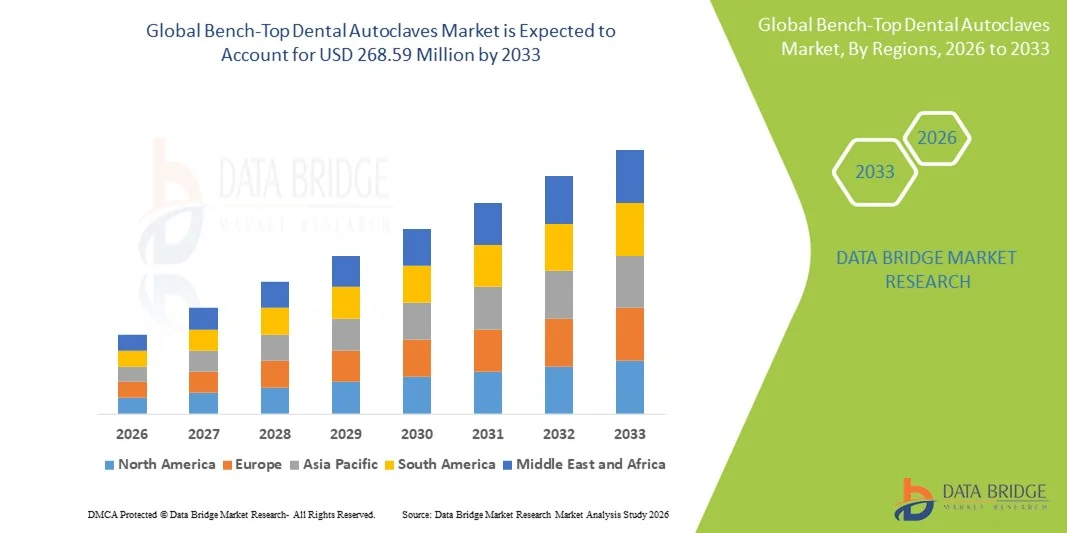

Bench-Top Dental Autoclaves Market Size, Share, Driving Trends, and Industry Forecast by 2033

Other |

2026-06-23 08:04:26

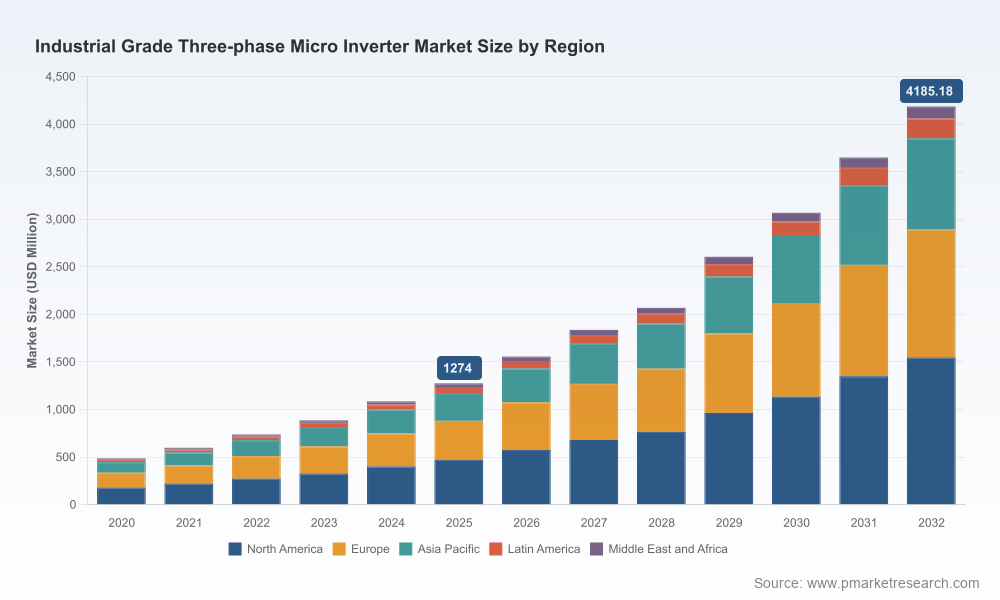

PW Consulting’s latest market intelligence on the Industrial Grade Three‑Phase Micro Inverter Market delivers a concise, actionable framework for corporate and investor decision‑makers preparing strategy for 2026 and beyond. Built on a rigorous 2020–2025 historical baseline and a 2026–2032 forecast horizon, the study quantifies a fast‑moving market that is expected to compound at a robust 18.52% CAGR. By 2025 the market has matured into an identifiable commercial segment and is forecast to expand materially through 2032, underscoring an inflection point for procurement, manufacturing localization, and technology investments.

Industrial Grade Three Phase Micro Inverter Market

Timing: 2026 is the year when regulatory nuances, domestic content rules and grid‑code evolution hit procurement cycles for commercial and industrial (C&I) solar projects. Our report maps those turning points to vendor readiness and supply chain options.

Industrial Grade Three Phase Micro Inverter Market

Market scale and trajectory: With the market already past a key maturity threshold in 2025 and forecast to more than triple by the end of the 2026–2032 forecast window, the opportunity is both large and time‑sensitive — requiring immediate strategy adjustments in sourcing, product roadmaps, and go‑to‑market models.

Industrial Grade Three Phase Micro Inverter Market

Concentration and competitive posture: The sector exhibits a high level of concentration among leading vendors. PW Consulting quantifies market concentration and competitive dynamics to help executives evaluate partnership, M&A and pricing strategies.

Validated market sizing and growth model (2020–2025 historical; 2026–2032 forecast) with sensitivity analysis across price, module size, and deployment scenarios.

