Advanced Insulation Materials: 2026 Strategic Brief — New PW Consulting Market Research Report

PW Consulting today publishes a strategic briefing derived from its forthcoming Advanced Insulation Material Market Research report — an evidence-driven compass for C-suite leaders, corporate strategists, and investors planning for 2026. The briefing synthesizes multi-year market performance, supplier dynamics, regulatory inflection points and practical playbooks to translate market data into actionable decisions. Consider this a high-level trailer: we reveal the directional analytics and strategic implications while reserving granular segmented datasets for report subscribers who require the complete modelling and downloadable databases.

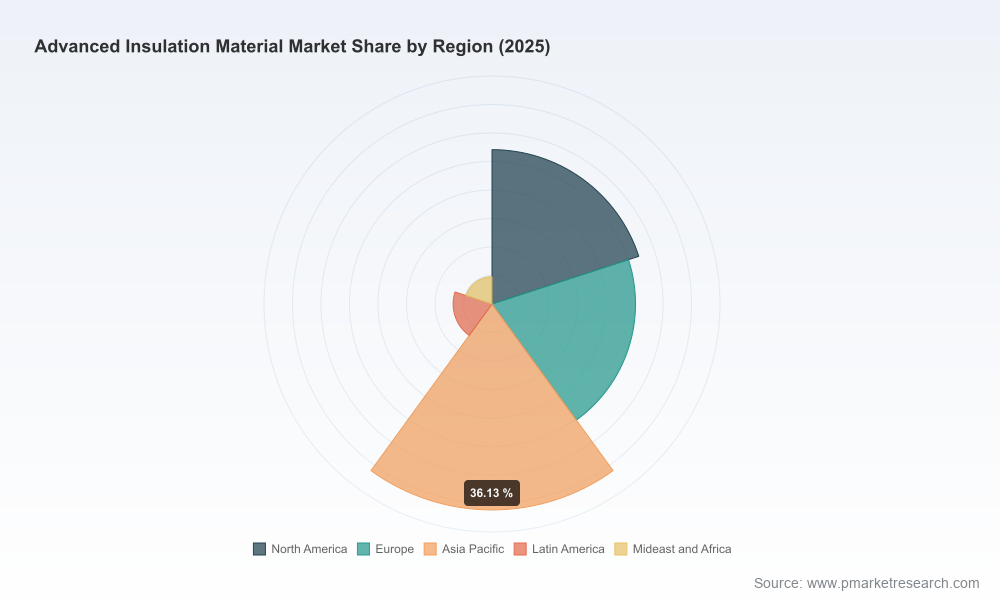

Advanced Insulation Material Market Research

Why 2026 is a Pivotal Year

The advanced insulation sector has moved from niche engineering curiosity to strategic industrial priority. The global market expanded from roughly USD 10.2 Billion in 2020 to USD 15.25 Billion in 2025, reflecting accelerating decarbonization agendas, building-energy retrofits and high-growth end markets such as EV thermal management and subsea energy infrastructure. Looking forward, we project a sustained expansion through the forecast window (2026–2032) at a compound annual growth rate (CAGR) of approximately 9.24%, with the total market exceeding USD 28 Billion by 2032.

Advanced Insulation Material Market Research

For 2026 planning cycles, this trajectory creates three simultaneous imperatives for commercial and operational leaders: navigate input-cost volatility; align product portfolios with tightening regulatory thresholds; and reassess go-to-market footprints given tariff and logistics pressures. Our report dissects each imperative with scenario-based financial modelling, supplier maps, and investment decision trees that executives can deploy directly in boardroom discussions.

Advanced Insulation Material Market Research

What the Report Delivers — Practical, Transaction-Ready Content

- Forward-looking market model: A calibrated, bottom-up market-sizing engine covering 2020–2032 with downloadable revenue curves, sensitivity testing and scenario toggles for raw material shocks and regulatory adoption rates.

- Price and cost battlegrounds: Rolling cost-impact simulations integrating recent feedstock trends (including the polyol price surge observed in late 2025) and transport surcharges to quantify margin risk across product families.

- Regulatory playbooks: Compliance checklists and staged product roadmaps to meet emergent standards (including new thermal conductivity requirements and restrictions on high-GWP blowing agents), with suggested certification timelines and third-party testing partners.

- Supplier and ecosystem maps: Tiered supplier assessments highlighting capacity, technology specialization and strategic levers—designed for procurement teams evaluating dual-sourcing, localization or backward integration strategies.

- M&A and partnership canvases: Target screening filters, valuation comparables and integration risk matrices tailored to both incumbent materials manufacturers and advanced-technology entrants (e.g., aerogel producers and phase-change solution providers).

- Commercial playbooks: Pricing playbooks, channel segmentation approaches, and account-based strategies for critical verticals such as buildings, energy and transportation.

- Operational readiness templates: Capex prioritisation frameworks, modular capacity-expansion blueprints, and time-to-market checklists for product launches under new regulatory regimes.

Competitive Landscape — Who Moves the Market

The advanced insulation market is moderately concentrated: the top three firms account for approximately 32.4% of industry revenue, while the top five reach nearly 48.6%. This concentration profile creates both stability in supply for buyers and opportunities for differentiated players to capture attractive niche margins.

- BASF SE (Ludwigshafen, Germany) — A broad-based chemical major, BASF leverages scale in polymeric technologies and foam systems for building and industrial markets. Recent capacity expansions for expandable polystyrene at its Ludwigshafen site underline a readiness to defend volume leadership where commoditized foam demand persists.

