Global Precipitated Silica from Rice Husk Ash Market Growing at 10.4% CAGR

Other |

2026-06-18 12:05:24

As commercial decision‑makers plan product roadmaps, procurement strategies, and regulatory compliance in 2026, the small batteries market presents a mix of steady growth, concentrated supplier power, and heightened safety and raw‑material volatility that together will shape competitive advantage. Our new PW Consulting Commercial Small Batteries Market report synthesizes macro trajectories and actionable playbooks—without giving away the tactical maps reserved for report subscribers—so executives can prioritize where to invest attention and capital this year.

Commercial Small Batteries Market

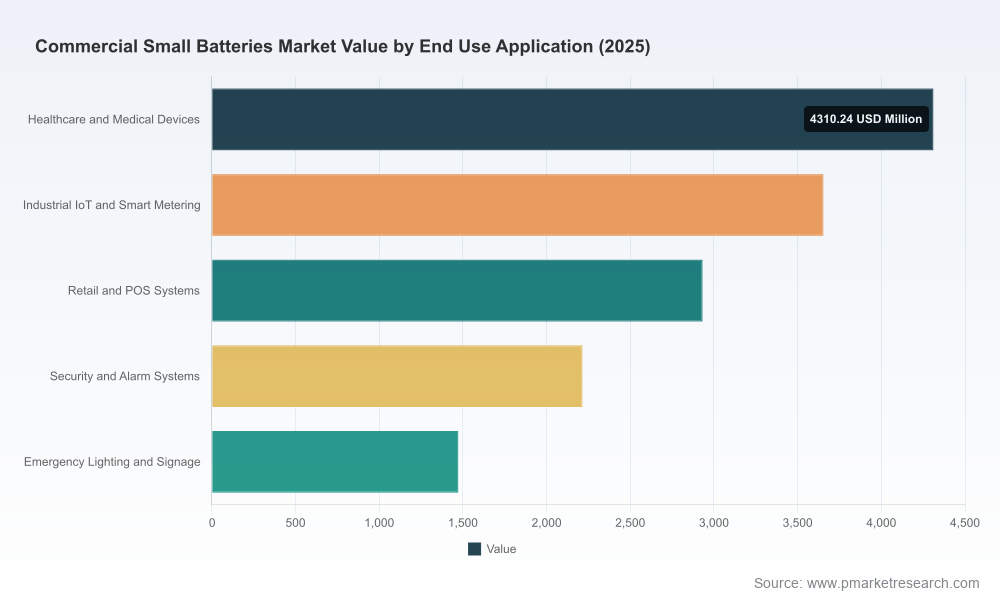

The market for commercial small batteries reached a substantial scale by 2025 and is set to expand further in 2026 and beyond. PW Consulting’s full model projects sustained expansion through the 2026–2032 forecast window at a compound annual growth rate of approximately 6.8%. That pace reflects a blend of continued demand from healthcare devices, industrial IoT rollouts, retail and point‑of‑sale systems, and steady replacement cycles across commercial applications.

Commercial Small Batteries Market

Why this macro picture is strategically useful in 2026: a mid‑single‑digit CAGR at an established market base signals opportunity for selective premiumization (safety‑enhanced and long‑life chemistries), scale plays (cost reduction via procurement and contract consolidation), and technology arbitrage (transitioning small form‑factor designs to higher energy‑density chemistries where safety and regulation permit).

Commercial Small Batteries Market

PW Consulting’s market study is built for executives who need to translate market insight into 90‑day and 18‑month action. The report is intentionally practical: it combines quantitative modeling with executable guidance across procurement, product, compliance, and M&A scouting. Highlights include:

The commercial small batteries segment remains shaped by a mix of legacy powerhouses and specialist manufacturers. Key incumbent profiles—ranging from multinational household brands to niche precision‑cell makers and backup‑power specialists—exhibit differing strategic advantages:

Competitive moves to watch in 2026 include product line expansions into adjacent small battery formats, selective capacity investments in response to regional demand shifts, and vertical integration plays to secure raw‑material access. Recent market signals—exhibitions that highlighted small battery innovations and product launches focused on child safety coatings—underscore a trend toward safety‑driven product differentiation and regulatory signaling as a commercial advantage.

2025–2026 saw an intensification of regulatory attention on small batteries. Decision makers must prioritize three regulatory vectors in 2026:

Raw‑material dynamics will materially affect unit economics and supplier risk in 2026. Lithium feedstock experienced a notable price rebound in the 2025 cycle, and consensus scenarios point to continued volatility this year. For commercial buyers and product designers this translates into three actionable steps:

From PW Consulting’s strategic vantage point, the commercial small batteries market offers asymmetric opportunities for firms that act on four levers:

For executives who need a clear path forward in 2026, PW Consulting recommends a two‑horizon approach:

Many market studies end at headline sizing and vendor listings. Our report couples that quantitative foundation with tactical artifacts—cost models, compliance matrices, and go‑to‑market playbooks—designed to be operationalized by procurement, product, and legal teams in 2026. We deliberately keep proprietary subsegment tables and granular supplier market‑share models behind the paywall: that level of tactical intelligence is what differentiates strategic programs from generic planning documents.

Leaders should treat the 2026 planning cycle as an inflection point: the market is large and growing, but margins and market access will be determined by how firms respond to safety regulation, raw‑material volatility, and channel expectations. Use macro forecasts to set investment horizons, the regulatory matrix to define compliance roadmaps, and the procurement models to renegotiate contracts with an informed view of price sensitivity.

For the exhaustive data tables, supplier benchmarking, and executable templates that will directly inform procurement negotiations and product launch timelines in 2026, PW Consulting’s full Commercial Small Batteries Market report provides the confidential, granular intelligence you need. Visit our report landing page to review the extended methodology, download the executive slide deck, and request a tailored briefing with our industry team.

For detailed analysis of this topic, please visit the official page:Commercial Small Batteries Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com