What Is Driving the Mequinol (MeHQ) Market Toward USD 245.3 Million by 2032 at a 5.2% CAGR?

Other |

2026-06-29 12:01:06

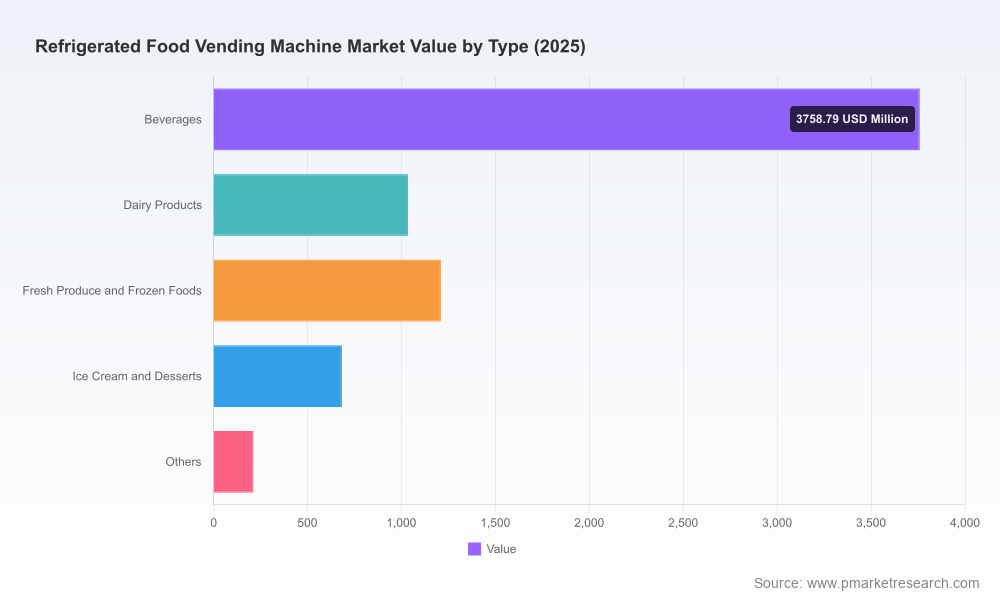

PW Consulting’s latest market study on Refrigerated Food Vending Machines delivers an evidence-based roadmap for executives making capital, product and channel decisions in 2026. The market has expanded rapidly over the past half-decade and now stands at an estimated USD 6.9 billion in 2025. Our forecast models show continued expansion at a compound annual growth rate of 7.5% through the 2026–2032 horizon, with the total market approaching USD 11.5 billion by 2032. That trajectory — driven by regulatory pressure, technology-enabled services and evolving foodservice distribution patterns — creates discrete windows of opportunity for OEMs, operators, food brands and investors who act with speed and operational rigor.

Refrigerated Food Vending Machine Market

Regulatory inflection points are now investment deadlines. The U.S. EPA’s AIM Act restrictions on high‑GWP refrigerants and the EU’s energy-labeling and efficiency requirements change not only product specifications but allowed go‑to‑market timing and retrofit economics.

Refrigerated Food Vending Machine Market

Technology and services are becoming the differentiator between thin-margin asset owners and high-value solution providers. RFID, telemetry, AI-enabled inventory forecasting and touchscreen merchandizing are shifting revenue mix toward service fees, merchandising partnerships and data monetization.

Refrigerated Food Vending Machine Market

Supply chain and material choices will determine unit economics. Structural materials and refrigeration components influence reliability, lifetime energy consumption and total cost of ownership — factors that investors, corporate procurement and concession owners now prioritize.

Market structure is moderately fragmented: the top three vendors account for less than a third of industry value while the top five approach the low‑forties percentage range, leaving room for consolidation and specialized entrants.

Actionable market sizing and high‑granularity forecast models calibrated to 2025 base-year data and stress‑tested across three scenarios (baseline, accelerated adoption and regulatory-constrained).

Regulatory impact matrix detailing short-, medium- and long‑term implications of the EPA AIM Act and EU energy labeling rules on product portfolios, manufacturing lines and aftermarket services.

Technology and product roadmap recommendations that prioritize energy efficiency, refrigerant transitions and modular design for rapid upgrades.

Go‑to‑market playbooks for OEMs and operators (channel mix, financing/leasing models, loyalty and merchandising partnerships), including pilot templates for corporate campuses, transit hubs and retail chains.

Procurement and supplier-management toolkit: sourcing checklists, cost‑build templates, steel and component sensitivities and strategies to mitigate raw-material exposure.

Operational playbooks for fleet operators: service cadence, remote diagnostics integration, shrink & food-safety controls, dynamic replenishment algorithms and key performance indicators (KPI) dashboards.

