Industrial Grade Ferric Chloride Market: Strategic Preview for 2026 Decisions

Executive summary

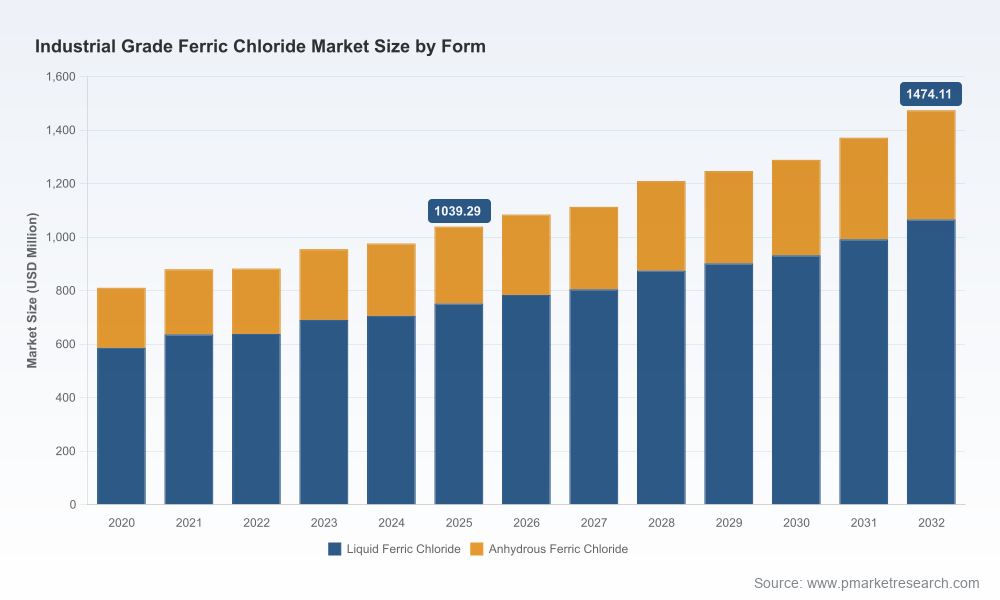

PW Consulting’s Industrial Grade Ferric Chloride Market report offers senior decision-makers a compact, actionable strategic compass for 2026. The global industrial ferric chloride market reached just over USD 1.03 billion in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of approximately 5.12% through the 2026–2032 horizon, approaching roughly USD 1.47 billion by 2032. These headline figures belie important structural shifts — in feedstock dynamics, regulatory intensity, and supplier concentration — that will define profitable options and risk exposures for manufacturers, distributors, and end‑users in 2026 and beyond.

Industrial Grade Ferric Chloride Market

Why this matters for 2026 planning

- Tactical procurement and inventory policy: With feedstock linkages to chlor‑alkali and steel markets, short‑term disruptions can create outsized effects on availability and delivered cost. 2026 procurement strategies must balance contract length, flexibility, and geographic sourcing.

- Regulatory compliance and product positioning: Ferric chloride’s role in drinking and wastewater treatment places certification and traceability at the center of commercial viability. Firms that deliver certified products and clear compliance documentation will retain pricing power in municipally regulated tenders.

- Competitive differentiation: The market exhibits mid-level concentration (CR3 ~41%; CR5 ~57%), implying meaningful room for regional players but increasing advantages for scale, integrated feedstock access, or premium certification.

Market dynamics shaping 2026 strategic choices

Three interconnected dynamics will most directly influence boardroom decisions next year: feedstock and production constraints, regulatory and end‑market demand drivers, and evolving supplier economics.

Industrial Grade Ferric Chloride Market

- Feedstock vulnerability and supply elasticity: Production of industrial ferric chloride commonly depends on inputs from chlor‑alkali processes (chlorine) and iron/steel sources. Reductions in chlor‑alkali capacity or swings in ferrous scrap availability historically compress supply windows and raise spot volatility. In 2026, buyers should model scenarios that incorporate both temporary plant outages and longer‑term shifts in chlor‑alkali capacity utilization.

- Regulatory tightening and treatment specifications: Ferric chloride is a preferred coagulant for phosphorus control and solids management in municipal and industrial wastewater treatment. Certifications such as NSF/ANSI Standard 60 remain gating factors for drinking water applications in many jurisdictions. Companies should prioritize product formulations, testing, and documentation pathways that facilitate rapid approval for public sector procurement.

- Demand base evolution: End markets are not monolithic. Municipal utilities, PCB and metal etching, paper/textile auxiliaries, and chemical intermediates each carry different margin, logistic, and specification profiles. The aggregate growth trajectory is steady but not uniform; targeted go‑to‑market plays in higher‑value applications will outperform commodity distribution models.

Segmentation: where to focus (without giving away the punchline)

The report dissects the market by form (liquid vs. anhydrous and hydrates), application (water and wastewater treatment, metal surface treatment/etching, drinking water, and chemical intermediates), and region. Each slice reflects distinct procurement cycles, regulatory touchpoints, and margin structures. For 2026, the most actionable intelligence lies in understanding which form‑to‑application pairings drive reliability of supply and margin resilience — details that PW Consulting provides in tabular and scenario formats in the full study.