Supply‑chain and manufacturing view that flags critical inputs (including the role of GaN semiconductors) and supply risk vectors that could affect lead times and total landed cost.

Regulatory and grid‑integration playbook — how IEEE 1547 / UL 1741‑SB compliance, evolving grid‑support requirements, and domestic content / Foreign Entity of Concern (FEOC) rules are reshaping procurement choices for C&I buyers.

Technology deep dive: comparative assessment of silicon vs GaN power stages, system efficiency tradeoffs, thermal management implications for rooftop and containerized C&I installations, and module‑level power electronics (MLPE) integration strategies.

Commercial implementation guidance: sample TCO models, dispatch and visibility requirements for behind‑the‑meter controls, and best practices for installer and O&M workflows at scale.

Competitive landscape with vendor profiles and go‑to‑market scorecards — strengths, strategic openings, and blue‑ocean niches for new entrants.

Regulatory friction and domestic sourcing: Several jurisdictions have tightened domestic content and FEOC rules for C&I solar assets. Our analysis demonstrates how compliance incentives and eligibility criteria materially affect vendor selection and the economics of retrofit vs greenfield projects in 2026.

GaN adoption and efficiency premiums: Leading suppliers are shipping GaN‑based three‑phase microinverters that claim peak efficiencies approaching 97.5%, yielding lower thermal envelopes and smaller form factors. The report quantifies the potential lifecycle savings and integration tradeoffs of GaN adoption across common commercial deployments.

Grid support and firmware agility: Modern three‑phase microinverters increasingly must provide advanced grid services and remote update capability to stay compliant and future‑proof. We map firmware governance and OTA (over‑the‑air) strategies against utility interconnection test cases.

Consolidation and concentration: The market shows significant concentration at the top. PW Consulting provides CR metrics and interprets what a concentrated supply base means for pricing power, innovation incentives, and strategic bargaining for system integrators.

Our vendor review covers incumbent specialists and emerging challengers across North America, Europe and Asia. The report features in‑depth profiles and capability assessments for market actors including high‑visibility innovators and regional suppliers. Examples of notable developments covered:

Enphase Energy (Fremont, California) — advanced commercial three‑phase offerings with GaN‑based products for 480Y/277V systems; recent commercialization activity has increased attention on domestically manufactured solutions for FEOC‑sensitive procurement pools.

APsystems — a multi‑module, commercial‑grade microinverter supplier focused on quad‑module and high‑voltage three‑phase applications.

Hoymiles — high‑power three‑phase solutions targeted at large rooftop and C&I use cases, with multi‑module integrated topologies and reactive power control functions.

Deye, Chilicon Power and European specialists — a mix of integrated inverter vendors and MLPE experts offering options for different project risk profiles and channel strategies.

Each vendor profile in the full report includes product roadmaps, manufacturing footprints, compliance posture, and a recommended engagement model for procurement teams. We deliberately summarize vendor capabilities here while withholding granular market share and revenue splits to preserve competitive context — the full vendor scorecards are available in the report package.

Procurement playbook: Build conditional purchase agreements that account for domestic content eligibility and certification timelines. For FEOC‑sensitive tenders, prioritize vendors with demonstrable US manufacturing and transparent supply‑chain audits.

Technology investment: Allocate R&D or capex to GaN‑enabled product lines where efficiency and form factor deliver quantifiable balance‑sheet benefits; but validate expected reliability through accelerated life testing before large‑scale adoption.

Partnerships and alliances: Consider strategic agreements with MLPE specialists or local manufacturing partners to secure capacity and to qualify for procurement incentives tied to local content rules.

Risk and compliance: Institute firmware governance, cybersecurity and OTA update protocols aligned to IEEE 1547 and UL 1741‑SB expectations to minimize interconnection delays and post‑commissioning outages.

M&A and investment screening: Use the report’s concentration and valuation lenses when assessing bolt‑on acquisitions or minority investments — consolidation dynamics are likely to favor scale players with demonstrated C&I track records.

Decision‑grade forecasting: Our market model gives buyers and suppliers the near‑term runway to lock in manufacturing and procurement strategies tied to realistic deployment schedules and price elasticity assumptions.

Negotiation intelligence: The report supplies scorecards that translate vendor technical claims into procurement levers — warranty structures, lead‑time protections, and performance guarantees you can negotiate from day one.

Implementation templates: We include sample RFP language, qualification checklists for MLPE, and O&M transition plans tailored to C&I integrators and asset owners.

To preserve the strategic value of the full research package, this release outlines high‑level sizing, growth parameters and vendor dynamics while omitting granular regional, application and channel share tables that form the core of competitive intelligence. PW Consulting’s full report contains detailed segmentation matrices, region‑by‑region deployment scenarios, and per‑vendor revenue splits that are essential for competitive benchmarking and bid preparation. Prospective clients and program teams are encouraged to access the full package for those defensible, transaction‑ready details.

For executives planning capital allocation, supplier selection or M&A activity in 2026, the Industrial Grade Three‑Phase Micro Inverter segment represents an inflection-rich opportunity: rapid growth, technology transitions (notably GaN uptake), and regulatory reshaping of procurement criteria. PW Consulting’s report translates these forces into an executable playbook — from sourcing and product decisions to compliance and integration blueprints. With market growth modeled at an 18.52% CAGR and demonstrable concentration among leading vendors, the right strategic moves in 2026 will yield outsized benefits through the forecast window.

To obtain the full report — including the complete segmentation, per‑vendor scorecards, and downloadable models for procurement and TCO — please visit our report page or contact PW Consulting’s industrial energy team for a briefing tailored to your organization’s priorities.

For detailed analysis of this topic, please visit the official page:Industrial Grade Three Phase Micro Inverter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com