Competitive benchmarking with vendor capability maps, M&A target screening criteria, and a prioritized watchlist for technology partnerships and bolt‑on acquisitions.

The vendor ecosystem spans legacy machine manufacturers, payment and telemetry specialists, and a growing wave of smart-device integrators. Our qualitative assessment highlights distinct capability clusters.

Crane Payment Innovations (formerly Crane Merchandising Systems) — U.S.-based systems integrator with strengths in merchandising, touchscreen UX and reliable refrigeration architectures. Their Merchant Media series illustrates the premium, integrated approach to combining media, payment and chilled merchandizing.

AMS Vendors — Focused on low‑temperature combo solutions and guaranteed-delivery systems. Their product strategy emphasizes reliability in combo food-and-beverage deployments — a logical fit for convenience and transit applications.

SandenVendo America — Supplier with a strong emphasis on energy-efficient refrigeration and commercial foodservice integration. Their portfolio addresses glass-front and frozen food applications where visibility and thermal performance matter most.

REDYREF — Emerging player focused on RFID-enabled smart fridges and inventory-aware kiosks. Recent deployments of smart food fridges for fresh meals underscore a trend toward contactless commerce and real-time stock management.

Azkoyen Vending Systems — European supplier with temperature‑specific solutions for perishable items; a strong regional foothold and a focus on regulatory compliance for cold-chain safety.

Seaga Manufacturing, Fuji Electric and TCN Vending — Represent a mix of North American, Japanese and Chinese capability bases. Their portfolios range from robust cold food combi machines to touchscreen-centric, adjustable cooling offerings — illustrating competitive pressures from both established and OEM-scaling international players.

Recent industry activity reinforces the technology-as-differentiator thesis. REDYREF’s 2025 RFID smart-fridge deployment and major trade shows in 2026 (notably the NAMA Show and Venditalia) showcased AI‑enabled coolers, micro‑market integrations and remote management systems. These public demonstrations are translating quickly into operator interest, especially for deployments that reduce shrink, improve replenishment efficiency and deliver branded meal programs.

EPA AIM Act enforcement altered the cost calculus for refrigerant selection and aftermarket servicing. OEMs that moved early to low‑GWP alternatives and retrofit pathways are now enjoying a first‑mover advantage; laggards face inventory write-down risk and retrofit cost burdens.

EU energy‑labeling rules (EN 50597-based standards) are raising the floor on acceptable energy consumption. Machines with outdated compressors or poor insulation face restricted market access in key jurisdictions unless upgraded.

Material dependencies matter. For example, specific steel grades are dominant in hot‑food structural components due to durability and thermal properties; procurement strategies that prioritize supply resilience and secondary sourcing for steel and refrigeration components will blunt near-term margin volatility.

OEMs: Accelerate product migration to compliant refrigerants, standardize modular refrigeration units for field retrofitability, and embed telemetry as default. Pursue energy‑efficiency upgrades that will be certifiable under leading regional labels.

Operators and Retail Chains: Pilot smart-fridge programs that bundle merchandising, loyalty and dynamic pricing; transition from pure-equipment procurement to service-based models (managed vending, revenue-share partnerships).

Food Brands & Foodservice Providers: Use vending as a low-friction channel for new SKUs and midday meal programs; co-invest in telemetry/data agreements to refine assortment and freshness metrics.

Investors & PE Sponsors: Target roll‑up strategies in regional OEMs that have IP in refrigeration retrofit kits or fleet‑management SaaS. Prioritize assets with demonstrable energy savings and recurring service revenue.

Public Sector & Facility Owners: Update procurement specifications to require energy-label compliance and refrigerant‑transparency; consider CAPEX support mechanisms for operators transitioning older fleets.

Use the report as both a decision-support engine and an execution kit. For strategic planning, run the included scenario models against your own installed base and capex pipeline to quantify retrofit versus replace decisions. For commercial execution, adopt the go‑to‑market playbooks to accelerate pilots and standardize vendor selection. For M&A or partnership diligence, leverage the vendor benchmarking and the M&A screening framework to prioritize targets by capability, compliance readiness and serviceable addressable market fit.

We intentionally present deep analytical rigor while preserving the commercial value of our proprietary segmentations and vendor scoring matrices — the detailed sub‑segment breakouts, company financial benchmarks and downloadable model files are available in the full report for clients and subscribers. That package includes spreadsheets, deployment checklists and an executable 90‑day pilot plan tailored to your role (OEM, operator, retailer or investor).

Contact PW Consulting to schedule a briefing and license access to the full Refrigerated Food Vending Machine Market report. For teams accelerating decisions in 2026, the right combination of regulatory foresight, product modernization and service innovation will separate winners from the incumbents that are left retrofitting under time pressure.

For detailed analysis of this topic, please visit the official page:Refrigerated Food Vending Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com