- Dow Inc. (Midland, Michigan, USA) — Dow’s portfolio focus on polyisocyanurate (PIR) systems and insulating sealants positions it as a materials innovator for construction and HVAC. Its visible product showcases indicate an intensified push toward higher-performance PIR formulations that balance thermal efficiency with manufacturability at scale.

- Saint-Gobain (Courbevoie, France) — With traditional strengths in mineral wools and a growing aerogel-based toolkit, Saint-Gobain is aligning sustainability credentials with product differentiation; recent sustainability certifications demonstrate competitive advantage in public tendering and specification-heavy projects.

- Rockwool, Knauf, Kingspan, Owens Corning — These incumbents combine legacy channel reach in building insulation with targeted R&D in acoustics, fire performance and low-conductivity cores, enabling them to defend share in commercial construction while exploring premiumization.

- Aerogel and specialty players (Aspen Aerogels, Cabot Corporation, Armacell) — Niche technology providers are converting laboratory advantages into commercial applications: recent product launches aimed at EV battery thermal management and cryogenic applications illustrate how technology-led entrants can create new addressable markets.

Recent industry moves underscore how competition is being fought on multiple fronts: Aspen Aerogels launched an EV-optimized aerogel product in October 2025, while BASF expanded EPS capacity in September 2025. Saint-Gobain’s Cradle to Cradle certification in mid-2025 signals that sustainability credentials are becoming a procurement differentiator, and Rockwool’s new façade-grade slab highlights acoustic/architectural functionality as a product battleground.

Market Dynamics and Strategic Implications

Five cross-cutting dynamics will most directly shape strategic choices in 2026:

- Feedstock volatility: Polyol and other petrochemical feedstock swings materially affect foam economics. The report’s cost-sensitivity module translates a 10–20% feedstock shock into margin and pricing scenarios for flagship product lines.

- Regulatory tightening: New thermal-performance thresholds and restrictions on high-GWP blowing agents require product reformulation and certification. We provide staged compliance timelines so product development, regulatory and commercial teams can synchronize go-to-market plans without revenue leakage.

- Trade and logistics friction: Tariffs on certain imports and higher trans-Pacific freight surcharges increase the attractiveness of local production or strategic inventory positioning. Our regional scenarios quantify breakeven points for nearshoring versus import strategies.

- Technology bifurcation: The market is splitting between cost-optimised bulk solutions (boards, foams, mineral wools) and performance-differentiated advanced materials (aerogels, vacuum panels, phase-change systems). Each segment requires distinct commercialization and margin models that we map in the report.

- Buyer sophistication: Large integrators and public projects increasingly specify low-conductivity targets and lifecycle CO2 metrics, elevating the value of certified, higher-price solutions. Our tender-readiness checklist helps commercial teams convert specification complexity into premium pricing.

Strategic Playbook — Where Executives Should Focus in 2026

- Prioritise a dual-supplier strategy for critical feedstocks — Use our supplier heatmaps to identify alternative polyol and silica supplies and build contingency stock policies tied to cost thresholds.

- Accelerate product reformulation for regulatory parity — Allocate R&D sprints and pilot production slots to replace high-GWP blowing agents and meet stricter thermal conductivity requirements in priority markets.

- Localise selectively — Evaluate nearshoring for aerogel and other high-value components where tariffs and shipping surcharges materially erode landed cost; our breakeven models provide decision gates.

- Pursue modular manufacturing expansions — Opt for flexible, smaller-scale capacity additions to reduce time-to-market risk while retaining optionality; our capex templates show ROI sensitivities under different demand-growth scenarios.

- Monetise certification and sustainability — Turn lifecycle credentials into margin by reshaping commercial terms, especially in public tenders and large-scale retrofit programs.

- Scan for bolt-on tech acquisitions — For incumbents seeking performance upgrades, targeted acquisitions of aerogel producers or PCM specialists can be accretive; we include screening criteria and integration checklists.

How to Use This Briefing

Consider this briefing a strategic orientation kit for 2026 planning. PW Consulting’s full report includes the exhaustive datasets, regional and application splits, product-level economics, and downloadable Excel models that underpin the scenarios summarized above. Clients receive access to an interactive dashboard allowing bespoke sensitivity analyses (e.g., tariff hikes, raw material shocks, certification lag) and a tailored advisory session with our industry practice to convert findings into a prioritized action plan.

We deliberately withhold detailed segmented percentages and downloadable datasets in this public release to preserve the integrity of the model and to ensure clients who need transaction-ready intelligence receive the full analytical suite. For procurement directors, innovation leads and M&A teams, the value lies in the combination of granular data and PW Consulting’s strategic playbooks — precisely what the full report delivers.

Next Steps

- Request a briefing: Schedule a tailored walkthrough where we map the report findings directly to your portfolio or geographic exposures.

- Commission a rapid scenario: Engage PW Consulting for a 4–6 week deep-dive (market sizing + supplier diligence + regulatory readiness) to produce a board-ready decision memo for 2026 capex or M&A deliberations.

- Subscribe for the full report: Access the model, data tables, vendor scorecards and procurement-ready templates.

PW Consulting’s Advanced Insulation Material Market Research is designed to convert market complexity into executable strategy. In an industry marked by regulatory shifts, feedstock volatility and rapid technology convergence, the right information — parsed into decision frameworks — becomes the decisive competitive advantage in 2026.

For detailed analysis of this topic, please visit the official page:Advanced Insulation Material Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com