At-Home Hair Removal Devices Market — Strategic Imperatives for 2026

PW Consulting’s new market study on At-Home Hair Removal Devices delivers an executive-grade, action-oriented intelligence package designed to inform boardroom decisions throughout 2026. Built on a rigorously validated market model (base year 2025) and a seven-year forecast, the report combines quantitative market sizing, regulatory intelligence, competitive mapping, go-to-market playbooks and scenario-ready strategic options. Executive teams in product, regulatory, commercial and corporate development will find the analysis directly applicable to capital allocation, new product investment, channel strategy and M&A prioritization.

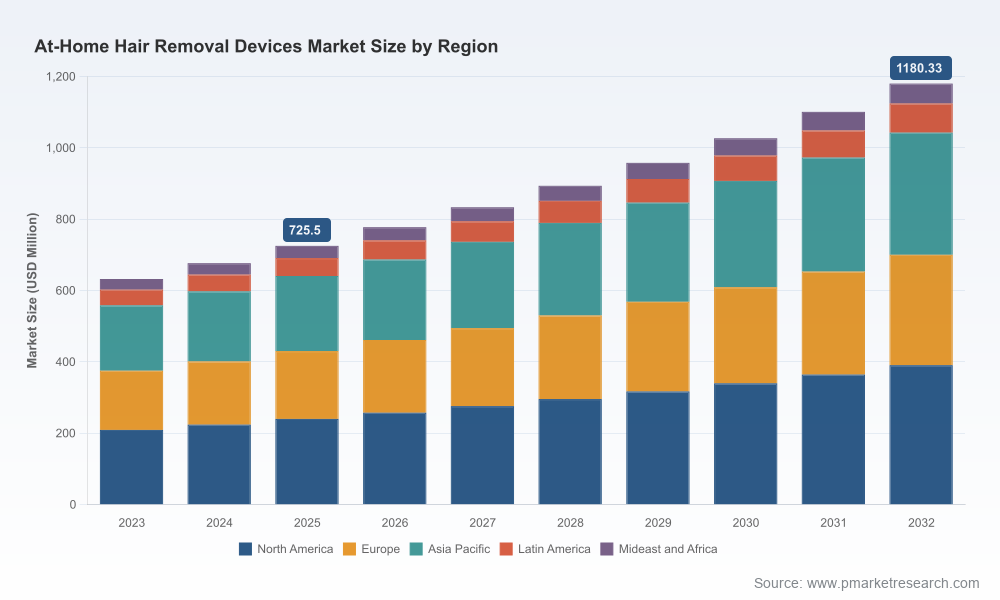

At Home Hair Removal Devices Market

Market snapshot

After steady expansion through the early 2020s, the at-home hair removal devices market reached an estimated USD 725.5 Million (Million USD unit, base year 2025). The market accelerated from roughly USD 632 Million in 2023 and USD 677 Million in 2024, and is projected to continue growing at a compound annual growth rate (CAGR) of approximately 7.2% over the forecast horizon (2026–2032). By 2032, our central scenario anticipates a market size north of USD 1.1 billion, reflecting both expanding consumer adoption and incremental enhancements in device efficacy, safety and channel economics.

At Home Hair Removal Devices Market

This growth is demand-driven (consumer willingness to substitute repeated professional sessions with one-time at-home solutions), technology-driven (improvements in IPL and diode laser implementations and adjacent comfort features), and distribution-driven (channel shift to direct e-commerce and D2C subscription models). At the same time, supply-side dynamics — from rising raw material and components costs to regulatory clearance timelines — introduce tangible constraints and opportunities that shape strategic timing.

At Home Hair Removal Devices Market

What the report delivers — practical, decision-ready content

- Validated market model with historical series (2020–2025) and multi-scenario forecasts (2026–2032) that can be fed directly into corporate planning systems.

- Competitive intelligence dossiers on incumbent and challenger brands, including product feature benchmarking, patent exposure indicators, and go-to-market footprints.

- Regulatory and reimbursement tracker tailored to Class II light-based devices — including a timeline of recent 510(k) clearances and jurisdictional requirements affecting market entry velocity.

- Channel and pricing playbooks: SKU rationalization, promotional elasticity estimates, and recommended channel mixes for premium versus value segments.

- Manufacturing and supply-chain risk map, with mitigation options for escalating raw material and electronic component costs.

- Early-warning indicators and KPI dashboards for real-time monitoring (sales velocity by channel, clearance pipeline milestones, return rates, NPS by cohort).

- Strategic scenarios and a 100–150 day tactical plan for market entry, product relaunch, or M&A integration.

Note: This article presents headline market sizing and strategic conclusions to establish perspective. Detailed segment-level revenue splits and unit economics are intentionally withheld here to preserve the report’s proprietary value; those granular datasets and downloadable models are available in the full report.

Key strategic implications for 2026 decision-makers

- Prioritize regulatory-first roadmaps. With at-home IPL and laser devices regulated as Class II medical devices in the U.S. and requiring 510(k) clearance, regulatory timelines materially affect time-to-market and cost. Recent 2025 510(k) activity — including clearances for multiple new ICE-cooling IPL models — demonstrates both a pathway and an operational cadence for entrants. For 2026 launches, secure regulatory engagement early and factor iterative clinical and usability cycles into development sprints.

