balances through 2032 and a sensitivity engine for feedstock shocks.

Price-formation framework and scenario-based price forecasts tied to supply chain stress tests and policy shock scenarios.

Plant-level CAPEX/OPEX benchmarks and step-up cost curves for incremental battery-grade capacity.

Supplier scorecards incorporating quality, ESG performance, logistics risk, and commercial flexibility to support shortlists and RFP evaluations.

M&A screening matrices and a prioritized list of actionable targets across scales and geographies — including commercial rationales and integration risk assessments.

Regulatory intelligence and an emissions-compliance playbook aligned to low-emission synthetic routes and permitting timelines.

To honor the “trailer” principle, the report deliberately withholds granular tables of regional and application-level shares in this press release — those datasets, and the interactive model attachments, are available only in the full report package.

For producers: prioritize brownfield debottlenecking and targeted high-purity upgrades that shorten time-to-market versus greenfield build-outs; accelerate low-emission process pilots to future-proof permits and corporate ESG commitments.

For battery manufacturers: secure multi-year offtake with quality and ESG clauses, include flexibility for minor chemistry shifts, and build layered tiering strategies (strategic partners + spot access) to manage supply risk.

For traders and distributors: invest in logistics and blending capabilities to arbitrage regional price dispersion and to offer rapid-response supply to OEM ramp-ups.

For financial sponsors: prefer assets with access to high-purity production routes, feedstock integration, or differentiated logistics; stress-test investment cases against EC-lean electrolyte adoption scenarios.

For policymakers and industrial planners: recognize that targeted incentives for low-emission carbonate production can unlock domestic battery ecosystems while reducing import reliance, but interventions should be time-phased to avoid stranded-asset risk.

Three risks deserve heightened vigilance in 2026: raw material shocks (ethylene oxide volatility), technological substitution (EC-lean electrolytes), and regulatory shifts that accelerate low-emission synthesis adoption. Our multi-scenario framework quantifies financial outcomes under each risk vector and provides trigger points for defensive and offensive moves — such as converting tolling relationships into capacity partnerships, or pivoting to specialty carbonate blends with higher margins.

PW Consulting’s Lithium Battery Ethylene Carbonate Market report is designed to function as an executable playbook for 2026. The complete package includes the interactive model, full competitive company dossiers, plant-level benchmarking sheets, and a prioritized deal-screen for M&A. If you are preparing capital plans, contractual negotiations, or R&D roadmaps for the coming 12–24 months, the full report delivers the granular, sourced intelligence you will need to act with confidence.

Contact PW Consulting to request the full report and the associated datasets — including the downloadable model that powers the scenarios summarized above. With EC at the crossroads of chemistry, capital, and climate policy, timely, rigorous intelligence will be the differentiator between winning supply positions and being exposed to second-order market shocks in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Lithium Batter Ethylene Carbonate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com