Adhesive Equipment Market Size, Share, Driving Trends, and Industry Forecast by 2032

Other |

2026-06-30 13:43:22

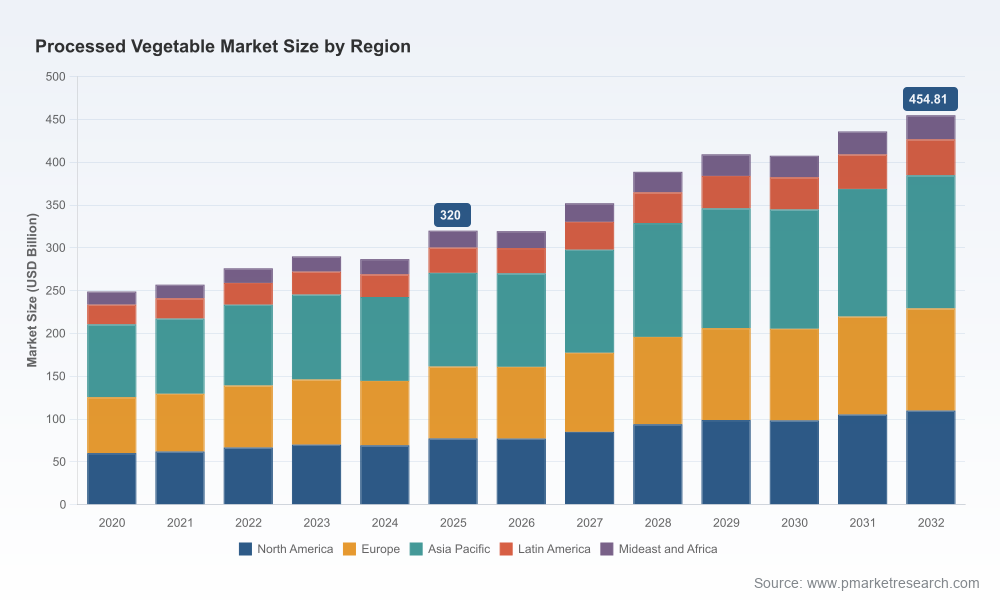

PW Consulting’s latest Processed Vegetable Market report frames the strategic choices facing manufacturers, retailers, ingredient suppliers, and investors as they enter 2026. The global processed-vegetable market demonstrated resilient expansion through the early 2020s—rising from approximately USD 249 Billion in 2020 to roughly USD 320 Billion in 2025—and our forward-looking model projects a sustained recovery and structural growth through the forecast window. Over the 2026–2032 period the market is forecast to expand at a compound annual growth rate (CAGR) of 5.15%, reaching an estimated USD 455 Billion by 2032.

Processed Vegetable Market

This release is designed as a strategic “preview trailer”: it surfaces the insights, tactical frameworks, and priority actions that will matter for 2026 corporate planning while directing practitioners to the full report for the granular regional, channel and SKU-level intelligence that underpins investment, sourcing, and product decisions.

Processed Vegetable Market

Macroeconomic clarity: We combine historical tracking (2020–2025) with scenario-driven forecasts to reconcile near-term volatility with longer-term demand vectors. The 5.15% CAGR is not merely a headline—it is the synthesis of price dynamics, consumption shifts, and capacity adjustments that will determine return profiles for the next wave of capital allocation.

Processed Vegetable Market

Practical prioritization: The report is explicitly built to inform board-level and operating-level decisions. Each chapter moves from insight to implication to recommended action—so that procurement, R&D, commercial and M&A teams can convert analysis into 90–180 day plans.

Competition and concentration lens: With measured market concentration at the national and global levels, we assess where scale matters and where modular, regional plays can win. Our concentration metrics provide a diagnostic for consolidation risk, pricing power and private-label opportunity.

Strategic frameworks: Playbooks for capacity planning, category prioritization and cross-channel portfolio optimization that map directly to P&L levers.

Supply-side diagnostics: Risk heatmaps for procurement, including supplier concentration, seasonality and sourcing-cost elasticity models that translate raw-material volatility into actionable hedges and contract terms.

Channel strategy templates: Segmented go-to-market options for retail, food service and industrial clients—each with margin and promotional-sensitivity scenarios to guide assortment and pricing decisions.

Regulatory and food-safety rulebook: Compliance roadmaps and quick-win controls addressing additive restrictions, labelling changes and recall mitigation techniques.

M&A and corporate-development playbook: Deal-screening filters, synergy-conversion models and integration checklists tailored to the processed-vegetable value chain.

Data annex: Time-series market sizing, demand-driver decomposition and scenario-based forecasts. Note: detailed regional and application-level tables are reserved for subscribers to preserve the value of the full dataset.

Several converging trends create both risk and runway for companies in this sector:

Raw-material inflation and farm economics: Public forecasts show fresh-vegetable price pressure into 2026, which will transmit to processors through higher procurement costs and margin compression for sellers who cannot fully pass on increases. Operationally, this elevates the importance of flexible sourcing and procurement contracting.