- Design product tiers around clinical-grade differentiation and convenience. Consumer willingness to pay is increasingly determined by demonstrable efficacy claims, comfort technologies (cooling, integrated skin-sensing), and usage economics (flash counts, consumables). Investments in higher-efficacy diode laser variants or platform variants that enable premium pricing can pay back faster in markets where clinical-grade positioning resonates.

- Capture the e-commerce premium without abandoning retail presence. Digital-first distribution continues to unlock lower customer acquisition costs and recurring revenue through consumables or warranty-extension up-sells. However, retail still plays a crucial role in discovery and competitive parity for mainstream consumers. The winning model in 2026 is hybrid: D2C for margin and data capture; selective retail for visibility and trust.

- Reassess cost architecture against raw material inflation. Rising costs in plastics, metals and electronics — documented across the sector in 2025 — compress gross margins for consumer device manufacturers. Optimization levers include strategic component sourcing, design-to-cost exercises, localized assembly, and contract manufacturing partnerships that shift capital intensity off the balance sheet.

- Embed reimbursement and clinical pathways for specialty indications. Although at-home devices remain broadly cosmetic and out of scope for routine health payers, certain clinical use-cases (e.g., gender-affirming care, selected dermatologic indications) may qualify for medical billing under specific CPT codes for professional procedures. Firms with the capability to support clinician partnerships and generate clinical evidence can create differentiated channels and institutional demand.

- Consider consolidation and strategic partnerships. Market concentration metrics indicate a market with room for scale effects — the top three firms control a meaningful share, while the top five increase that concentration further. For many mid-sized players, the pragmatic route to scale in 2026 will be through partnerships (technology licensing, distribution alliances) or targeted M&A focused on capability expansion (clinical-grade lasers, cooling patents, service platforms).

Competitive landscape — players to watch and where they compete

The market is populated by global consumer-electronics incumbents and specialist laser/beauty device firms. Leading players we profile in depth in the report include Philips (Lumea series with SkinAI and multi-attachment ecosystems), Braun (Silk Expert Pro series with SensoAdapt skin tone sensing), Tria Beauty (clinical-grade diode laser products), Ulike (cooling-enhanced IPL devices), Cyden Ltd / SmoothSkin, Remington and Silk’n. Each brings a distinct positioning — from clinical-grade efficacy to mass-market convenience and affordability — and each pursues different channel strategies, from pharmacy shelf presence to D2C subscription ecosystems.

Recent industry events in 2025 (notably multiple 510(k) clearances for new IPL home-use devices) have lowered barriers for certain China-based and OEM manufacturers to enter developed markets, increasing competitive pressure on pricing and innovation cadence. Our analysis profiles product roadmaps and patent exposure for these players, highlighting areas where incumbents retain moats (brand, distribution, regulatory expertise) and where challengers have first-mover advantages (cost-engineered platforms, comfort technologies).

Risk map and scenario planning

- Regulatory tightening. A more conservative regulatory posture or additional post-market surveillance requirements would increase product development costs and delay market entry.

- Raw material and component shocks. Escalating plastics or semiconductor prices could compress margins if not mitigated by pricing power or cost engineering.

- Consumer safety incidents. Publicized adverse events or recalls could depress demand and invite stricter regulation.

- Technology substitution. Rapid improvements in compact clinical lasers or adjunct at-home therapies could shift competitive advantage away from mature IPL platforms.

- Distribution disruption. Changes in ad platforms, marketplace policies, or retail consolidation could materially affect acquisition economics.

For each of these scenarios, the report provides quantified impact ranges, mitigation playbooks and trigger-based response templates so leadership teams can operationalize contingency plans without losing growth momentum.

How teams should use this report in 2026

- CMOs: Recalibrate acquisition mixes toward lower CAC channels and test subscription-based replenishment for consumables.

- Chief Product Officers: Prioritize one clinical-grade and one comfort/price variant; validate with a phased regulatory submission strategy.

- Heads of Supply Chain: Lock multi-year component agreements, build dual-sourcing for critical parts, and model localized assembly options.

- Corporate Development: Target tuck-in acquisitions that close capability gaps (clinical evidence, cooling IP, D2C CRM platforms) rather than revenue chases.

- Regulatory & Clinical Affairs: Maintain an active 510(k) clearance calendar and invest in post-market data collection to speed label-enabling claims.

Readiness checklist — key KPIs to monitor in the next 12 months

- Regulatory pipeline milestones (pre-submission meetings, submission dates, expected 510(k) decision windows)

- Sales velocity by channel and cohort-level CAC/LTV

- Gross margin sensitivity to commodity price moves

- Customer retention and consumable attach rates

- Product return and complaint ratios (safety early-warning)

PW Consulting’s full report contains the detailed datasets, segmented forecasts, competitor scorecards, regulatory dossier timelines and executable 100–150 day playbooks that boards and operating teams can act on immediately. This article surfaces the strategic arcs and headline economics (including the market’s seven-year trajectory at a ~7.2% CAGR) to help leaders prioritize questions to bring into 2026 planning sessions.

Next steps

Executives seeking the granular segment breakdowns, downloadable financial models, and the complete competitive dossiers should consult the full PW Consulting report to access the underlying tables, methodology notes and proprietary scenario models. The full study is structured to be directly usable in 2026 operating plans, investor decks and M&A diligence.

For detailed analysis of this topic, please visit the official page:At Home Hair Removal Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com