Release Paper Market Outlook 2026: Strategic Imperatives for Procurement, Product and Sustainability Leaders

PW Consulting’s latest Release Paper Market Release Paper Market Release Paper Market (Base year: 2025) synthesizes commercial intelligence and scenario-driven strategy to help executives make higher-confidence decisions in 2026. This Release Paper Market snapshot distils why release liners and coated paper substrates are no longer a niche supply challenge but a cross-functional strategic lever—impacting packaging design, cost-to-serve, regulatory compliance and circularity roadmaps.

Release Paper Market

Market Snapshot: What the headline numbers mean for strategy

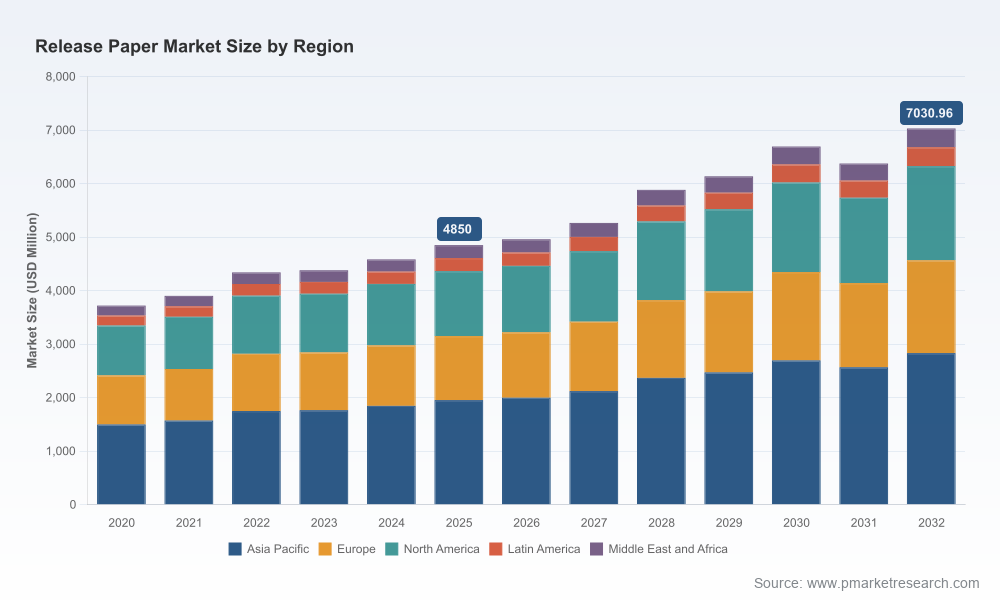

The global release paper and liner market has moved from the low billions in 2020 to an estimated USD 4.85 billion in 2025, and our forecasted trajectory drives the market toward slightly above USD 7.0 billion by 2032, reflecting a mid-single-digit compound annual growth rate (CAGR) of approximately 5.45% across the 2026–2032 horizon. Market concentration remains low: the top three firms account for roughly one-fifth of global revenues and the top five under one-third—a structural signal of fragmentation and opportunity for differentiation.

Release Paper Market

For 2026 decision-makers, these headline dynamics translate into three simple strategic facts:

Release Paper Market

- Stable, predictable base demand: growth is steady enough to justify multi-year sourcing and sustainability contracts but not homogeneous across product types or geographies.

- Fragmentation creates supplier power shifts: buyers can engineer competitive tension, while focused suppliers can win via specialized capabilities (sustainable coatings, on-site recycling, regional service networks).

- Regulation and raw material volatility materially affect cost pass-through, product design and recycling feasibility—making scenario planning essential for procurement and innovation teams.

The practical value of this Release Paper Market report to 2026 decision-making

We designed this Release Paper Market report as a practical playbook for procurement directors, packaging leaders, investors and sustainability officers. The full report combines market sizing and forecasting with ready-to-apply tools—without overwhelming readers with raw segmentation tables on the homepage. Highlights include:

- Actionable supplier scorecards and a five-factor sourcing framework that lets procurement run rapid supplier selection exercises tailored to sustainability, lead time, and cost-to-serve priorities.

- Cost-pass-through and inflation sensitivity models calibrated to recent pulp and kraft price behaviours, enabling finance teams to stress-test supplier contracts under plausible raw-material scenarios.

- Decision trees for paperization vs. film substitution that incorporate recyclability, EPR requirements and manufacturing constraints to guide packaging SKU rationalization.

- Operational playbooks for recycling and circularity pilots—covering waste collection flows, pre-treatment options, co-processing, and partnerships with reclaimers—tuned to the technical realities of silicone coatings.

- M&A and JV screening checklists that prioritize capabilities (e.g., silicone application expertise, reclaiming tech, regional capacity) aligned to three plausible 2026–2028 market scenarios.

- Risk matrices and mitigation templates for regulatory developments (EPR schemes, recyclability mandates) and supply disruptions caused by raw-material price spikes or localized capacity additions.