Industrial Grade Ferric Chloride Market

Report highlights — practical deliverables for executives

Rather than abstract commentary, our report equips practitioners with implementation tools designed for immediate use in 2026 planning cycles. Key deliverables include:

- Five procurement playbooks aligned to common buyer profiles (municipal utility, large industrial user, regional distributor, contract etcher, chemical intermediary), with supplier scorecards and negotiation levers.

- Supply‑chain risk maps integrating chlor‑alkali and ferrous feedstock scenarios, outage sensitivity analyses, and contingency sourcing pathways.

- Regulatory pathway appendices covering certification timelines, test regimes, and documentation templates to support NSF/ANSI and equivalent approvals across major markets.

- Commercial modeling tools: price elasticity matrices, margin waterfall templates, and scenario‑based NPV outcomes for capacity additions or backward integration.

- Competitive playbooks including acquisition targets, partnership archetypes, and contract manufacturing options that reflect realistic consolidation pathways given current concentration metrics.

Competitive landscape: strategic takeaways

The market retains a blend of multinational incumbents, regional specialists, and cost‑focused producers. The competitive map shows mid‑to‑high fragmentation at the regional level but increasing clustering among global suppliers that have integrated chlorine access or multi‑site production footprints. For 2026, companies should evaluate three practical strategic postures:

- Scale and integration — Firms such as BASF and Kemira represent vertically integrated models, producing both solution and anhydrous forms and leveraging integrated chlorine feedstocks. These players can defend premium channels where feedstock control matters.

- Regional specialization — Producers like PVS Chemicals, Tessenderlo Group, and regional suppliers in Asia and the Middle East focus on proximity, certification for local utilities, and service models that reduce freight and delivery lead times.

- Cost and niche — Several manufacturers concentrate on export‑oriented capacity or specific high‑volume industrial etching markets; their value is price competitiveness and supply flexibility rather than brand premium.

Representative company notes included in the report (selection):

- PVS Chemicals (USA) — A North American-focused producer with multiple facilities and NSF/ANSI 60-certified formulations, positioning it strongly for municipal and industrial water segments.

- Kemira Oyj (Finland) — A global water‑treatment specialist offering multiple product forms and leveraging European and North American production presence; strategic advantage stems from broad treatment chemistry portfolios and customer relationships in municipal procurement.

- Tessenderlo Group (Belgium) — European producer supplying high‑purity grades for coagulation and sludge management, with strengths in technical service and supply reliability for utilities.

- BASF SE (Germany) — One of the remaining Western European producers capable of making anhydrous FeCl3 via integrated chlorine electrolysis, giving it an edge in applications demanding high‑purity anhydrous grades.

- Regional players (DCW, HOO CHEMTEC, SJCC, and several Indian and Middle Eastern manufacturers) — Compete on capacity, cost, and proximity, and in some cases hold certifications that support drinking water applications in their local markets.

Strategic recommendations for 2026

Based on our integrated analysis, PW Consulting recommends a prioritized action matrix for executives preparing 2026 plans:

- Short horizon (0–12 months): Secure conditional supply agreements with dual‑sourcing clauses; fast‑track certification dossiers for any product lines intended for potable water applications; and run stress tests on working capital to absorb spot volatility.

- Medium horizon (12–24 months): Evaluate investments in backward integration (chlorine access, captive iron feedstock), contract manufacturing arrangements, or long‑term offtake agreements with regional producers to lock in margins.

- Long horizon (24+ months): Consider strategic consolidation where scale translates to disproportionate procurement advantage or where cross‑selling opportunities exist between coagulants and adjacent water treatment chemistries.

Scenarios and what they mean for value creation

The report models three plausible scenarios through 2032: a baseline aligned with the stated CAGR, a constrained‑supply scenario driven by chlor‑alkali capacity reductions, and an accelerated demand scenario from tightening phosphorus discharge rules in key jurisdictions. Each scenario is translated into actionable P&L sensitivities and recommended tactical responses — for example, differential inventory policies, targeted certification investments, and M&A thresholds that preserve investor returns.

What the full report contains (practical table of contents)

- Executive summary and strategic implications for 2026

- Market sizing and forecast methodology (historical 2020–2025 and forecast 2026–2032)

- Segmentation analysis by form, application, and region (detailed tables and scenario outputs)

- Feedstock and production cost models with chlor‑alkali linkage analysis

- Regulatory and certification pathways, including compliance checklists

- Supplier benchmarking, CR3/CR5 concentration analysis, and company profiles

- Procurement playbooks and commercial negotiation templates

- Risk maps and contingency sourcing frameworks

- Appendices: data tables, assumptions, and primary research notes

Invitation to engage

This briefing is a strategic preview. It demonstrates the depth and practicality of PW Consulting’s analysis while deliberately withholding the granular subsegment figures and proprietary model outputs that are included in the full report. If your 2026 plan depends on defensible supplier choices, robust procurement playbooks, or evidence‑based M&A thresholds in the industrial grade ferric chloride market, access to the comprehensive dataset and model is essential.

Contact PW Consulting to obtain the full Industrial Grade Ferric Chloride Market report, including granular form‑by‑application tables, regional forecasts, primary supplier scorecards, and scenario modeling spreadsheets designed to be embedded directly into your 2026 planning workflows.

For detailed analysis of this topic, please visit the official page:Industrial Grade Ferric Chloride Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com