Regulatory tightening and food-safety vigilance: A wave of state-level restrictions on certain food additives and a notable number of recalls in 2025 highlight the need for stricter ingredient governance, faster traceability and clearer consumer communications.

Trade and tariff complexity: New tariffs and retaliatory measures in certain North American corridors have changed cross-border economics—forcing companies to reassess import/export strategies, nearshoring and inland processing footprints.

Consolidation, but with room for regional plays: Market concentration metrics indicate modest aggregation among the largest players, yet the landscape still provides entry points for well-capitalized or vertically integrated challengers—especially where local sourcing, branded differentiation or private-label scale can be achieved.

The sector combines global manufacturing leaders with specialized regional processors. Key strategic positions and recent events have altered competitive dynamics entering 2026:

Incumbent branded players maintain global shelf presence and established logistics networks. Their advantages include scale procurement, recognized brands and retail relationships—useful for defending premium segments and national promotions.

Specialist frozen and fresh-processed groups continue to focus on quality, category innovation and B2B relationships with foodservice and industrial processors. These players often compete on freshness, speed-to-market and technical processing capabilities.

Recent deal activity has repositioned several portfolios. A notable transaction in early 2026 resulted in the acquisition of packaged-vegetable assets by an established global supplier, reflecting opportunistic M&A activity amid chaptered restructurings. This type of asset-level consolidation will create new competitive configurations and integration challenges for buyers and sellers alike.

Bankruptcy and asset sales experienced in the most recent cycle created distressed-asset opportunities—both for buyers seeking immediate scale and for market entrants aiming to secure processing capacity at favorable economics. These transactions warrant careful diligence around legacy liabilities and supply agreements.

Companies that treat 2026 as a year to convert defensive measures into offensive advantage will outperform. PW Consulting recommends five priority moves to embed now:

Hedge and diversify procurement: Shift from single-source, spot-driven buying to blended contracts that include index-linked clauses, fixed-price tranches and victory-by-volume off-take agreements with growers. Where possible, institute supplier scorecards tied to yield, traceability and contingency capacity.

Operational resilience via modular capacity: Invest selectively in modular or co-located freezing and canning capacity that can be scaled up on seasonal peaks or repurposed between retail and foodservice pack sizes. This reduces penalty costs when raw-material prices spike or when trade flows are disrupted.

Regulatory-first product design: Revisit formulations and labelling to anticipate additive restrictions and to limit recall exposure. Faster in-house or third-party testing and batch-level traceability platforms reduce time-to-response and limit reputational and financial fallout.

Win in private label and value tiers: Retailers will increasingly shift premium shelf-space to brands while expanding cost-sensitive private-label offers. Processors should develop dedicated SKUs and supply streams for private label that protect branded margins.

M&A with integration discipline: Pursue bolt-on deals that add processing geography, cold-chain capability or proprietary packaging technology—but only with pre-defined synergy capture roadmaps and independent downside scenarios that assume extended price volatility.

Board workshops: Use the market sizing and concentration metrics to stress-test strategy and to set guardrails for capital allocation. Our interactive scenarios help boards choose between growth and margin preservation.

Commercial sprint plans: Translate channel templates into 90-day pilots—test private-label bundles, streamlined SKUs for foodservice and a limited assortment of innovation SKUs that align with cleaner label trends.

Procurement and supply-chain war room: Establish a cross-functional task force to implement hedging, supplier diversification and a prioritized capital plan for modular capacity.

M&A diligence checklist: Use the report’s deal-screen filters and integration playbooks as a pre-deal governance layer to avoid paying for speculative synergies.

This preview synthesizes the high-level market trajectory, core structural dynamics and priority actions for 2026. The full PW Consulting report contains the detailed regional, channel and type-level splits, SKU-level price elasticities, proprietary supplier-risk scores and an annex with scenario-based P&L impacts—information we intentionally reserve in the full release to preserve the integrity of the dataset and to enable tailored client engagements.

Senior executives, corporate development teams and institutional investors who require the granular tables, supplier-level risk dossiers or a custom briefing can access the full report and bespoke advisory services through PW Consulting’s client portal. The full deliverable includes downloadable datasets and an executive workshop package designed to convert insight into implementation within 60 days.

The processed-vegetable sector enters 2026 with a blend of structural growth and tactical disruption. For organizations that apply disciplined procurement, targeted capacity investments, and regulatory-aware product design, the market’s mid-single-digit CAGR represents an opportunity to convert operational resilience into share and margin expansion. PW Consulting’s complete report is designed to be the operational playbook for converting those macro trends into executable moves—book a briefing to see the detailed maps and decision frameworks that underlie our forecast.

For detailed analysis of this topic, please visit the official page:Processed Vegetable Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com