Competitive landscape: how leading players are positioning for 2026

The Release Paper Market remains a mix of integrated paper manufacturers, specialty liner producers, and adhesive-system suppliers. Our qualitative assessment of industry leaders reveals three recurring strategic plays:

- Scale and vertical integration to secure raw materials and control cost-to-serve (exemplified by diversified pulp and specialty paper producers).

- Sustainability and circularity initiatives—investing in recyclable substrates, recycled feedstocks and partnerships to reclaim silicone-coated waste.

- Service differentiation through regional footprint expansion and tailored coating technologies for labels, tapes and packaging applications.

Key companies profiled in the report and their strategic postures include:

- Loparex LLC (USA): a specialty-focused liner producer emphasizing direct-coated and poly-coated paper release liners for demanding label and graphic applications. Their strength lies in tailoring substrate-coating pairings to production lines—an advantage for converters seeking reduced waste and higher yields.

- Ahlstrom (Finland): positions itself as a fiber-based, sustainability-first supplier. Its investments in release base papers and coated materials align with brand owners prioritizing recycled content and lower lifecycle footprints.

- Mondi Group (Austria/UK): has combined product innovation with recent capacity investments and cross-industry circularity initiatives, signalling an integrated approach to sustainable packaging and liner reuse.

- UPM Raflatac / UPM (Finland): focuses on recyclable, paper-based liner alternatives and labelstock integration—attractive for consumer-packaged-goods (CPG) firms under tight recyclability mandates.

- Avery Dennison and 3M (USA): both leverage broad adhesive and materials portfolios to couple release liners with pressure-sensitive systems—winning where technical integration and conversion reliability matter most.

- Regional specialists and film-centric players (e.g., Polyplex, LINTEC, Gascogne, Sappi, Felix Schoeller, and several Asia-based producers) continue to compete on cost, local service and flexible substrate offerings—important options for converters seeking regional resilience.

Recent corporate activity underscores these themes—Mondi’s facility opening in the U.S. (2026) to support eCommerce and industrial packaging demand, and earlier collaborations to increase circularity in siliconized and coated paper waste—are practical examples of firms moving from rhetoric to operational change. Similarly, trade exhibitions and new barrier formulations introduced by chemical partners indicate accelerating technology transfer aimed at enabling "paperization" of traditional film applications.

Regulation, raw materials and operational risk: what you need on your 2026 radar

Three external dynamics will disproportionately shape viable strategies this year:

- Regulatory push toward EPR and recyclability. Jurisdictions, particularly in the EU and select U.S. states, have tightened packaging responsibility rules, increasing the commercial benefits for recyclable paper-based liners—and the penalty for ignoring end-of-life costs.

- Recycling technology mismatch. Many paper-based release liners remain technically challenging to recycle at scale due to coatings; industry pilots and chemical reclaiming solutions are advancing, but scale and cost remain constraints.

- Raw-material price volatility. Leading indicators such as the U.S. Producer Price Index for wood pulp and observed regional kraft price variances in early 2026 highlight that feedstock exposure must be actively managed—via hedging, strategic inventory, index-linked contracts, or supplier diversification.

How to use this intelligence in 2026 (practical next steps)

PW Consulting recommends a three-tiered program for executives looking to convert market intelligence into near-term advantage:

- Immediate (0–6 months): Run a supplier health check using our scorecard—focus on continuity, compliance to EPR expectations, and carbon metrics; re-negotiate contracts to include indexation clauses where justified.

- Near-term (6–18 months): Pilot paperization or hybrid liner solutions on selected SKUs, with clear KPIs for recyclability, yield, and stored cost delta; set up a circularity trial with a reclaiming partner to validate end-of-life flows.

- Strategic (18–36 months): Pursue targeted M&A or JVs to secure technical capabilities (silicone application, reclaiming tech) and regional capacity—use our M&A screening checklist and ROI model to prioritize targets.

Why PW Consulting’s Release Paper Market report is essential for 2026

This Release Paper Market report is structured to be a working document for strategy and operations teams. It pairs market forecasting with executable tools and supplier intelligence—helping leaders translate macro trends into procurement actions, product choices and investment priorities without requiring in-house market modelling teams.

We present the depth analysts expect while deliberately reserving detailed segment-level tables and proprietary supplier scorecards for the full report—ensuring clients receive actionable, source-level data as part of the Purchase or Inquiry process.

Next steps and how to access the full intelligence

Executives seeking the complete dataset, supplier scorecards, scenario models and bespoke advisory services should visit PW Consulting’s Release Paper Market page to request the full Release Paper Market report and a 1:1 briefing. The full report contains the granular segmentation, regional detail and downloadable decision-support models needed to operationalize the guidance summarized here.

PW Consulting stands ready to run tailored workshops with procurement, packaging R&D and sustainability teams to convert the report’s insights into an executable 18-month roadmap—balancing cost, compliance and circularity in a market where both risk and opportunity are intensifying.

For detailed analysis of this topic, please visit the official page:Release Paper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com